a. When an investor invests in fixed income securities, he receives a return from one or more of the following sources:

i. Coupon Interest Payments.

ii. Capital Gains (or losses) when the security matures or is called or sold.

iii. Interest received on the reinvested interim cash flows.

All these three sources of return from fixed-income security are to be considered while calculating the potential return using a yield measure.

b. The first source of return, i.e. coupon payment, and the principal repayments are subject to the credit risk. Whereas, the other two sources, i.e. reinvestment of coupon and capital gains/losses are subject to interest rate risk.

c. We can explain this with the help of an example.

Suppose we have an 8% 10-year, annual bond trading at $ 85.5030, we can calculate the YTM of the bond by solving the following equation for the value of r (or by simply using the financial calculator):

85.503075 = [8 / (1+r)1] + [8 / (1+r)2] + [8 / (1+r)3] + … … … + [8 / (1+r)n]

Solving the above equation, we get the value of r as 10.4%, which is also the YTM of the bond.

Now, if we assume that the coupons are reinvested at the same yield, up to the maturity of the bond, and all the investment so made will be liquidated at the time of maturity, i.e. after 10 years, we will receive a sum equal to the future value of an annuity of the coupon of $ 8 per annum for 10 years. The future value of the same discounted at the YTM of 10.4% will be $ 129.9707.

Therefore, in total the investor will receive the following:

|

Particulars |

Amount ( in $s) |

|

Total Coupons |

80.0000 |

|

Interest on Coupons |

49.9707 |

|

Principal |

100.0000 |

|

Total |

229.9707 |

In the above calculation, we have assumed that the coupons, when reinvested will yield the same returns, i.e. 10.4%. However, in reality, the return on the reinvested income may vary due to the changes in interest rates. This results in interest rate risk for the investors.

d. Thus, we can say that the yield-to-maturity or YTM concept assumes three things:

i. that the investments are held up to maturity,

ii. there will not be any defaults in the scheduled payments of coupons and principals, and

iii. coupons are reinvested at the same rate of interest as the investment.

e. In the above example, now let us assume that the investor, instead of holding the bond for 10 years sells it after four years.

In order to calculate the price at which this bond can be sold at the end of year 4, we need to discount the future value of the bond after 10 years (i.e. $ 229.9707) for 6 years by calculating the present value. Thus, the value of the bond after 4 years would be $ 89.6688.

Also, the FV of the coupon payments at the coupons at the end of 4 years would be:

8 (1.104)3 + 8 (1.104)2 + 8 (1.104)1 + 8 = 37.3471

Thus, we can calculate the total return on the bond by equating the current price of the bond with the discounted value of coupons and sale price. We would solve the following equation for r:

(37.3471 + 89.6688) / (1+r)4 = 85.5031

We get the value of r = 10.4%.

Based on the above calculations, we have the following basic assumptions:

i. that the coupons are reinvested at 10.4%, and

ii. the bond is sold on the constant yield price curve.

