a. There is an inverse relationship between the trade balance and the capital account. When there is a trade surplus or deficit, exchange rates, and prices change, which offsets the effect of the financial flows out of or into a country. For example, if there is a trade deficit, foreign capital flows into the country.

b. Thus, the net effect of imports and exports affects a country’s capital flows:

Trade deficit → Capital account surplus

Trade surplus → Capital account deficit

c. Using the relationship of the national account, we see the relationship between trade and expenditures/savings and taxes/government spending:

(X – M) = (S – I) + (T – G)

Here, (X-M) i.e. exports minus imports, represents current account trade surplus or deficit. S represents private savings (i.e. Sp) and T-G (i.e. taxes less government savings) represents fiscal surplus or deficit (i.e. Sg).

d. Rearranging the above terms, we get:

Sp – Sg = CA + I

e. The potential flow of financial capital in or out of a country is mitigated by changes in asset prices and exchange rates.

f. There are two major theories on the exchange rate/trade relationship, i.e. Marshall Lerner’s theory and The Absorption Approach.

1.1. The Marshall-Lerner Theory

a. Before we discuss this theory, recall the formula for the elasticity of demand, which is:

ɛ = – (%∆Q) / (%∆P)

b. The Marshal-Lerner theory states that:

wxɛx + wm (ɛm – 1) > 0

Where:

i. wx = X / (X+M) or the weight of exports in foreign trade,

ii. ɛx is the price elasticity of foreign demand for exports,

iii. wm = M / (X+M) or the weight of imports in foreign trade, and

iv. ɛm is the price elasticity of domestic demand for imports.

The term wxɛx assumes that the exports are billed in the domestic currency and that the price of a domestic currency is unchanged. Whereas, the term wm (ɛm – 1) assumes that the imports are billed in foreign currency.

c. So, if the above condition holds, the FX rate management will have an effect on the trade balance.

d. So if the weight of imports is higher than the weight of exports (i.e. a trade deficit), then the FX rates devalue and depreciation will help to get the weights of exports equal to the import’s level.

e. Thus, the effectiveness of currency devaluations or depreciation on trade depends on the price sensitivities (that is, price elasticities) of the goods and services.

i. If the goods and services are highly elastic, trade responds to devaluation or depreciation, improving the trade balance

ii. If the demand for exports and imports is price inelastic, trade is less responsive to devaluation or depreciation.

f. The FX rate changes will be more effective for trade adjustment if, the exports and imports have:

i. have substitutes,

ii. trade in competitive markets,

iii. are luxury goods rather than necessities, and

iv. are the goods that represent a large portion of consumer expenditure.

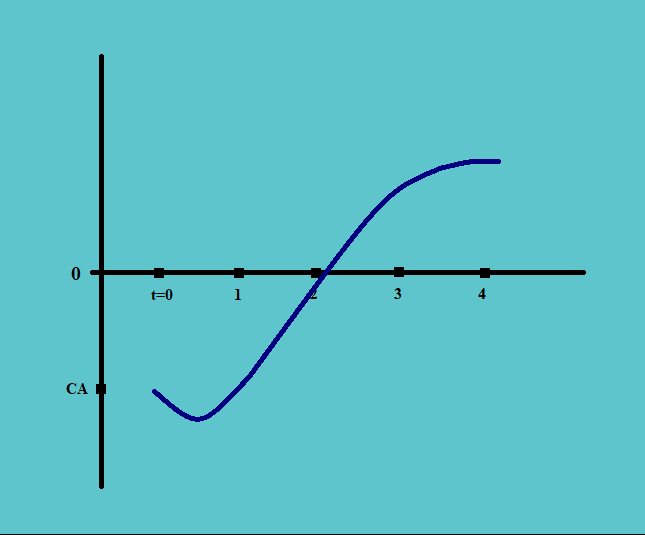

g. The pattern followed the consumers to change the behavior pattern exhibits the J-Curve pattern, as follows:

According to this theory, in the short-run, if there is a current account deficit and the FX rate declines as a result, but the elasticity of demand is less than 1. The consumers need time to change the behavior, therefore the deficit worsens.

In the long run, however, consumers respond to the change in relative prices, and there is an increase in the current account balance as a result. The shape of the curve forms the shape of J.

1.2. The Absorption Approach

a. Consider the statement for national income:

Y = (C + I + G) + (X – M)

In this equation, we name the term (C+I+G) as A, representing the total absorption in the economy. And, the term (X-M) is B, representing trade balance.

b. Thus,

Y = A + B

or,

B = Y – A

Thus, if Y-A is greater than 0, then there is a trade surplus and if Y-A is less than 0 then there is a trade deficit.

c. In order to improve the trade balance, we need to:

i. Increase incomes/output, and/or

ii. Reduce absorption.

d. This affects national income through the wealth effect. The reduced purchasing power of domestic-currency-denominated assets leads to lower expenditure and increased saving boosting the marginal propensity to save.

e. A lower FX rate will shift demand to domestic goods and services if there is any excess capacity.

f. If the marginal propensity to consume is less than 1, output rises faster than absorption, therefore trade balance improves.