a. Before we define and understand the meaning of securitization, it is important to understand the mechanisms through which the traditional bonds function.

The bonds that are issued to the investors are backed by the physical assets of the company.

On the other hand, the debenture holders have a general claim over the assets of the company. The debentures are not backed by any specific physical assets.

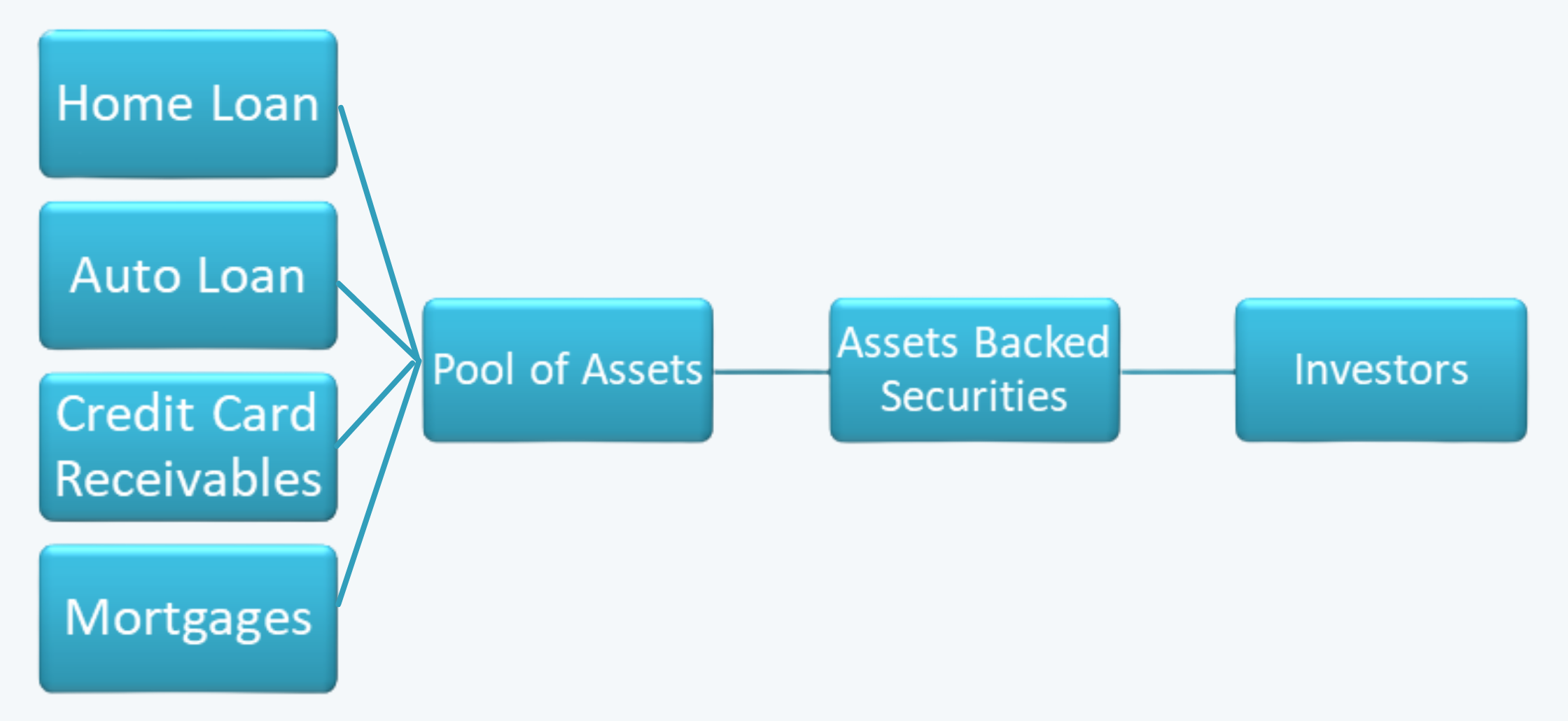

b. On the contrary, asset-backed securities are a type of bond or note that is based on a pool of assets or collateralized by the cash flow from a specified pool of underlying assets. The assets are pooled to make otherwise minor and uneconomical investments worthwhile, while also reducing risk by diversifying the underlying assets. Securitization makes these assets available for investment receivable like credit card payments, auto loans, housing loans, and mortgages. Typically, the securitized assets might be highly illiquid and private in nature.

1.1. Process of Securitization

The process of securitization follows the following steps:

a. Transfer of assets by the originator (person holding the assets, or the consumer company) to an entity (company or trust) specially created for the purpose called Special Purpose Vehicle (SPV). SPV is a separate entity formed exclusively for charting this deal and providing funds to the originator.

b. The assets transferred should preferably be homogeneous in nature in terms of the risk attached to them and/or maturity such that the pooling of such assets would be convenient. SPV divides this pool of assets transferred by the originator into marketable securities called Pay or Pass-Through Certificates and resells them to various investors.

c. The investors may either be banks, mutual funds, or state or the central government. The investor may even be a parent company or the financer of the originator.

d. The issue of securities is managed by the merchant banker, who may underwrite the whole issue or a syndicate of a merchant The originator continues to administer the loan portfolio for some fee and he passes the collections to the trust which services the securities.

