1. Price Multiples

a. Price multiples are the ratios that compare the share price with some sort of money flow or value.

b. The monetary flow can be in the form of earnings, sales, or cash flows. The value multiples, on the other hand, can be in the form of book value.

c. Some of the common price multiples and their respective formulas are:

|

Price Multiple Ratios |

Formula |

Advantages of this ratio |

Disadvantages of this ratio |

|

Price-Earnings Ratio (P/E Ratio) |

P0 / (EPS) |

· Easy to use; · Most common measure for appropriateness of price of the stock; and · Strongly correlated to long-term returns |

· Useless if the EPS is less than zero; · Useless if the earnings are volatile; and · Earnings are just an accounting measure and not the economic measure of the profitability of a company. |

|

Price-Sales Ratio |

P0 / (Sale per share) |

· This multiple is less affected by the accounting choices made by the management, thus less biased. · This is a better metric if the EPS is less than zero. |

· The management bias may still creep in, as the revenue recognition issues still apply to this method as well. · This method ignores the cost structure of the company. |

|

Price-Cash Flow (P/CF) Ratio |

P0 / (Cashflow per share) |

· This is a better economic measure than just being a mere accounting measure. · The cash flows are more difficult to manipulate, thus less subject to any sort of bias. · The cash flow tends to be less volatile than the EPS. · This multiple is more reliable in the longer run. |

· This method ignores the non-cash revenues. |

|

Price-Book Value (P/BV) Ratio |

P0 / (Book Value Per Share) |

· This is a more stable measure. · This multiple can also be used even if the EPS is negative. · This multiple is more appropriate for the firms in distress |

· This method ignores the relative asset size in comparison. · The book value is generally equal to the market value. |

d. These ratios are calculated for the required companies or stocks and compared with the specified value such as the industry standards, historical data, etc. If the ratio is less than the specified value, the stock is considered as undervalued; if it is equal to the specified value, the stock is valued fairly; and if it is greater than the specified value, the stock is considered as overvalued.

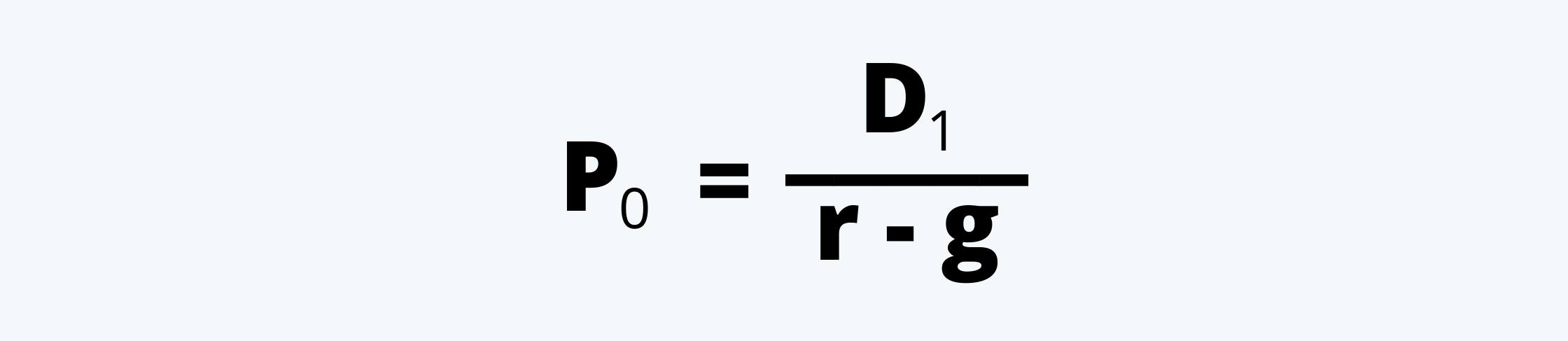

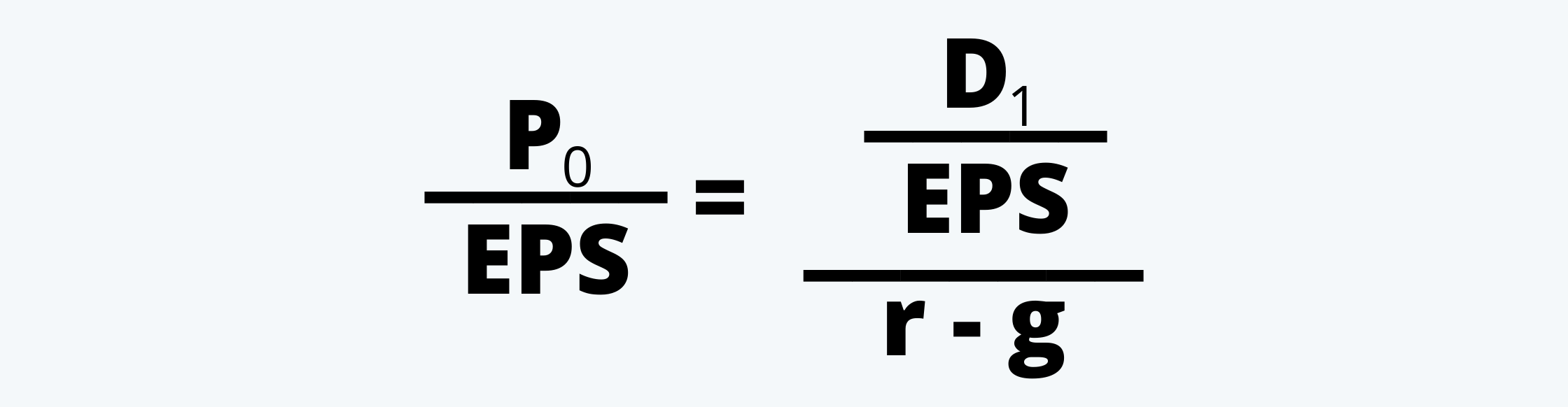

e. We know that as per Gordon’s Growth Model,

Now, for a stock to be considered fairly valued, its intrinsic value i.e. V0 should equal its market price, i.e. P0. Therefore,

If we divide both sides by EPS, we get:

Here, is the P/E multiple and represents the dividend payout ratio (or DPR).

Thus, to be considered fairly price or justified,

This is also called the justified P/E ratio.

e. So, if we go by the above equation, the P/E multiple is positively related to:

i. DPR (This is only if we strictly go by the formula or the above equation of P/E multiple. In reality, however, the higher the DPR, the lower is the retention and the re-investment rate; so there is a dividend displacement of earnings.)

ii. g. Thus, the closer the growth rate is to the required rate of return, the higher is the price and thus a higher P/E multiple.

f. The P/E multiple is negatively correlated to the required rate of return on equity.

g. The analyst can choose the best-suited multiple for a company or a stock. He may even choose to have multiple, multiples and then compare them with a benchmark value, typically called the ‘comps’.

This benchmark value can be obtained from:

i. the values of a closely matched individual stock,

ii. average values of the peer group or the industry,

iii. average multiple derived from the trend or the time-series analysis.

The main rationale behind comparing the multiples of one company with the benchmark is the ‘Law of One Price’. According to this law, identical assets should sell for the same price.