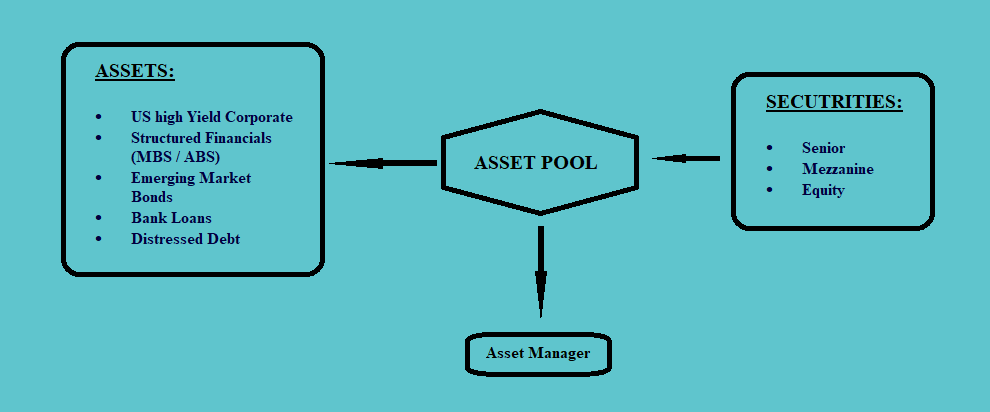

a. Under the CDO structure, the securities are issued, generally under different tranches, to generate funds that are managed by a fund manager and are invested in an asset pool consisting of different debt instruments.

b. Unlike the other asset-backed securities, under CDOs, first, the securities are issued, and then it is managed by an asset manager, who then decides where and how to invest.

If the funds are invested completely in the bonds instrument, they are called the collateralized bond obligations. However, if they are invested only in the loans, they are called collateralized loan obligations.

c. An asset manager is a person or an agency that buys and sells the assets to generate cash flows, in the form of capital gains, interests, etc.

There are certain restrictive covenants associated with the securities issued that guide the manager for their conduct and in their investment decision. The covenants may include the restrictions, such as, where the investments cannot be made (like on the basis of geography, or type of investments, etc.).

The ability to pay interest payments to the tranches depends on the performance of the assets and the asset manager.

d. The cash flow for the asset pool comes from three different sources:

i. interest payments,

ii. maturing assets, and

iii. sale of assets.

e. In a CDO structure, an SPV is floated which issues the bonds with floating rates and holds assets in the form of bonds having both fixed and floating rates. Thus, there is an interest rates swap (i.e. fixed for floating in this case).

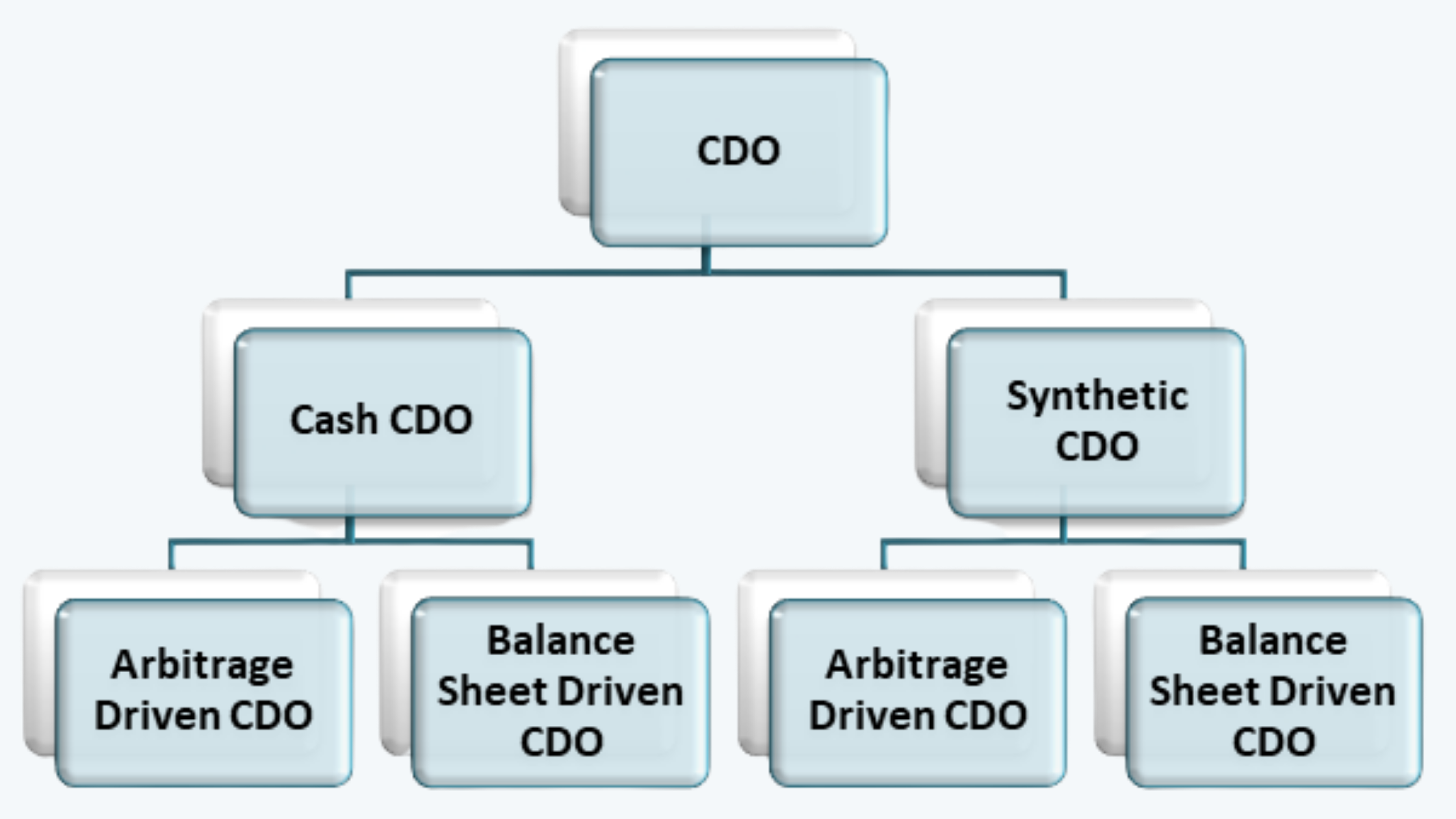

f. The CDOs can be classified into two major categories, i.e. Cash CDOs and Synthetic CDOs.

A cash CDO is mainly backed by real assets such as bonds and loans. However, synthetic CDOs are mainly backed by derivatives.

These two categories can be further divided into the arbitrage driven CDO and balance sheet driven CDO. The arbitrage-driven CDOs capture the spread and derive profits from the difference in yields on the assets. The balance sheet-driven CDO, on the other hand, removes the assets from the sponsor’s balance sheet.

g. The main motivation behind the CDOs is active management.

h. The timeline of a CDO basically has two types of periods, i.e. the ramp-up period and the reinvestment period.

The ramp-up period is the initial phase on the timeline of a CDO, usually the first year, where the management is engaged in buying the assets. The phase after the initial year is the reinvestment period, where the assets are sold, the securities are retired and the proceeds are reinvested.