a. Duration is a good measure while estimating the percentage price change for a small change in interest rates, but the estimation becomes inferior with the larger change in interest rate. Therefore, the duration is only an approximation of a percentage price change for a small change in the yield.

The reason for this is, the duration is a first approximation for the small change in the yield.

b. By using the second approximation, it can be improved. This approximation is known as convexity.

We can use the convexity measure of the security to approximate the change in price that is not explained by the duration.

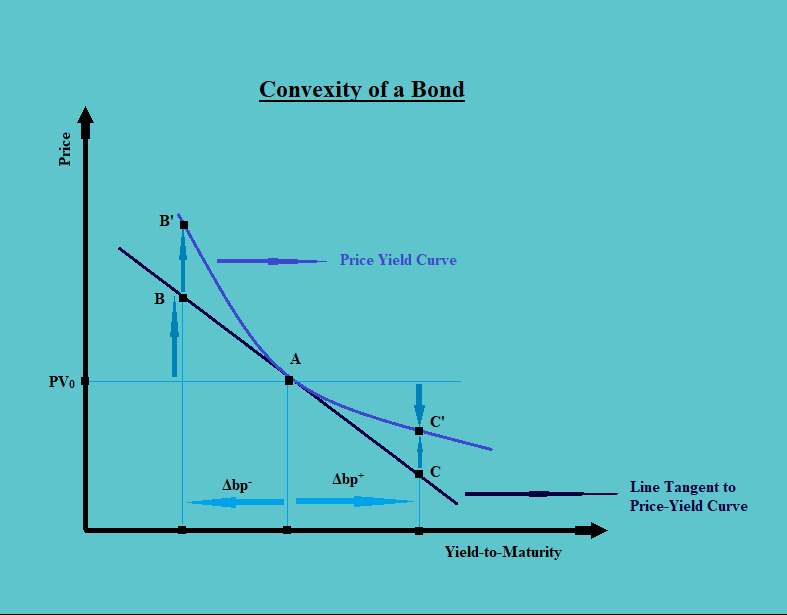

c. Consider the following diagram:

In the above diagram, we can see that due to an increase or decrease in the yield (by the amount Δbp+ and Δbp–). The duration of the bond reaches up to point C and B respectively. But these points lie on the line tangent to the price-yield curve. But to reach the point on the price-yield curve, up to point B’ and C’, there is a need for the convexity adjustment.

d. The percentage change in the total price is a result of two effects, i.e. the first is a result of duration (called the first-order effect) and the second is a result of convexity (called the second-order effect).

|

The first part of the total percentage change is due to the duration, and the second part due to the convexity.

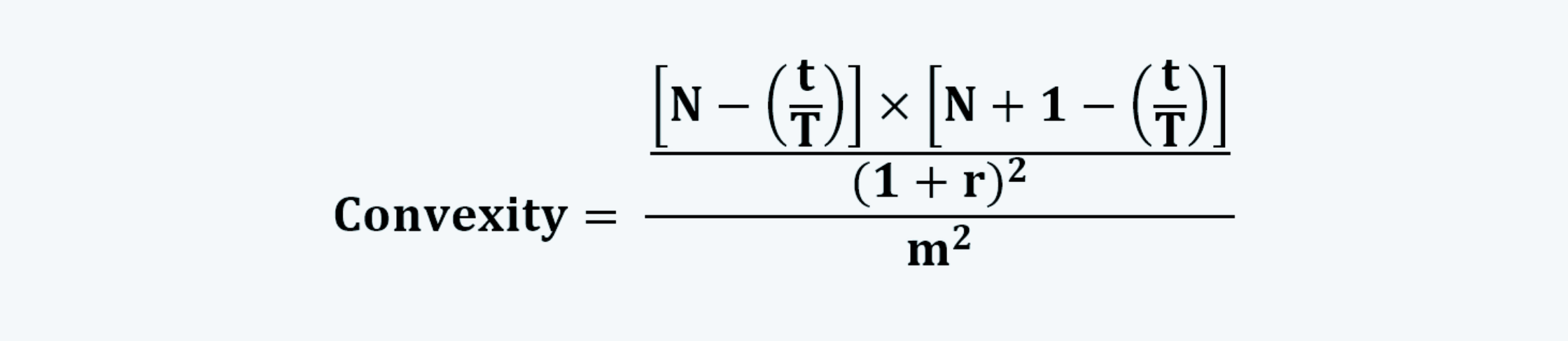

e. The convexity of a bond can be calculated using either the closed-form formula or the approximate formula.

f. The closed-form equation for calculating the convexity of a bond is:

|

g. The approximate convexity can be calculated using the following equation:

|

h. The one calculated above is the convexity of a bond in percentage terms. We can also calculate the money convexity of the bond or the convexity of a bond in dollar terms.

The equation for the money convexity of a bond is:

|

The first part of this equation refers to the first-order effect. Whereas, the second part refers to the second-order effect.

i. When the bonds cash flows do not change as a result of the change in yield, we can use the approximate convexity measure, which is:

|

j. However, when the cash flows changes, we need to calculate the effective convexity using the following equation:

|

1.1. Yield Volatility

a. The yield volatility shows the number of basis points changes in the duration, due to certain basis point changes in the yield of a bond.

b. There are mainly two sources of yield volatility:

i. Interest Rate Shifts. To manage the same, one needs to measure the interest rate risk first. Duration analysis is an important tool for the analysis of the sensitivity of portfolios to changes in interest rates.

ii. Changes in Volatility of Interest Rates. Although less common, this type of risk is a major component of the total risk of a fixed income portfolio. The greater the expected yield volatility, the greater is the interest rate risk for the given duration and current value of a position.