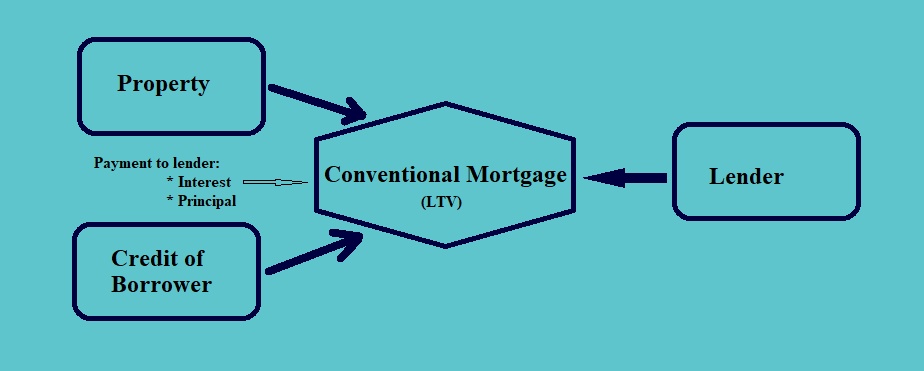

a. Residential mortgage loans are the loans against the residential properties for the purchase of the same taken for a very long period (of usually 10-30 years).

b. In these transactions, the borrower pledges the property and credit of the borrower to the mortgage of the lender and receives the loan to purchase the same property. The loan is received by the borrower at a certain percentage of the value of the property, usually called the ratio of loan-to-value (LTV). The borrower has to make the periodic payments of the interest and principal to the lender. They also have the option to make the prepayments ahead of the scheduled The prepayments could also be made in full or for a partial value.

1.1. Prepayments

a. The prepayments result in the amount and the timing of the cash flows becoming uncertain for the lender. Thus, it creates a prepayment risk for them. Therefore, in residential mortgage loans, there are different clauses for the prepayments.

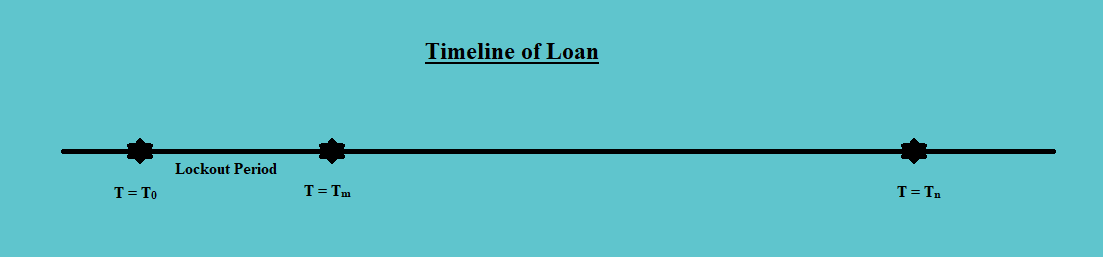

b. Consider the following timeline:

In the above figure, assume that the loan is taken for a period of ‘n’ years. There would be a schedule for the periodic repayment of the loan each period up to n years. However, the borrower may choose to make a prepayment of such loan amount, creating a prepayment risk for the lender.

c. In order to curb such a risk, the lenders usually fix a period for say ‘m’ years starting from the day the loan is made. This period is called the lockout period. During this period, the borrower cannot make any prepayments. If they do so, they would attract a penalty.

d. After this lockout period, the prepayment can be made without a penalty. Or else, if the prepayment made exceeds a certain amount then the penalty for prepayment is imposed.

e. The prepayment penalty is imposed as a multiple of month’s interest lost.

1.2. Interest Rate Determination

a. Based on the interest rate payments, the mortgages may be:

i. Fixed-Rate, Level Payment, or Fully Amortizing Mortgages;

ii. Adjustable Rate Mortgages or ARMs (These mortgages fix the ceilings and the floor for the amount of interest that can be paid); or

iii. Others such as initial period fixed and then floating, with low teaser plus a higher reset rate, convertibles (from fixed to floating, or vice-a-versa).

b. Depending upon the interest rate structure, each of the loans has an amortization schedule. For example, for a fixed rate, level payment, and fully amortizing mortgage, the amortization schedule can be made by finding the annuity value of the future payments that would result in a present value of the loan equaling the mortgage value.

c. During the lifetime of the loan, in the initial years, the ratio of interest to the principal in the annuity payments is higher, and this ratio keeps on decreasing as the loan approaches its maturity.

d. The rights of the lender are usually stated in the foreclosure. Depending on the rights, a loan may be recourse or non-recourse. In a recourse loan, all the assets of the borrower can be used to make the lender whole. In the non-recourse loan, the borrower may, however, walk away.

1.3. Credit Guarantee Sectors

a. Based on the credit quality, the mortgage-backed securities (MBS) can be classified into either Agency MBS or Non-Agency MBS.

b. The Agency MBS are more secured Mortgage-Backed Securities. They have a higher credit guarantee as they are issued by:

i. The federal agency such as Government National Mortgage Association or GNMA, or

ii. The government-sponsored agencies such as Federal National Mortgage Association (FNMA) or Federal Home Loan Mortgage Corporation.

c. The non-agency MBS are mainly issued by the banks.