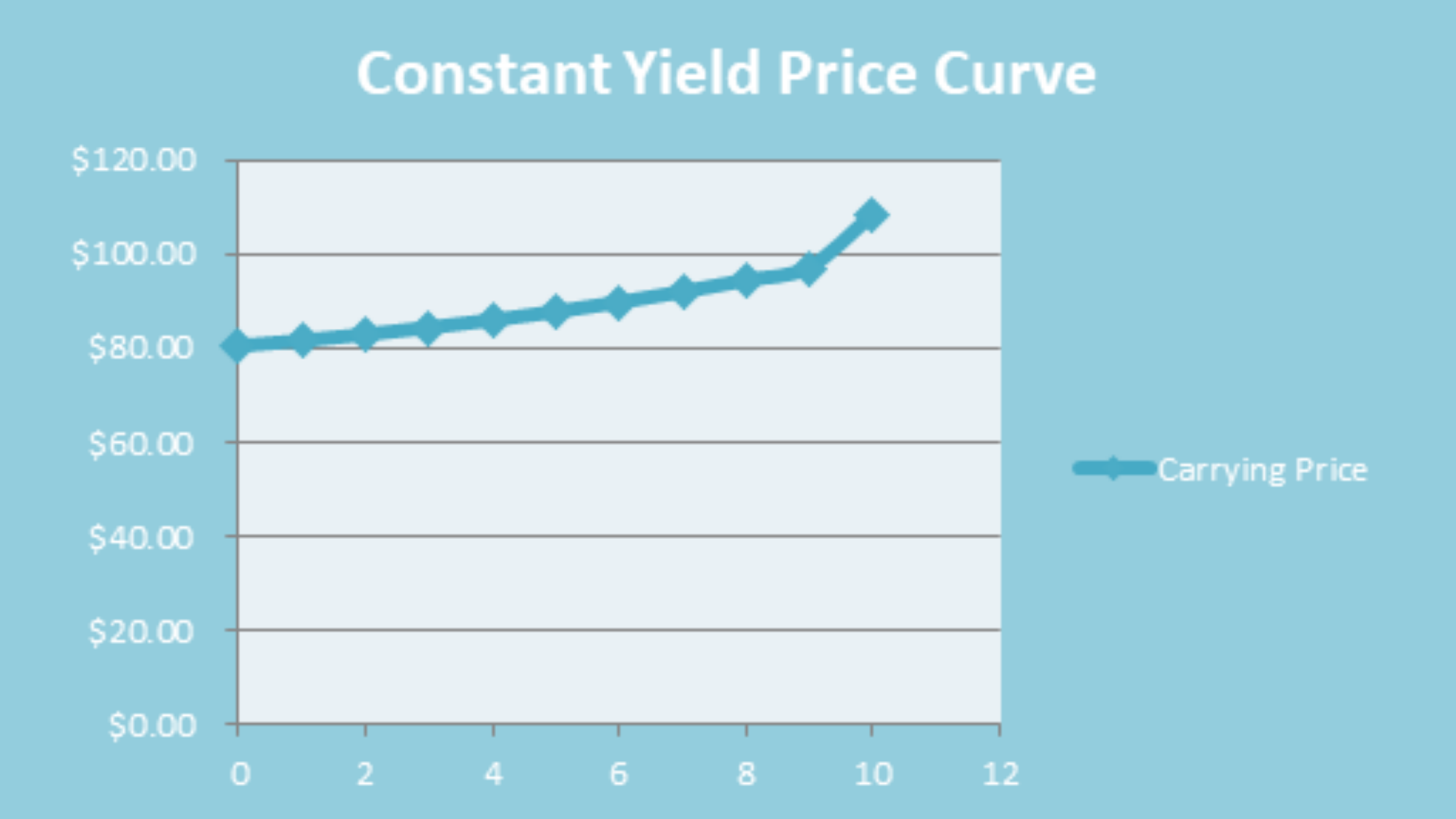

e. A constant-yield price curve shows the market price of the bonds, assuming that the yield of the bonds remains constant across the life of the bond. The constant yield price curve for the above example of the bond at 10.40 % yield would be:

Here, the carrying price, as reflected by the curve is nothing but the purchase price plus the amortized amount of discount or the premium.

If the bonds are sold during the life of the bond at the constant yield, it would fetch the price as reflected in the curve, i.e. its carrying value. However, if the bonds were to be sold at a yield above this curve, it would fetch a higher price and would result in capital gains, and vice-a-versa for the lower yield.

So, we can see that at the end of year 4 the price of the bond is $ 89.67 at the yield of 10.4%. Now if the yield rises by 100 basis points, to 11.4%; the price of the bond will be $ 85.78, and the future value of the coupons will be $ 37.90, making a total of $ 123.68. There is a capital loss of $ 3.89 as a result of the loss of the market price.

However, if there is a fall in the yield rate, there will be the following implications:

i. There will be lower re-investment of the coupon if the bond is held till maturity; and

ii. There will be lower re-investment and capital gain on the sale of the bond if the bonds are sold before maturity.