a. The credit risk can be classified into two components, i.e. default risk and loss severity.

b. The default risk is the risk that arises when the issue is not able to satisfy the terms and conditions of the obligations with respect to the timely payment of interest and repayment of the amount Thus,

c. The loss severity is the amount of exposure to the loss of the lender in case of any default.

If the default occurs, the investor does not lose the entire amount invested as he can recover a certain percentage of the investments. This is called the recovery rate.

d. Normally, credit rating agencies rate the companies for their issue on the basis of certain factors like capital structure, leverage ratio, earnings ratio, current ratio, the performance of the particular industry, etc., and give the ratings for the issuing companies. Companies with higher ratings will have lesser default possibilities compared to the companies with lesser ratings.

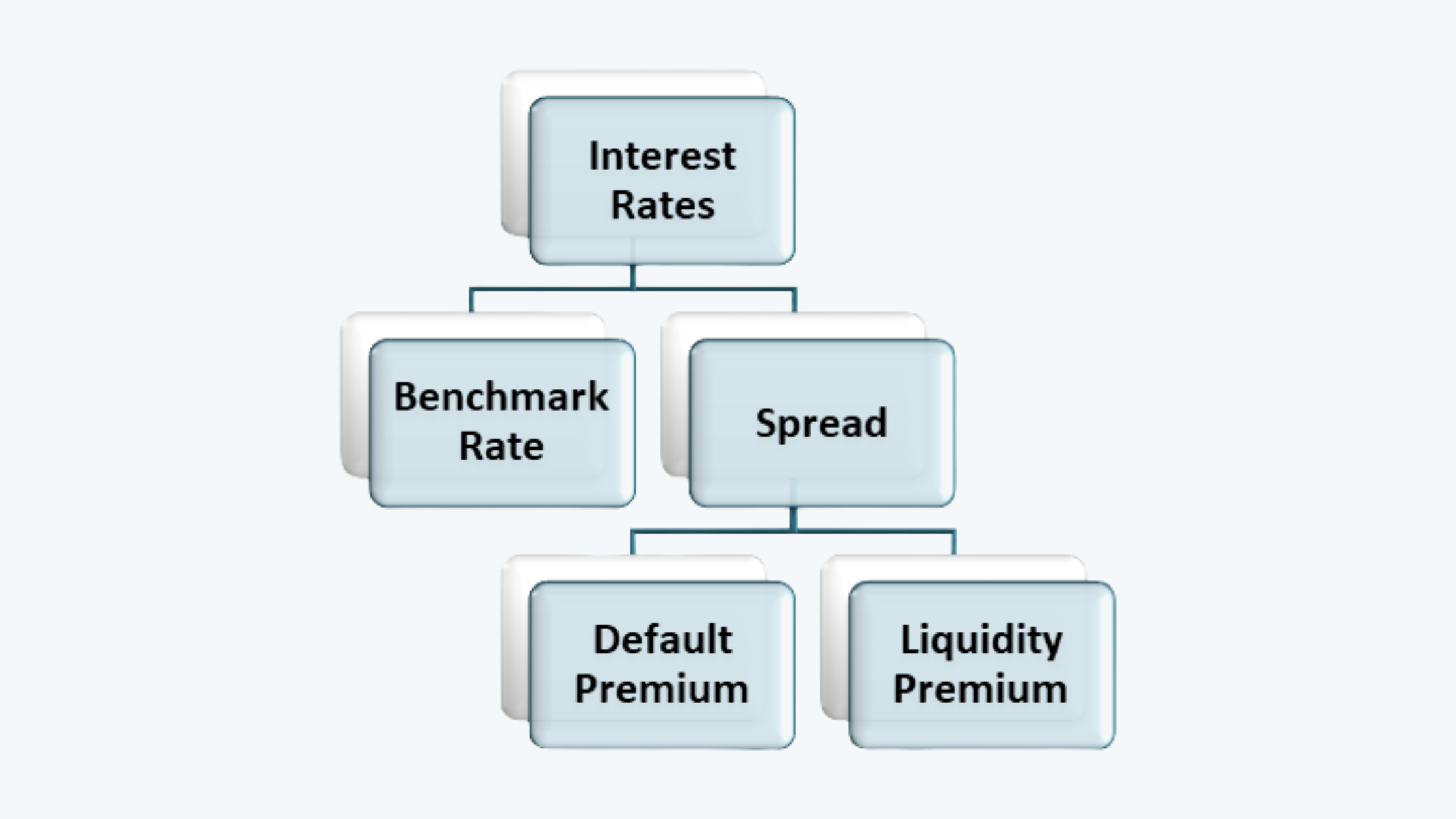

e. As discussed before, a corporate issue is based on a benchmark rate plus some spread. This spread can be bifurcated further into a default plus some liquidity premium.

f. The liquidity premium is mainly offered to compensate for the credit spread risk, i.e. the situation where the market price of the bond differs from the transaction price of the similar securities. It is a function of credit quality and the size of the debt.

f. The default risk premium, on the other hand, is offered for the credit migration risk. It is the risk that arises due to chances of downgrades in ratings by the rating agencies. An unexpected downgrade increases the credit spread and fall in bond price. The risk involved here is the downgrade risk and is closely related to credit spread risk.