Apart from the SPV, a trustee is normally appointed to oversee the process of securitization. An escrow account is created for the purpose of distributing the receivables to the investors in the deal. The trustees maintain such an escrow account.

1.2. Parties Involved in Securitization

Looking at the above process of securitization, we have the following parties involved in the process of securitization:

a. Seller: The seller is the originator of the loan or the consumer company.

b. Issuer/Trust: The issuer is the Special Purpose Vehicle or SPV created for charting the deal.

c. Servicer: These are the other parties involved in collections, etc.

d. Others: Others involve the parties such as lawyers, underwriters, accountants, rating agencies, trustees, etc.

1.3. The Documents Required in Securitization

Following documents are required to be made in the process of securitization:

a. Prospectus: Prospectus is set up as a waterfall agreement. It lists the following:

i. Priority and the amounts of payments,

ii. Service fee,

iii. Administration fees,

iv. Principal,

v. Interest, etc.

b. Purchase Agreement: It is the agreement between the seller and the SPV.

c. The Waterfall Structure: It describes the structure of the security on the basis of priority.

d. Servicing Agreement: It is the agreement between the servicing agency and the SPV.

1.4. Bond Classes/ Tranches Issued

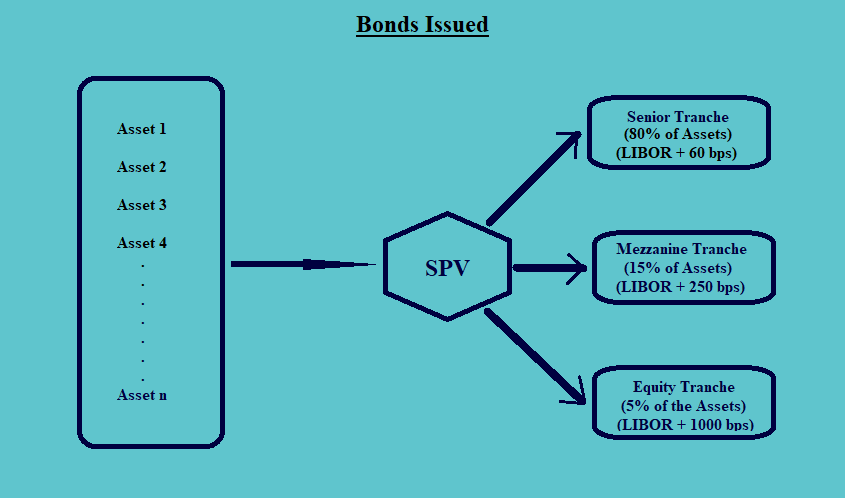

The bonds are issued by the SPV, which collects (purchases) the assets from the originator. These assets are funded by issuing bonds. The bonds are generally issued in different classes or tranches, based on the riskiness of each class. This can be explained with the help of an example; consider the following figure:

a. In the above figure, the box on the left-hand side represents all the assets that are sold by the originator to the SPV.

b. The SPV issues the bonds belonging to different tranches to finance these assets.

c. In the above example, the issuing price of the senior-most tranche of the bonds is enough to buy 80% of the assets, then the second tranche represents 15% and the last one (i.e. the equity tranche) represents 5% of the assets.

d. The senior tranche is the highest-rated bond issued by the SPV. In case of a default of up to 20% by the assets, the senior tranche will receive the full payment. The lower tranches do not get paid in such cases. The higher tranches have a priority in terms of receiving the payments in case of any default. Thus, there is credit protection of 20% for the senior-most tranche and credit protection of up to 5% for the middle tranche, i.e. mezzanine tranche. Thus, credit tranching helps in reducing credit risk.

e. Since the tranches with higher levels of seniority are more secured, they can be issued at lower interest rates. And, since the credit risk keeps on increasing for each lower level of tranches, they must be issued for a higher spread than the previous tranche bonds. And the senior tranches are also rated higher.

f. The assets in the senior-most tranche are the easiest to sell. It is difficult to sell the assets in the mezzanine tranche, and those in the lowest tranche are the most difficult to sell, since they have the highest risk of default, and are mostly retained by the originator.

g. Within each of the tranches themselves, the bonds are again divided into sub-tranches. While making the payments within the sub-tranches also, the order of seniority is followed and the sub-tranches which are higher in the priority are given priority over the lower tranches.

h. Instead of assigning a credit tranche as above, the companies can also redistribute the prepayment risk through time tranching or prepaid tranching. Here, the bonds are assigned to the tranches according to different terms to maturity and yields. In the time tranching:

i. Each bond class receives periodic interest;

ii. However, the principal is paid to the senior tranches first, before heading to the next level of tranche for making the payment.

i. A company may also use a combination of credit tranche and time tranching.