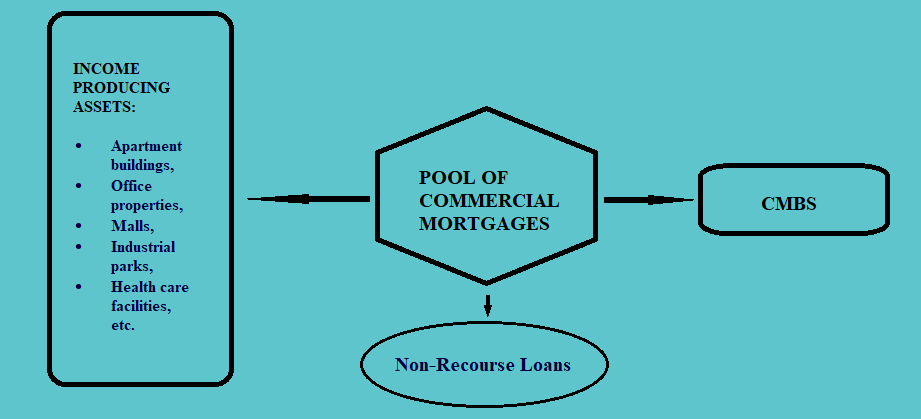

a. These mortgage-backed securities are backed by income-producing real estate, usually in the form of warehouses, shopping centers, apartments, office buildings, senior housing, health care facilities, hotels or resort properties, etc.

b. These loans are originated usually by conduit organizations like commercial mortgage companies, which negotiate and close commercial real estate loans that are incorporated into CMBS.

c. The assets held under the pool of commercial mortgages here are the non-recourse loans. Therefore, the credit analysis involves the analysis of cash flow on a loan-by-loan basis.

d. The credit analysis can be done using the following two ratios:

i. Debt-to-Service Coverage Ratio: This ratio can be calculated using the following formula:

The higher this ratio, the better it is.

ii. Loan-to-Value Ratio: This ratio can be calculated using the following formula:

The appraised value in the commercial MBS can be manipulated. Therefore, usually, there is a low loan-to-value for commercial properties in comparison to residential ones.

e. The commercial MBS, like the non-agency MBS, requires credit ratings. Therefore, if the DSC and LTV ratios are not sufficient for a rating, then there is a need for credit enhancement, especially in the form of subordination.

f. The rating agencies, thus, require sequential retirement. Therefore, the losses from the defaults are first charged against the lowest priority tranche (usually called the first-loss piece, equity tranche, residual tranche, etc.)

g. The commercial properties generally offer a higher level of call protection, in form of lower prepayment risk, in comparison to the loans on the residential properties. This call protection is mainly from the prepayment and credit risk and is in form of:

i. Prepayment Lockout: This is the initial period of the loan where the restriction is imposed on the prepayment of the same. If the prepayment is made during this period, there is a penalty imposed.

ii. Defeasance Premium: Here, the borrower of the loan purchases the securities as collaterals to cover the remaining principal balance along with an amount to substitute for what the yield would have been

iii. Prepayment Penalty Points: Here, if the borrower wishes to prepay, there are penalty points attached to them, and the borrower has to pay 100 percent plus the penalty point percent as a premium. For example, a loan has a five-year lock-in period, with penalty points of 5, 4, 3, 2, and 1. Now if the borrower wants to make a prepayment in the first year, he will have to make a payment of 105% of the principal, 104% of the principal in the second year, and so on.

iv. Yield Maintenance Charge: This is a kind of penalty imposed on the borrower for prepayment, equivalent to the amount of yield that is lost as a result of the prepayment. The main purpose of this charge is to maintain the yield of the asset even in the case of prepayment. The penalty so imposed is also called the make-whole charge. In case of a change in interest rates, if the borrower gets the assets refinanced to get a lower rate, the borrower must make the yield whole. At the structure level, the manager of the fund can opt for credit tranching.

h. The CMBS, unlike the residential MBSs, are not always fully amortizing loans. They may also be partially amortizing loans, and hence, may require balloon maturity provisions. This provision requires the borrower to make one big balloon payment at the end of the term of the loan.

Thus, at the end of the term, the borrower may not be able to refinance, sell the property, or pay the loan. This results in balloon risk or extension risk. In such situations, the lender is most likely to extend the loan.