1.1. Yield Measures for Fixed-Coupon Bonds

a. The yields on the fixed coupon bonds are generally stated on an annualized basis, but these are not compounded, rather they are the simple average basis.

b. For a zero-coupon bond, which is stated on an annual yield basis, if there is a different periodicity, it results in a different yield.

This can be seen with the help of the following example:

If a 5-Year bond is stated at $ 80, then the yields for different periodicity would be:

|

Periodicity |

Calculation |

Yield |

Annualized |

|

|

Annual |

[(100/80)^(1/5)] -1 |

0.0456 |

0.0456 |

|

|

Semi-Annual |

[(100/80)^(1/10)] -1 |

0.0226 |

0.0451 |

|

|

Quarterly |

[(100/80)^(1/20)] -1 |

0.0112 |

0.0449 |

|

|

Monthly |

[(100/80)^(1/60)] -1 |

0.0037 |

0.0447 |

|

The values in the last column reflect the effective annual rate, semi-annual bond basis yield, quarterly bond equivalent yield, and monthly bond equivalent yield.

However, instead of annualizing, if we compound the yield, we would get all the yields equal to the effective annual yield. Thus, for a semi-annual bond, if instead of multiplying 0.0225 by 2, if we compound the same as follows the effective annual yield would be:

(1.02256518)2 -1 = 0.04564 or 4.564%

This is the same as the effective annualized yield.

c. For converting the annual yield from one periodicity to another, we equate the following equation:

d. The street convention for the yield on fixed coupon bonds assumes that the payment date or the date on which the redemption of the bond falls due could be any weekend or a holiday.

e. The true yield, however, takes delayed payments and future value into consideration. But this yield is difficult to calculate and rarely significant.

f. The government equivalent yield is quoted for a corporate bond. It restates the yield as per the 30/360 convention to the yield as per the actual/actual convention. This results in a more accurate measure than the ‘spread over the benchmark’.

g. The current yield or the income/interest yield is the return calculated in terms of payments received each year (in the form of interest or coupon) over the flat present value of the bond. It takes into account only the interest and ignores the reinvestment of capital gains if any on the investment. Thus,

|

h. The simple yield is also similar to the current yield, except, it also takes into account the straight-line amortization of capital gains or losses during the year. Thus,

|

i. Then, there are bonds with the embedded options, such as call and put options. With these bonds, the valuer needs to calculate the value of these options as well.

For example, there is a 7-year, 8% annual bond, callable after 4 years, currently trading at $ 105. The call, schedule of the bond is such that, if it is called at the end of the next 4 years, it can be called at $ 102. If it is called at the end of the next 5 and 6 years, it could be called at $ 101 and $ 100 respectively.

For calculating the yield of the bond, we calculate the respective yields on the bond if it is called in the 4th, 5th, and 6th year respectively. Using the financial calculator, we can calculate the yields as follows:

|

Yield to the first call |

: 6.975% |

|

Yield to the second call |

: 6.956% |

|

Yield to the third call |

: 6.953% |

|

YTM |

: 7.070% |

The lowest of the above yields is called the ‘yield-to-worst’. This is considered as the yield on the bond.

For a more precise measure of yield, the valuer can value the embedded option separately, using the option pricing model and the estimate of future interest rate volatility. Thus the option-adjusted price of the bond is the flat present value of the bond plus the value of the option. The value of the call option is added, whereas, the value of the put option is subtracted from the value of the bond.

1.2. Floating Rate Notes

a. As seen in the fixed-rate bonds, the coupons remain fixed, but the price of the bonds changes with a change in interest rates. Thus the fixed coupons have price variability. A floating rate bond, on the other hand, has coupon variability. Its coupons changes with a change in the interest rates. The price of a floating rate bond remains fairly constant.

b. The coupons in the floating rate notes are generally tied to the short-term money market rates, such as 3-month LIBOR. It is a sum of the reference rate plus some quoted margin. The quoted margin is generally credit-related and may be negative as well. The interest rates at which the coupons are paid are determined at the beginning of the period. And it is paid at the end of the coupon period.

c. The required margin is the market-determined rate of interest at which the coupons are discounted.

Thus, for example, if there is a floating rate bond, with a 50 bps quoted margin, if there is no change in credit risk, the required margin remains the same. Thus, a change in credit risk equals the change in the required margin. If there is no change in the coupon payments of a floating rate note, between the two coupon dates, the price of the bond remains the same on the two dates. However, the prices may fluctuate in between.

d. The quoted margin and discount margin generally have the following impact on the price of the bond:

i. If the quoted margin equals the discount margin, the present value of the cash flow and thus the price equals 100 on the payment date.

ii. If the quoted margin is greater than the discount margin, the present value of the bond is greater than 100 and it is a premium bond on the payment date.

iii. If the quoted margin is less than the discount margin, the present value of the bond is less than 100 and it is a discount bond on the payment date.

e. The formula for calculating the value of the bond is:

|

1.3. Money Market Securities

a. The money market securities are basically pure discount bonds, whose term to maturity is one year or less. Thus, the yields on these bonds are annualized, but not compounded (as the returns are not reinvested).

b. The yields on the money market securities are stated on a simple interest basis. They are either quoted on a discount basis or the add-on basis.

c. If the yields are quoted on the discount basis, the PV of the bond is calculated as follows:

|

Where, DR is the discount rate. |

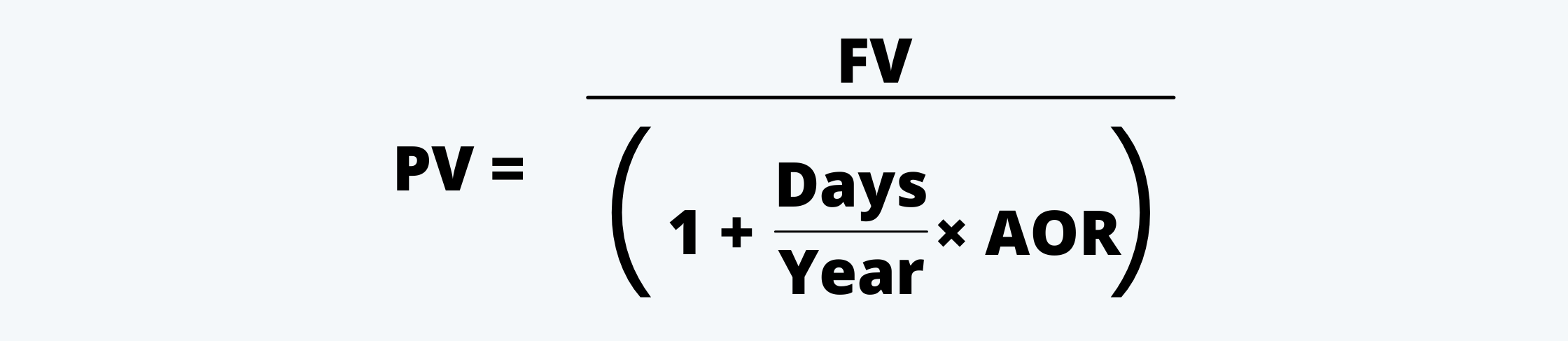

d. If the yield is quoted on an add-on basis, its PV is calculated as follows:

|

Where, AOR is the add-on rate. |