a. Credit analysis is an assessment of the issuer’s ability to pay the obligations of interest and principal repayments. It is the financial analysis used for determining the creditworthiness of an issuer using various quantitative and qualitative factors.

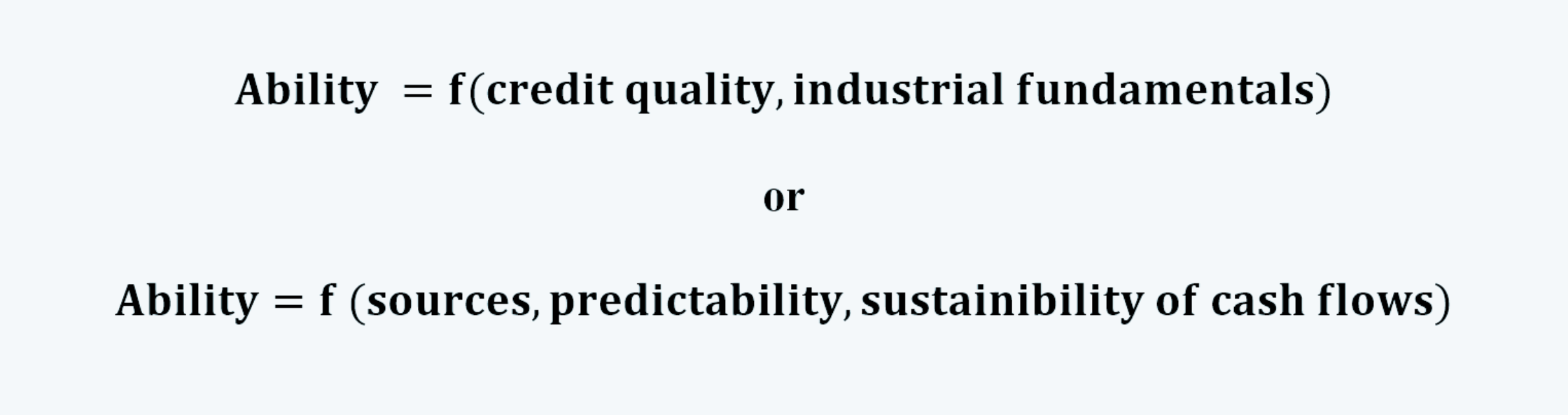

b. The ability to pay an issuer is the function of credit quality and the industrial fundamentals. Or, to say, it is the function of the sources, predictability, and sustainability of the cash flows.

1.1. 4 C’s of Credit Analysis

The four C’s of credit analysis are: Capacity, Collaterals, Covenants, and Character.

1.1.1. Capacity

a. The capacity is the capability of the borrower to repay the debt. It reflects the volatility in the borrower’s earnings.

b. If the repayment of debt contracts proves to be a constant stream over time, but earnings are volatile (and thus have a high standard deviation), it’s highly probable that the firm’s capacity to repay debt claim s would be at risk.

