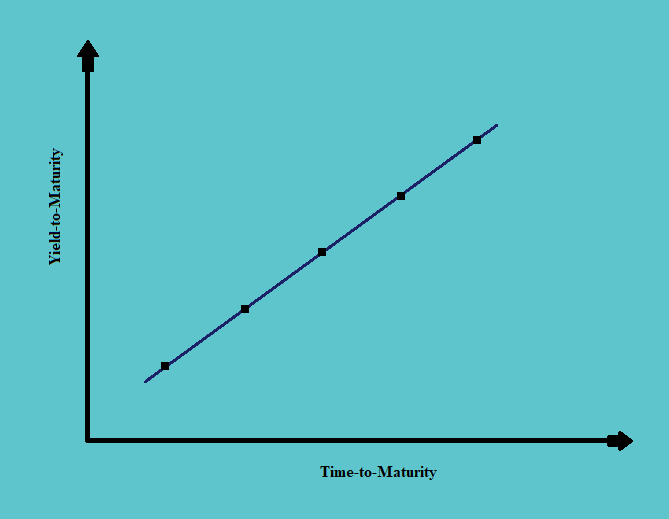

If everything else is constant (which is not generally practical), the YTM of a bond increases with an increase in the time-to-maturity of a bond. Thus the yield curve is generally an upward-sloping straight line.

1.1. A Government Bond’s Spot Curve

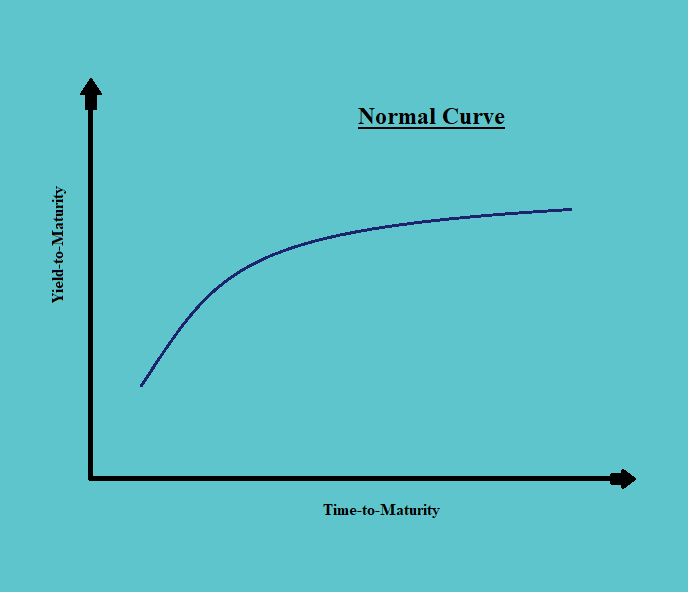

a. A spot curve is the curve joining the YTMs on zeros for a range of maturities. If the bonds are coupon bonds, the zeros can be created by stripping the bonds

b. A normal spot curve of government bonds is an upward sloping curve, sloping at a decreasing rate, and the YTMs is generally stated on a semi-annual basis.

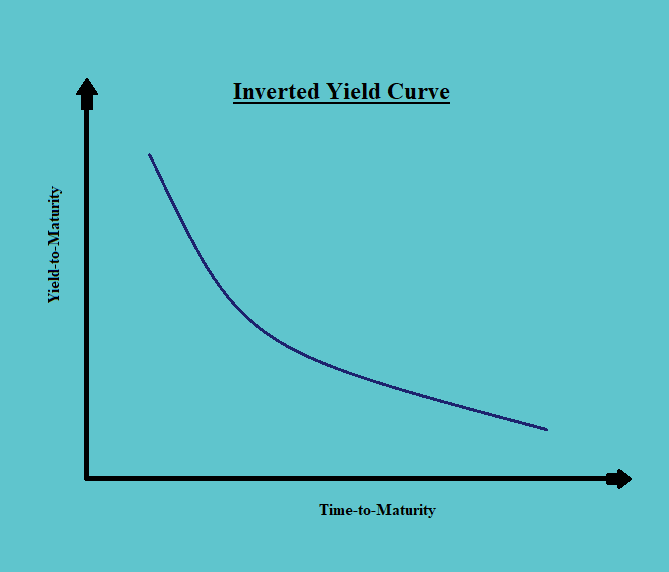

c. The curve may, however, also be a downward sloping curve. This generally happens prior to the recession. But it does not indicate that a downward slope in the yield curve would be followed by a recession.

d. The zero curves are theoretically the ‘pure curves’, but since most of the bonds pay coupons, these curves are not very useful.

1.2. Government Bond’s Yield Curve

a. For a coupon paying bond, the yield curve looks like the following

b. This curve is a linear interpolation of various points.

c. In the money market, the non-coupon-paying bonds can be converted into bond equivalent yields.

1.3. Par Curve

a. The par curves are obtained from the spot curves, and each maturity is priced to par on these curves.

b. The yield on these curves is calculated by assuming that each of the bonds is currently priced at its par value. And the curve is drawn by joining these yields.

c. The par curves also look similar to the bond yield curves.

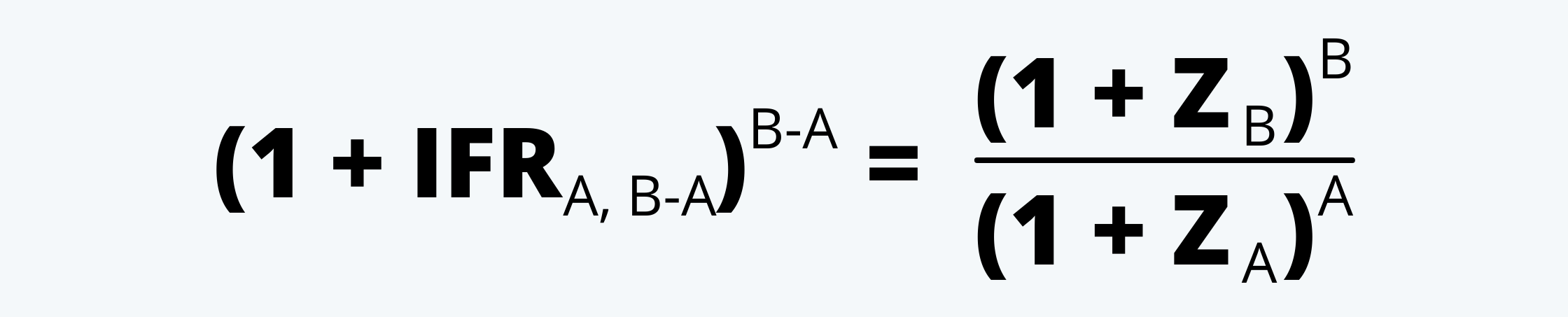

1.4. Forward Curve

a. These are the curves based on the forward yields; the yields that are agreed on today, to be delivered in the future.

b. These bonds are quoted as ‘when what’ bonds. Thus, if there is a 1y5y bond quoted, it would mean that there is an agreement to deliver a 5-year bond in a year from now.

c. Thus, to generalize, we can say, that AyBy bond would answer two questions:

i. When? To be delivered in A years from now.

ii. What? A (B-A) year bond.

d. If we have two spot rates available for A-year and B-year bond, then we can calculate the yield on this bond as follows:

|