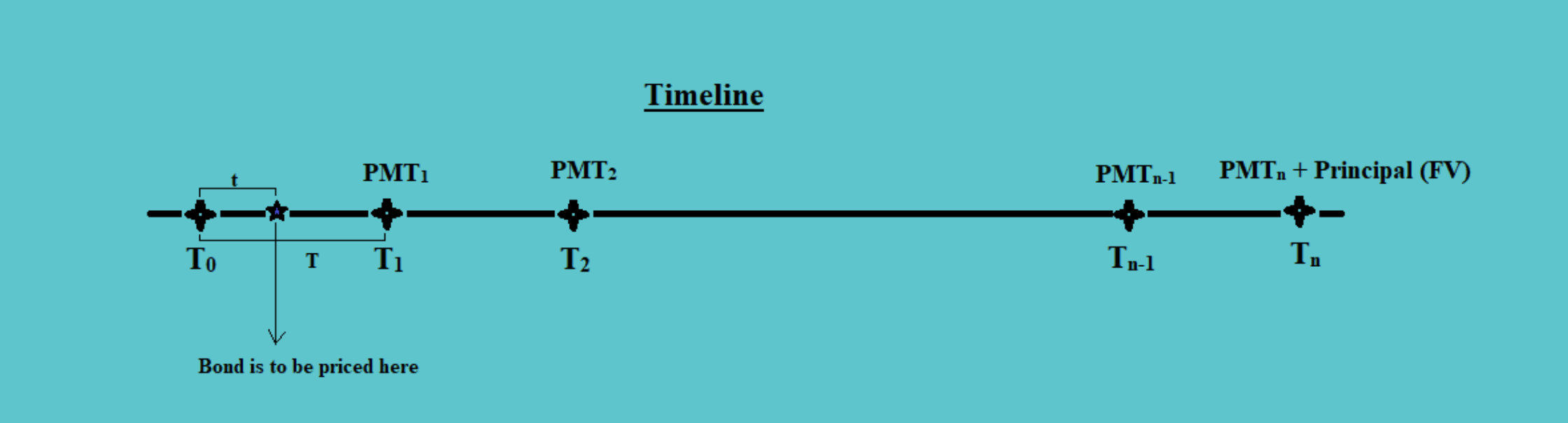

a. Up to now, we have calculated the present value of the bond on the payment date. But, the bond could be priced in between the payment dates as well.

Thus to say, on the following timeline, the bond is supposed to be priced in between the payment dates:

Here, ‘t’ is the number of days from the last coupon date to the settlement date. And, ‘T’ is the number of days between each payment.

b. The price of the bond, on a day, in between the two payment dates has two parts, i.e. the flat price and the accrued interest. Therefore,

| PVfull = PVflat + AI |

The full price of the bond is also called its ‘dirty price’, whereas, the flat price of the share is also called the ‘clean price’ or the ‘quoted price’.

c. The full present value of the bond is:

|

or, we can simplify this equation as:

|

Thus,

d. The accrued interest is the proportion of time that the seller held the bond times the payment. That is,

|

e. There are two ways of calculating the number of days, i.e. ‘actual/actual convention’ and ‘30/360 days convention’.

In the ‘actual/actual convention’ we calculate the actual number of days and in ‘30/360 days convention’ we consider 30 days a month and 360 days in a year.

Thus, for example, if for a bond the coupon dates are May 15th and November 15th, and we have to calculate the accrued interest on June 27, then the number of days would be calculated as follows:

i. actual/actual convention: (16+27)/184 = 43/184 days

ii. 30/360 convention: (15+27)/180 = 42/180 days

The actual/actual convention is used for the valuation of government bonds and the 30/360 convention is used for the valuation of corporate bonds.