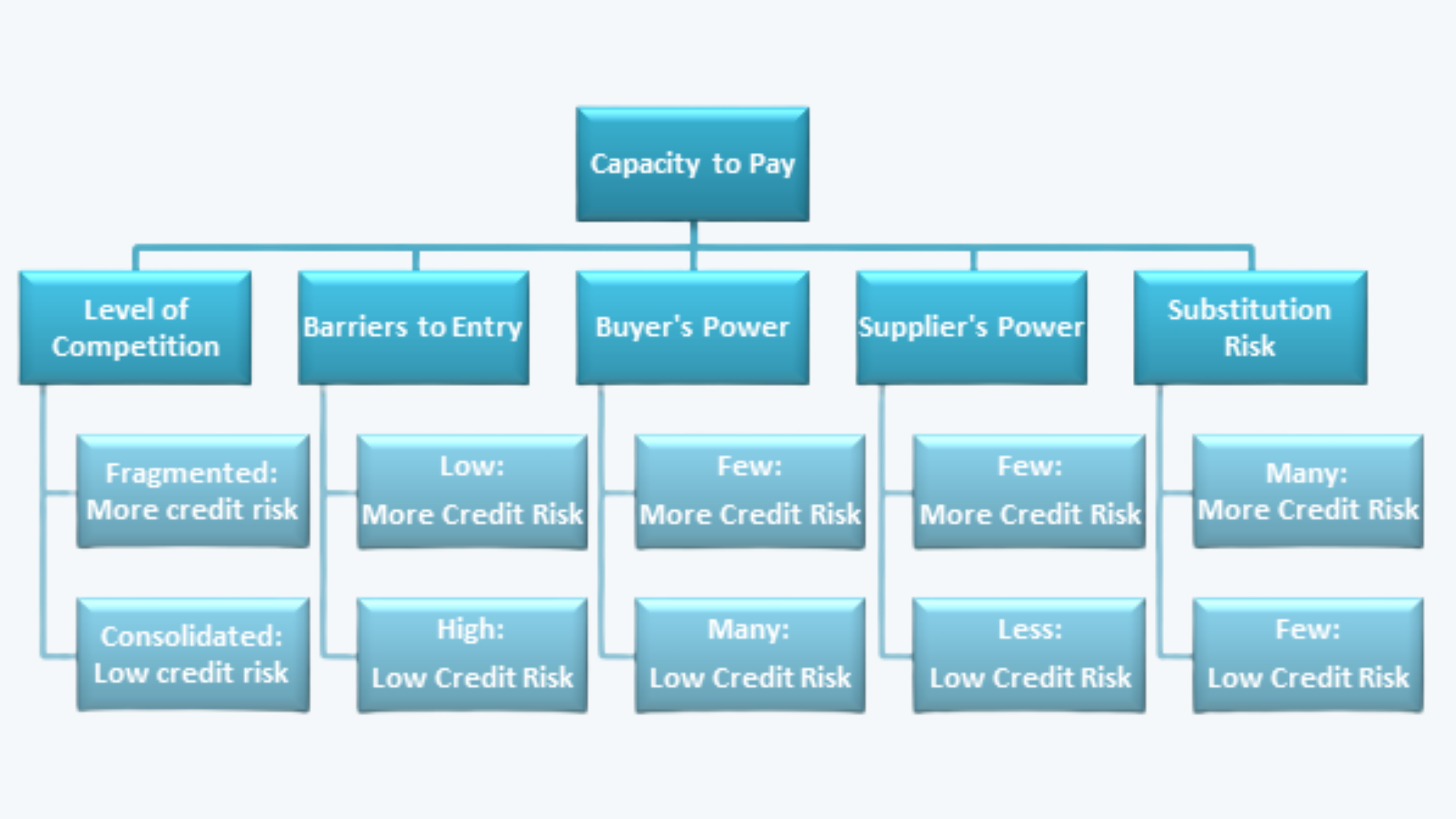

c. The capacity to pay can be determined using both industry and company analysis.

d. The industry analysis can be done using Porter’s Model, which basically has 5 factors that determine the level of credit risk faced by the securities. These factors are:

i. Level of Competition

ii. Barriers to entry

iii. Power of the buyer

iv. Power of the supplier

v. Substitution risk

The following figure shows how the above-mentioned factors affect the credit risk:

e. There are companies with fixed cost structures, and there are others with variable cost structures. The companies with the fixed cost structure have higher credit risk due to low liquidity and high fixed cost coverage, in comparison to the companies with the relatively variable cost structure.

f. One can also have a fair idea of the capacity from the fundamental analysis of the company and the industry.

One can look at the cyclicality of the industry. The companies belonging to the non-cyclical industries have lower credit risk in comparison to the companies from the cyclical industries, due to the steadiness of the cash flows.

One can also do an analysis of the growth prospects of the company, and also refer to the published industry statistics to identify the credit risk.

g. After the industry analysis, the analyst can also look into the company’s statistics to make inferences about the company’s capacity to pay.

