a. The forward exchange rates are quoted in terms of points, also commonly known as pips (i.e. points in the percentage). The points are mostly quoted as 1:10000. The forward rates can be quoted as a number of pips from the spot rate or as a percentage of the spot rates.

b. If the forward rate is more than the spot rate, the base currency is said to be trading at a forward premium.

c. For example, suppose the A/B spot rate is 1.1500, and that the one-month forward premium is 50 pips. Therefore, the forward rate is:

Forward Rate = 1.1500 + (50/10000) = 1.1550

d. If the forward rate is quoted in terms of percentage, say the spot rate is 1.2500 and it is quoted at a 0.5% premium, the forward will be:

Forward Rate = 1.2500 × 1.0050 = 1.25625

e. On the other hand, if the forward rate is less than the spot rates, the base currency is said to be trading at a forward discount.

1.1.1. Arbitrage Using Forwards

a. We can explain the process of making arbitrage profits using an example.

b. Suppose an investor has X amount of money to be invested.

c. If the interest rates on his domestic currency are id, after the investment period he will receive the amount of investment plus the interest earned, that is:

X (1 + id)

d. Alternatively, the investor can convert the local currency into a foreign currency at the spot rate Sf/d and invest the same in a foreign country, where the interest rate is if. By doing so he will have the following amount of foreign currency with him:

X × Sf/d (1 + if)

e. The investor can get back the money by converting the same into domestic currency by dividing the same by the forward rate:

[X × Sf/d (1 + if)] / Ff/d

f. Now, if the return from investing in the domestic currency was equal to the return earned through investing in the foreign currency, there would not be any arbitrage opportunities.

g. So, there would not be any arbitrage opportunities if:

X (1 + id) = [X × Sf/d (1 + if)] / Ff/d

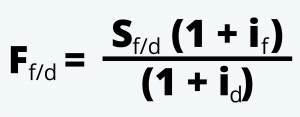

Solving the above equation for the forward rates, we get:

h. Thus, for an arbitrage opportunity to exist,

i. Example:

i. Suppose the spot exchange rates of two currencies (Sf/d) is 1.5000 and the interest rates in the domestic country (id) are 4% and that in the foreign country (if) is 5%.

ii. Then the no-arbitrage forward rates would be:

Ff/d = [1.5000 × (1 + 0.05)] / [1 + 0.04] = 1.5144

iii. Thus, we can say that the forward is trading at 144 pips.

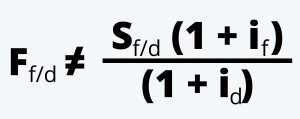

iv. Now, if the forward rate was 1.6000 instead, this means that the price of the foreign currency is overstated in the forward market.

v. Therefore, the best the investor can do is go long on the domestic currency and short on the foreign currency. He can do this by borrowing 1.5000 of the foreign currency and convert the same into one unit of the domestic currency and sell the same in forward market at 1.6000.

vi. By investing in the domestic currency at the interest rate of 4% he receives 1.04 (i.e. 1.00*1.04) at the end of the period.

vii. Had, he invested in the foreign market and converted the same back into domestic currency, he would have received 0.9844, which is less than the amount he earned by investing in the domestic market.

j. So the general rule for the forward pricing is:

i. If the base currency is the higher-yielding currency then the forwards for the same will trade at a discount.

ii. And, if the base currency is the lower-yielding currency, the forwards will be at a premium.