a. There are basically two types of orders, i.e. bid order and ask order.

b. The bid rate is the rate at which the dealers and traders are ready to buy, and an ask rate is a rate at which they are ready to sell.

c. The bid-ask spread is the simple difference between the selling price and the buying price of the asset. In the foreign exchange market, the bid-ask spread is the dominant source of dealer’s income.

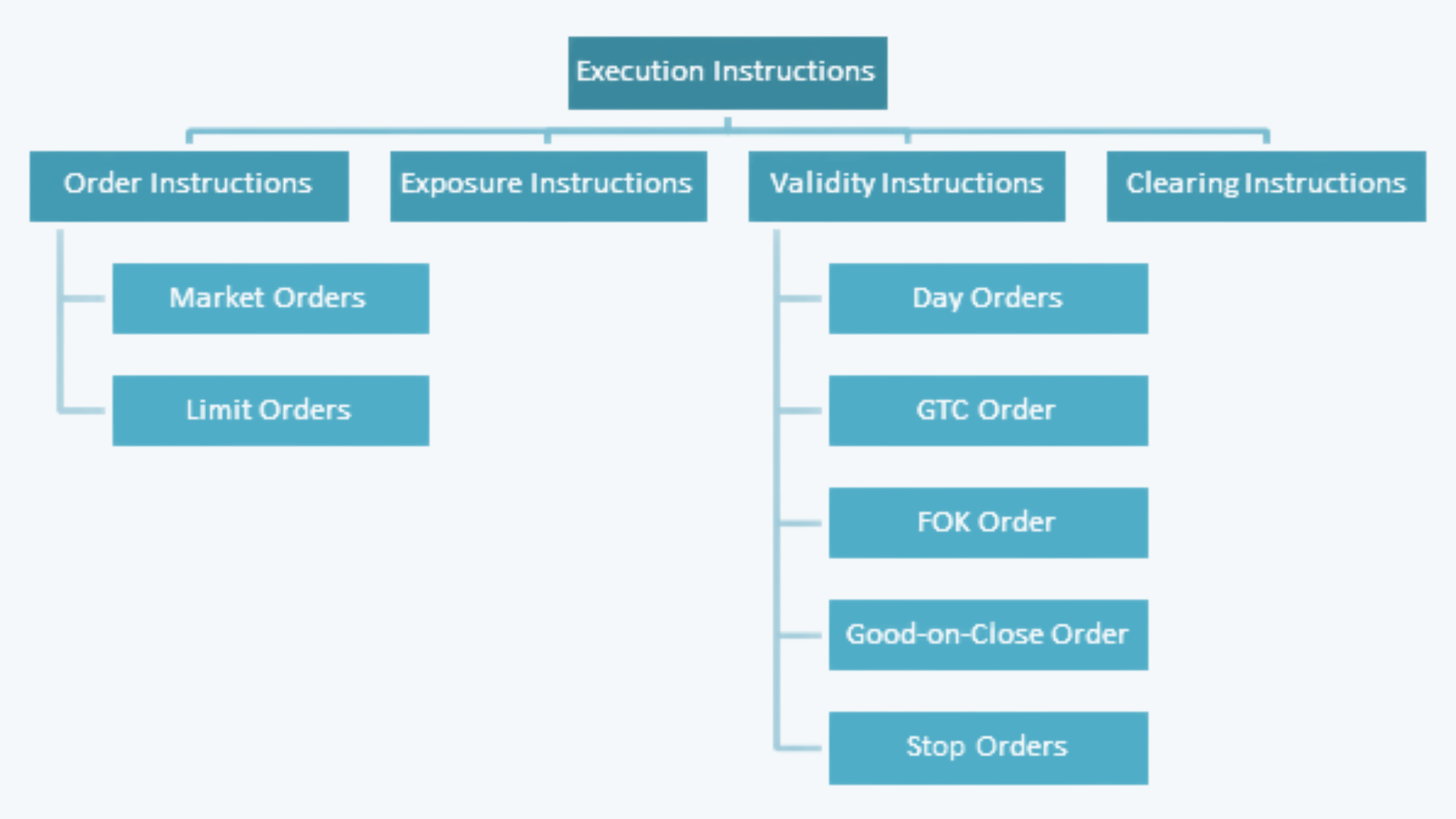

1.1. Execution Instructions

Execution instructions are the instructions as to how the market orders should be filled. They could be in the form of ordering instruction, exposure instruction, or validity instruction, etc.