One should look into the company fundamentals such as:

i. competitive positions,

ii. track record or operating history

iii. management strategies and execution

iv. ratio analysis (including profitability and cash-flow analysis, leverage ratios, coverage ratios, etc.)

h. Different ratios that can be analyzed are:

i. Profitability and Cash Flow Ratios: The important profitability and cash flow ratios that can be analyzed are:

# EBITDA

# FFO (Funds From Operations)

# FCFE (Free Cash Flow to Equity)

ii. Leverage Ratios: While calculating the leverage ratios for analysis, the debt should include the debt-like liabilities, such as leases. The important leverage ratios that can be calculated are:

# Debt/Capital Ratio

# Debt/EBITDA

# FFO/Debt

iii. Coverage Ratios: These ratios measure the company’s ability to meet interest payments. Some of the important coverage ratios that need to be calculated are:

# EBITDA/Interest Expense

# EBIT/Interest Expense

1.1.2. Collaterals

a. In the event of default, a lender has the claim on the collateral pledged by the borrower.

b. The greater the proportion of the claim over the assets and the greater the market value of the underlying collaterals, the lower is the remaining exposure risk in the case of a default.

c. The main focus in the analysis of collaterals is on estimating the exposure due to the inability to recover the losses. It mainly involves the estimate of the market value of the tangibles and the intangible assets, underlying the issue.

1.1.3. Covenants

a. These are the agreed terms and conditions between the borrower and the lender.

b. There are two types of covenants that can be seen in lending agreements, i.e. the affirmative covenants and negative covenants.

c. The affirmative covenant is the promise of the borrower to meet certain promises like paying interest, principal, taxes, etc.

d. The negative covenant is the restriction to the borrower regarding what actions are prohibited.

e. The covenants are mostly listed in the bond’s prospectus.

1.1.4. Character

a. It is the measure of the firm’s reputation, its willingness to repay, accounting policies, tax strategies, and credit history.

b. In particular, it has been established empirically that the age factor of an organization is a good proxy for its repayment reputation.

c. The history of business and the experience of its management are critical factors in assessing a company’s ability to satisfy its financial obligations.

1.2. Credit Risk Vs. Return

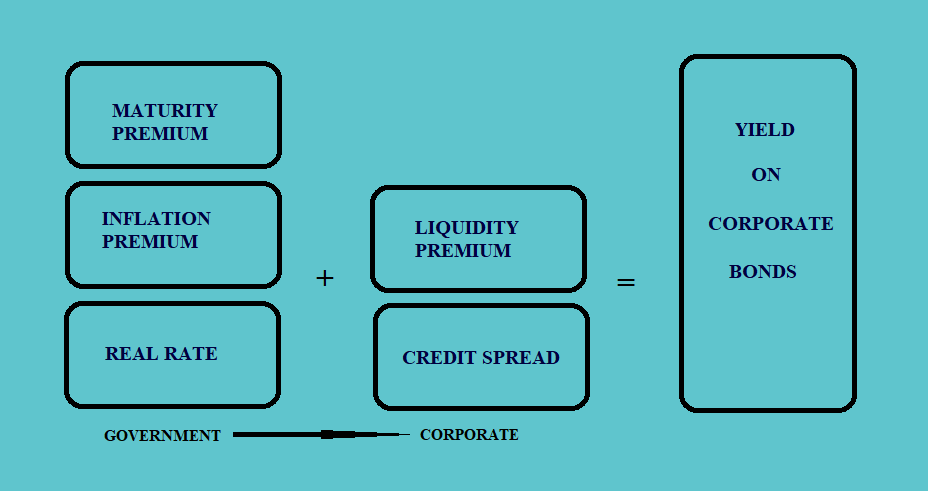

a. There is always a trade-off between the risk and return for all investments. Thus, if a bond is having a higher credit risk, it will also be accompanied by a higher potential return to compensate for the high volatility and lower certainty of cash flows.

b. The total return on any bond consists of premiums for different costs and opportunities foregone. This can be explained with the help of the following:

The government bonds offer a premium for inflation and maturity over and above the real rate. However, the corporate bonds have to pay the premium in the form of credit spread as well as on the liquidity risk over the yield on the government bonds.

c. The spread on the corporate bonds, over and above the yield on a government bond is affected by the following factors:

i. credit cycle

ii. broader economic conditions

iii. financial market performance

iv. market-making willingness (i.e. efficient over-the-counter market)

v. supply and demand

d. The spread risk results from the changes in return due to changes in the spread. It can be calculated using the following formula:

(This is discussed in details in the previous chapter)