a. Monetary and fiscal policy use different channels to affect the economy but may have similar policy objectives.

i. These policies may conflict with one another, or they may enhance one another.

ii. Because of the potential for monetary and fiscal policies to work against each other, coordination between the government and the central bank is important.

iii. Both types of policies are challenging because of lags in data and the inability to predict the future path of the economy.

b. Easy or tight fiscal and monetary policies have a different impact on aggregate demand and interest rates in the economy.

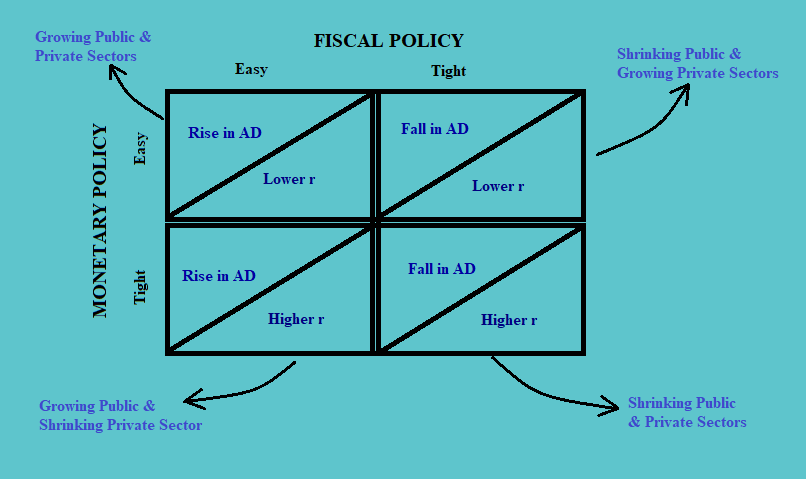

i. Easy fiscal policy results in a rise in aggregate demand.

ii. Tight fiscal policy results in a fall in aggregate demand.

iii. An easy monetary policy lowers the interest rates.

iv. A tight monetary policy raises the interest rates.

Thus a different combination of easy and tight fiscal and monetary policy has a different impact on the economy. This can be explained with the help of the following matrix:

Results of a different combination of fiscal and monetary policies are as follows:

i. A combination of both easy fiscal as well as monetary policy results in growth in both private and public sectors, as it induces more expenditure on durable goods. This is a highly expansionary policy.

ii. A tight fiscal policy and monetary policy results in shrinking public and private sector growth. This is a highly contractionary policy.

iii. A tight fiscal policy and an easy monetary policy result in a shrinking public sector and a growing private sector. There are mixed results.

iv. A tight monetary policy and an easy fiscal policy, on the other hand, results in a shrinking private sector and a growing public sector. There are mixed results.

1.1. National Debt

a. While formulating any fiscal or monetary policy, the policymakers have to choose between deficit or debt.

i. When the revenues in an economy are more than the expenditure, it is called the deficit. It could be financed by selling the bonds.

ii. The accumulation of all unpaid deficits is called debt.

b. To analyze the severity of the situation, we can calculate one of the two ratios:

i. Debt-GDP Ratio, or

ii. Interest Payments-GDP Ratio.

c. Interest payments to GDP ratio is a better measure of serviceability of the interest payments.

d. If the real GDP growth is less than the real interest rates, then the change in tax revenue is less than the interest payments. And this makes the ratio of debt to GDP even worse.

e. Following are the reasons for no concerns regarding national debt:

i. Much of a nation’s debt is owed internally.

ii. Some of the debt may have been incurred to finance capital projects or to enhance human capital, which should contribute to the growth of the economy.

iii. Large deficits may encourage changes in tax laws, which may contain distortions.

iv. Private sector saving may increase.

v. If there is unemployment, debt is not taking funds from productive uses.

f. Following are the situations which make national debt a concern:

i. A high debt-to-GDP ratio may lead to higher taxes and hence disincentives.

ii. Lack of confidence in the government may exist, making some policies ineffective.

iii. Government borrowing diverts funds from more productive uses (referred to as crowding out).