a. We have seen that the YTM of a bond is the sum of the benchmark rates (generally risk-free) plus a risk premium.

b. The risk on the benchmark is generally called the beta risk and the risk on the spread portion is called the alpha risk.

c. The alpha risk is mostly influenced by the micro factors, whereas the beta risk is influenced by the macro factors.

The micro factors include the impact of taxation, liquidity and credit risk, etc. The Macro-factors include the factors such as inflation, real rate, etc. The micro factors also sometimes have a macro influence.

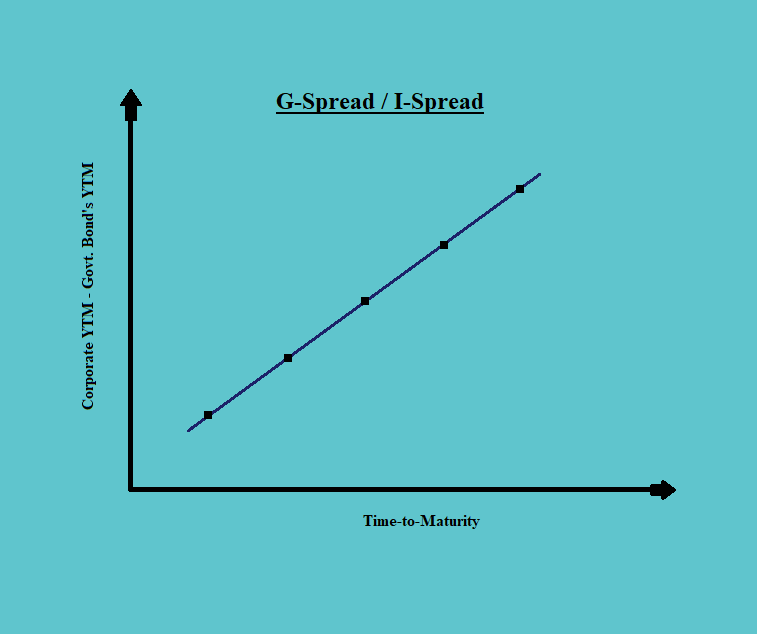

d. The benchmark is generally the yield on the government bonds that were issued most recently are on the run. And the spread of these yields is called the G-Spread. For some bonds such as European issued bonds, the benchmark is some swap rate, and the spread on it is called the I-Spread.

e. We can plot the G-Spread or I-spread curve by reducing the YTM on government bond from the YTM on corporate bonds, as follows:

f. As the time to maturity of the bond increases the spread between the bond price and the interest rates increases.

g. For G-Spread / I-spread, all the cash flows are discounted at the same

h. If we use Z-spread instead, all cash flows are not discounted at the same Rather, they are discounted at some constant spread plus some spot rate. The spot rate changes over time. The Z-Spread is also called the zero-volatility spread.

i. Thus, the present value is:

|

Where, z = Spot Rate Z = Spread |