Before we discuss different types of policies being followed by the central bank, we need to understand, what constitutes the important characteristics that promote the effectiveness of these policies.

1.1. Characteristics of Effective Central Banks

a. Independence: Central banks are often independent of the government, but the degree of independence varies among nations.

i. The central bank should be independent operationally, to target the rates without any influence.

ii. It should also be free to define inflation. They should have the independence to set the targets.

b. Credibility: The credibility of central banks is necessary for the efficient execution of monetary policy. There should not be any competing incentives in the hands of the employees of the central bank.

c. Transparency: There should be complete transparency concerning the data based on which the decisions are taken by the central bank, and the forecast on growth and inflation should be published.

1.2. Policies

a. Inflation Targeting: Central banks attempt to bring price level stability in the economy by targeting the inflation levels in the economy.

i. Unexpected inflation is considered costly because it is not factored into wage negotiations and contracts, and the uncertainty regarding inflation can affect (and exacerbate) the business cycle.

ii. Inflation targeting is the maintenance of price stability using monetary policy.

iii. Most of the central bank’s target inflation level is around 2% per annum for a horizon of up to 2 years.

iv. In developing nations, there are challenges to price stability, e.g., illiquid government bond market, changing the economy, changing the definition of money supply, and lack of credibility, etc.

b. Exchange Rate Targeting: This type of targeting is used by some countries.

i. Exchange rate targeting requires setting a band for the target exchange rate against a major currency.

ii. The central bank buys and sells foreign currency toward the goal.

iii. There is a risk involved in the exchange rate targeting, i.e. the speculators may trade against the monetary authority.

1.3. Types of Policies

a. The monetary policies of the government / central banks can be categorized into two categories, i.e. expansionary policy and contractionary policy.

b. Whether a policy is expansionary or contractionary, depends on the target interest rates.

c. The neutral rate is the rate that neither spurs nor slows down the economy. It is the average policy rate over the business cycle.

d. Any rate above the neutral rate will be described as the contractionary policy. Whereas, any rate below it will be described as expansionary monetary policy.

e. This is mainly because; a higher interest rate would mean lower demand for money and thus lower demand for goods and services. Similarly, a cut in the target rate means an increase in the liquidity in the system which increases the rate of growth in the money supply and the real economy.

f. The interest rates are made up of two components:

i. The real interest rate, which is the real trend growth of the underlying economy; and

ii. The inflation component, which is the long-run expected inflation, is generally set by the central bank of the country as the target inflation.

1.4. Limitations of Monetary Policy

1.4.1. Problems in Transmission Mechanism

a. The most basic problem with the monetary policy may arise in its transmission mechanism.

b. Here, the channels such as asset prices, interest rates, expectations, and exchange rates may not act as efficient means of targeting the inflation rate in the economy.

c. A liquidity trap is an example of a problem in the transmission. A liquidity trap occurs when market participants hold large cash balances, so changes in the money supply will not affect real activity. Hence, the policy changes are ineffective in bringing the desired changes.

1.4.2. Deflation

a. Another limitation of the monetary policy is that it cannot handle the situation of deflation.

b. This is mainly because; the central bank can only reduce the target rates down to 0% and not below that.

c. Deflation has the following effect on the economy:

i. It raises the real value of debt.

ii. It may also result in delays in consumption because people expect an increase in the value of their goods and currency. Therefore, they prefer to hold them rather than consume them.

d. This leads to the deflationary pressure building up and the economy entering into the spiral of deflation.

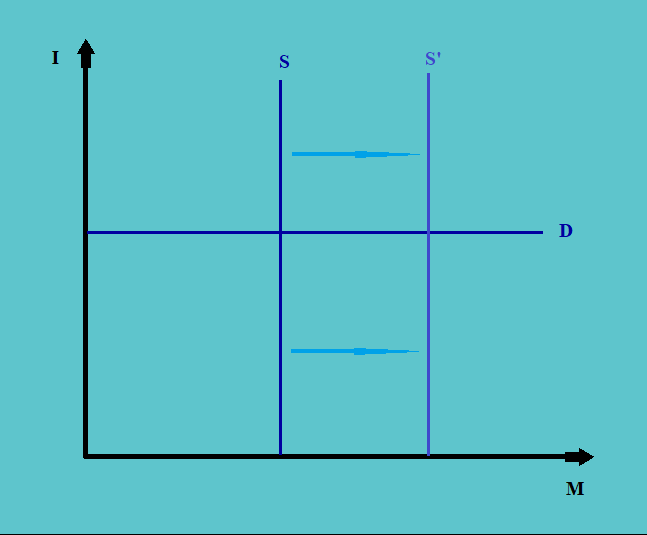

e. Another effect of this deflation is that it may result in the demand curve becoming a horizontal straight line.

This is mainly because, the expectations of an increase in the value of currency motivate people to hold the same, and the changes in the supply of money do not have any impact on the same.

f. So the policy mechanism that can help ease such a situation is quantitative easing (QE), which is an increase in money supply intended to stimulate the economy. This helps in decreasing the long rates since the short rates cannot be changed much.

g. QE can take different forms (e.g., purchase of specific securities, such as mortgage bonds).

h. A risk of QE is that if the securities with credit risk are purchased, the central bank is taking on significant risk.