1.1.1. Order Instructions

Some of the ordering instructions are:

a. Market Order. It is the order to buy or sell the assets at the best current market price. Market orders provide immediate liquidity to the market. The investors who want to buy/sell the stocks instruct the broker to make the trade at the lowest/highest price available in the market. The investors may be unaware of the prices at which the stocks would be traded.

In the market orders, the execution of the trade is guaranteed, but the price at which it would be executed is not guaranteed.

b. Limit Orders. In the limit order, the investor specifies the limit at which he would like his stock to be traded. The buyer would specify the maximum limit at which the stock would be bought by the broker. Thus the broker has the choice to buy the stock at the specified limit or lower than that. Similarly, the seller can also specify the maximum limit, below which the stock cannot be sold.

In the limit orders, the price guarantee is there, but the guarantee of execution of the order is not there.

So, if an investor is buying the securities, he could place the limit order in the following ways:

i. If the limit is put above the ask rate it is considered as a marketable limit order and can be filled at least partially.

ii. If the limit is put between the bid and ask rate, it creates a new market, as it is still below the current market rate.

iii. If the limit is put at the current bid rate, it makes the market. The chances of the order being executed depending upon the size of the order and all the buy orders placed at this price would be executed before the latter one is executed.

iv. If the limit is put below the current bid rate, it is behind the market and will be executed only if the price drops.

1.1.2. Exposure Instruction

a. Here the instructions are given by the investors, whether to display or hide the order on the exchange.

b. The orders could be fully hidden; in this case, only the brokers and exchanges can see your order.

c. The orders can also be partially hidden, where the display size of the order is lower than the actual order size. These are also called the iceberg orders.

d. The orders are mainly hidden from the market, just so that, after knowing the large size of the order, the price is not pulled up.

1.1.3. Validity Instructions

These are the instructions as to when an order may be filled. Some of the major validity instructions are:

a. Day Orders. Day orders remain valid only during the specified day on which the order is placed. Generally, all the market orders are placed as day orders only. The underlying assumption behind such an order is that the market, economic and industry conditions may change; thus investment should be specified for a particular day only.

b. Good-Till-Cancelled (GTC) Order. This order remains in the system until it is canceled by the trading member. It will therefore be able to span trading days if it does not get matched. The maximum number of days a GTC order can remain in the system is notified by the Exchange from time to time; but it remains for a maximum period of 6 months, typically.

c. Fill-or-Kill (FOK) Order. This order allows the trading member to buy or sell security as soon as the order is released into the market, failing which the order will be removed from the market. A partial match is possible for the order, and the unmatched portion of the order gets canceled immediately.

d. Good-on-Close Order. It is also called the market-on-close order. It is executed at the price prevailing at the close of trading on the day it was placed. The main motive behind placing a good on close order is that the trader might not want to close the books on a particular day at a loss. There may also be situations, where the market is pushed on high at the closing; in such situations, a good-on-close order is a more ideal option.

e. Stop orders. It allows the trading members to place an order which gets activated only when the market price of the relevant security reaches or crosses a certain threshold price. Until then the order does not enter the market.

A sell order in the stop loss gets triggered only when the last traded price in the normal market reaches or falls below the trigger price of the order.

A buy order in the stop-loss book gets triggered only when the last traded price in the normal market reaches or exceeds the trigger price of the order.

1.1.4. Clearing Instructions

The clearing instructions specify how the final settlement is arranged. When there is a single broker, there is not much need for the clearing instructions. However, when there is more than one broker, for executing both buy and clearing orders; then there is a need for the clearing instructions. The clearing instructions should indicate whether a sale is a long sale or a short sale.