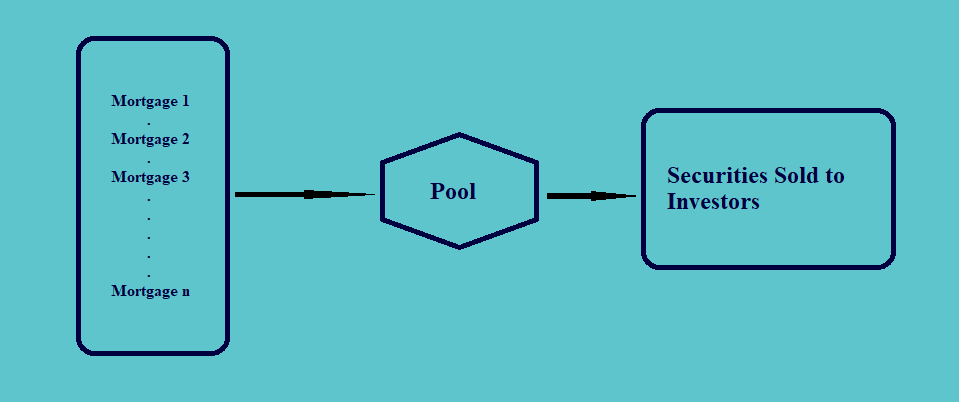

a. A mortgage pass-through security is a share or a participating certificate issued by a collection pool comprising several mortgages.

b. The mortgage is said to be securitized when the mortgage in the pool of mortgages acts as collateral to the mortgage pass-through security.

c. The cash flow to the investors of these securities depends on the cash flow generated by the pool which is in the form of interest, principal, prepayment, and penalties.

d. The securities holders receive the principal and interest each period, whose timings and the amount may not be identical to the ones received from the pool. The amount that the holders receive is the monthly cash flow from the mortgages less the servicing and other fees like the fee charged by the issuer or the guarantor. The rate at which the security holders are paid is called the pass-through rate.

e. Since a pool consists of different mortgages which may vary in terms of the mortgage rate and the timings of cash flows, the pool actually has a weighted average coupon rate (WAC) and Weighted Average Maturity (WAM).

f. To be included in a pool, each mortgage must meet certain underwriting standards based on the size of the issue, the documents required, maximum loan-to-value, insurance, etc. Those mortgages that meet such standards are called the conforming assets, while the others are the non-confirming assets.

1.1. Measuring The Prepayment Speed

a. The prepayment can be measured using two measures, i.e. the single monthly mortality (SMM) rate, a monthly measure, and its corresponding annualized rate, the conditional prepayment rate (CPR).

b. The SMM, during any point in time, is calculated using the following equation:

|

The value of prepayment during any month is determined based on historical observations of actual activity in the month t.

If, however, the SMM is assumed, the expected prepayment amount can be calculated by multiplying the SMM with the difference between the beginning balance and the scheduled principal payment during the month.

c. The SMM gives us the monthly mortality rate; we can annualize the same to calculate the conditional prepayment rate or CPR. The CPR can be calculated using the following formula:

| CPR = 1 – (1-SMM)12 |

In the above equation, 1-SMM represents what is not being prepaid during the year. And, (1-SMM)12 represents what is not being prepaid during the year.

Thus, the whole term, i.e. 1 – (1-SMM)12 represents what is being prepaid for the year. The value of CPR, thus, represents the percentage of beginning-year principal that will be prepaid during the year over and above the regular principal payments.

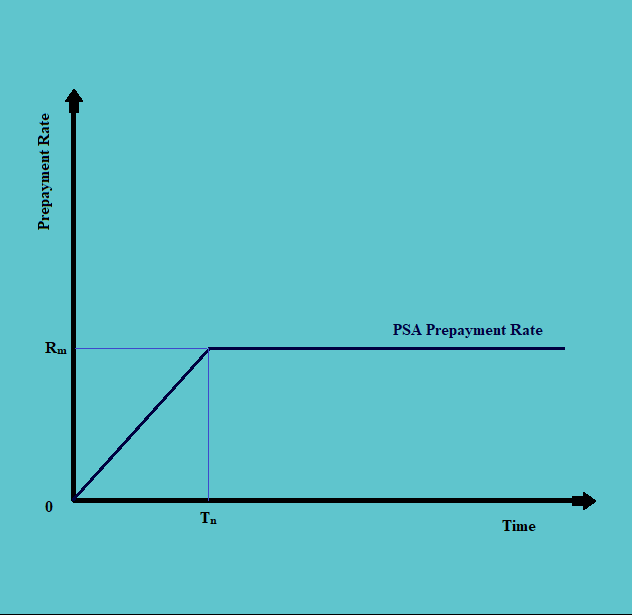

d. The prepayments can also be measured using the PSA (Public Security Association) Prepayment Rate. Here, the prepayment is described in terms of prepayment pattern or a benchmark over the life of a mortgage pool. It is expressed as a monthly series of CPR. According to this measure, the prepayment rates are low at the beginning, but as the age of the mortgage progresses, there is an increase in the prepayment rates until they become stable after a certain time period.

If there is complete conformance in the pattern of a prepayment with the prepayment benchmark rates, then it is called 100% PSA or 100 PSA.

A zero PSA generally means that there is no prepayment, whereas 100 PSA means that prepayments are at the same speed as benchmarks. A less than 100 PSA would mean slower prepayment, whereas a more than 100 PSA mean a faster prepayment.

1.2. Weighted Average Life

a. Weighted average life is the average life up to the maturity of the bonds, after taking into consideration, the regular principal payments and repayments.

b. It can be calculated using the following formula:

|

c. The weighted average life depends upon the PSA speed and the prepayment assumption.

d. The mortgage rate also affects the level of prepayments and thus the average life in the following ways:

i. If the mortgage rate drops, the amount of refinancing increases, increasing the level of prepayments. With an increase in the level of prepayments, there is an increase in the PSA Speed, which in turn decreases the average life. This also results in contraction risk

ii. On the other hand, when there is a rise in the mortgage rate, the refinancing decreases, resulting in a fall in the level of prepayments. A fall in the level of prepayments decreases the average life of the securities. This results in an increase in extension risk.

e. We can thus sum up the prepayment risk and its two components (i.e. extension risk and contraction risk through the following table:

|

Prepayment Risk |

Contraction Risk |

Extension Risk |

|

Arises from: |

Decreasing Rates |

Increasing Rates |

|

Results in: |

· Shorter average life · Greater cash flows |

· Longer average life · Minimum cash flows |

|

Adverse Condition: |

· Price will not rise by an amount as much as an option-free bond. · Lower reinvestment of cash flow. |

· Price will fall at about the same rate as an option-free bond. · Lower cash flow for reinvestment |