1.1. Bond Prices & Interest Rates

a. The bond prices and the interest rates are inversely related to each other. Thus,

i. The price of the bonds increases as the rate of interest falls; and

ii. The price of the bonds falls as the interest rate rises.

b. For the same coupon and time to maturity, the percentage change in price as the interest rates fall is usually greater than the percentage change in price as the interest rates increase. That is:

| |%∆P| as r ↓ > |%∆P| as r ↑ |

Thus, the prices are more volatile on the upside for the percentage change in rates.

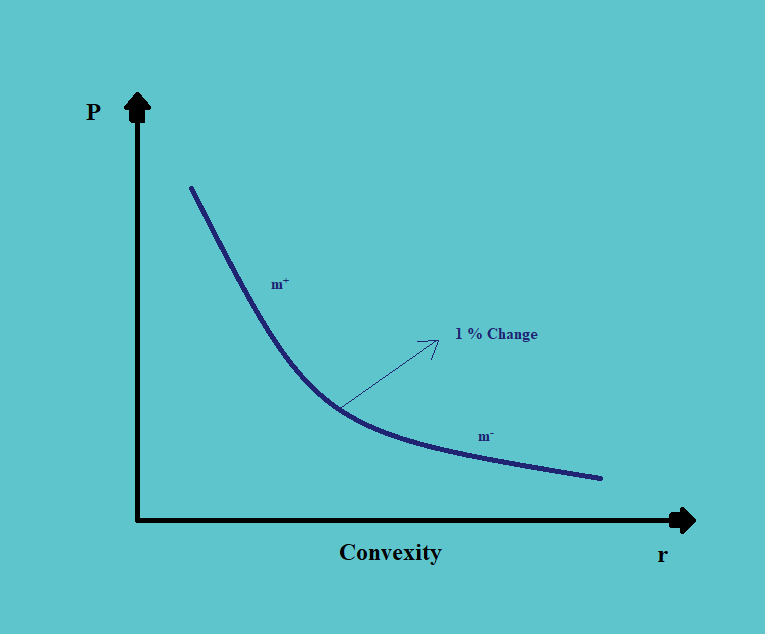

This results in convexity in the relationship between the price of the bond and the interest rates. Look at the following graph:

In the above graph, we have taken interest rates on the x-axis and the price of the bond on the y-axis. We can see that the slope of the curve above (for the higher prices) is greater than the slope of the curve below, for the lower prices. This results in the convexity in the interest and price relationship.

1.2. Bond Price and Coupon

a. At the same time to maturity, the lower coupon bonds have more price volatility than the higher coupon bonds.

b. For the same coupon bonds, the longer-term bonds have more price volatility than the shorter-term bonds, for a one percent change in interest rates.

c. Thus, if there is an expectation of a fall in interest rates,

#. it is advisable to move to longer-term bonds with lower coupons.

d. And, if there is an expectation of an increase in interest rates,

#. it is advisable to move to short-term bonds with a higher coupon.

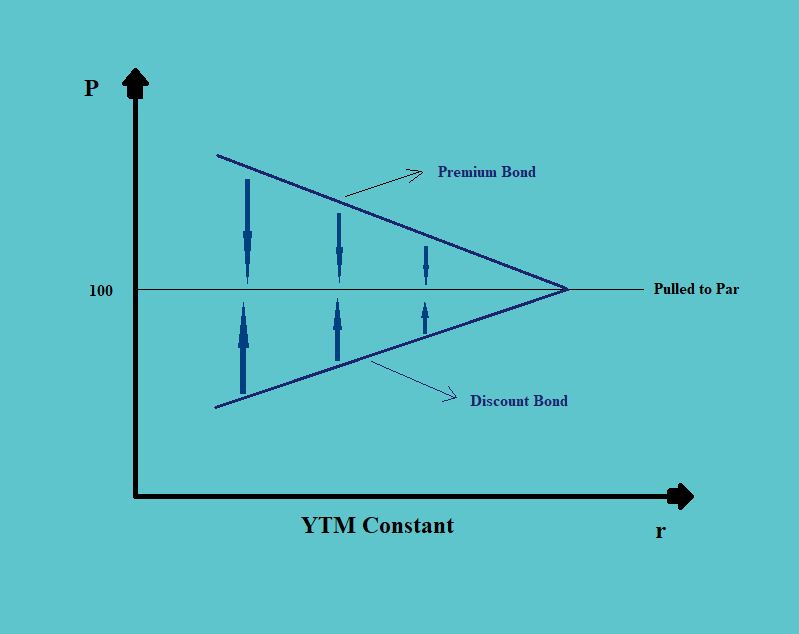

e. Look at the following figure:

In the above figure, we can see that in the long run, as the bond approaches maturity, the prices of the bonds are pulled to par, and the volatility in the prices decreases; if the yield-to-maturity is constant.