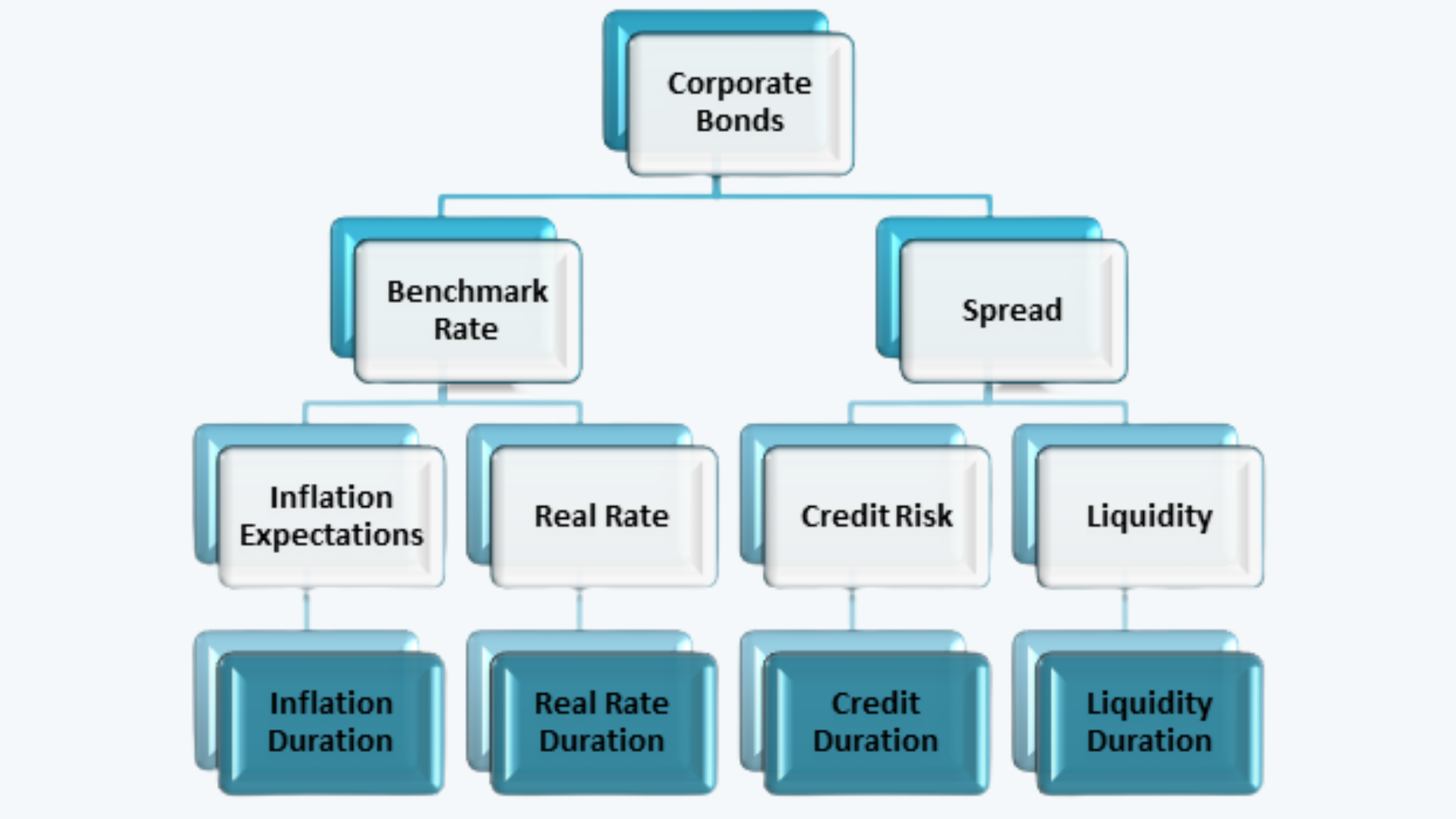

a. The returns on a corporate bond can be broken down into a benchmark rate and a spread.

b. The benchmark rate can be due to either the inflation expectation or the real rate changes.

c. The spread can be divided into credit risk and liquidity.

d. Each of these components has its respective effect on the duration. Such as:

i. Inflation expectation affects the inflation duration,

ii. Real rate changes affect the real rate duration,

iii. Credit risk affects the credit duration, and

iv. Liquidity affects the liquidity duration.

e. There is an interaction effect between each of the durations as mentioned above, such that, we don’t get one of these durations in isolation of others.

Generally, the conditions leading to the changes in the benchmark rates also affect the changes in the credit quality and the changes in the liquidity of the bond.