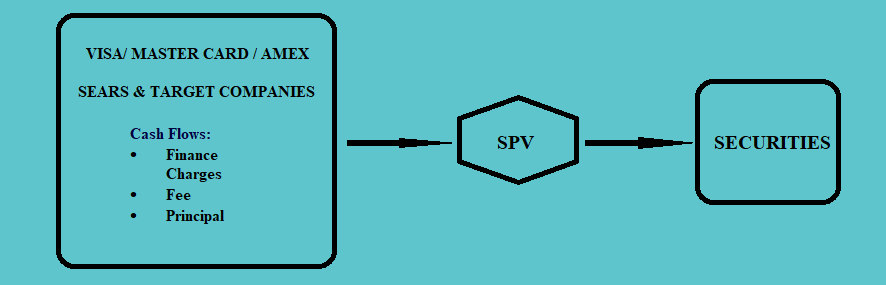

a. For these securities, the assets, i.e. receivables from the issue of credit card are pooled together and securities are issued against them.

b. For holders of CARDS, the interest is paid monthly, and the principal is not amortized. The principal payments made by the credit card borrowers are retained by the trustee for a specified period known as lock-out period or revolving period to be reinvested in additional receivables. The lock-out period varies from 18 months to 10 years.

c. The period after the lockout period during which the principal is paid to the investors is called the principal amortization period. The different structures used in the amortization of credit card receivables are:

i. The pass-through structure,

ii. The controlled-amortization structure, and

iii. The bullet-payment structure

In the first case, the principal cash flows from the credit card accounts are paid to the security-holders on a pro-rata basis.

In the second case, a predetermined principal amount is set at a very low level so that the obligations are met even under certain inadvertent conditions. The investor is paid the predetermined principal amount or the pro-rata amount, whichever is less.

In the third case, the investor receives the full amount at one time, but there is no guarantee that the amount will be paid in full. Some portion of the principal is deposited monthly into the account by the trustee. The account will generate interest to make periodic interest payments and will accumulate principal to be repaid in a lump sum.

d. There may be situations under which the amortization of principal has to be done earlier before the completion of the lock-in period. In such situations, provisions that are made are referred to as “early amortization or rapid amortization”. The primary purpose of this provision is to safeguard the credit quality of the issue. When this early amortization provision is activated, the cash flows will be altered.

The situations under which this may occur are:

i. Default of the servicing party,

ii. Inability of the trust to generate income to pay for the coupon and the servicing fee,

iii. Decline in the credit support below a particular level, and

iv. Violation of the agreements by the issuer regarding pooling and servicing.