a. The companies can issue their shares in not just their country, but in the international markets as well, due to globalization and free trade. This helps the countries widen their base of shareholders and get the best cost (obviously lower cost) for the capital issued.

b. Though the investors have a bias towards domestic investments due to the tax laws promoting the local investments, still they can gain access to the foreign investments, which may result in diversification of risk, away from the ‘domestic only’ investments.

c. There are certain restrictions imposed by different countries that restrict the flow of capital away from the local territorial boundaries. Such restrictions:

i. Limit the amount of control foreign investors have over domestic companies,

ii. Give domestic investors an opportunity to own the shares of foreign companies conducting business in the domestic markets, and

iii. Reduce the volatility of capital inflows and outflows.

These restrictions promote the investment in and growth of the local companies and thus the economy.

d. However, these restrictions do affect the performance of the equity market, which can be improved if these restrictions are reduced.

e. Off lately, a large number of companies have listed their shares in the markets outside their home countries. This is called ‘dual-listing. The main benefits of foreign listing are:

i. This improves the awareness about the company’s products and services, not only in the foreign countries but also improves their reputation locally.

ii. Foreign listing improves the liquidity of the shares.

iii. Since the companies issuing the shares internationally, have to fulfill the filing requirements of different countries, their transparency also gets increased.

1.1. Methods of Issuing Non-Domestic Equity

Following methods can be used to issue equity in a non-domestic region:

1.1.1. Direct Investing

a. As per this method, the securities are bought and sold directly in foreign markets.

b. The purchases, sales, gains/losses on the sale, payment of dividends, etc. are all done in foreign countries by the issuing companies. This kind of issue is, thus, subject to the exchange rate risk.

c. To make such an issue, the issuing company must be familiar with the trading, clearing, and settlement regulation of the foreign market.

Such issues may lead to either less transparency and more volatility, or more transparency and less volatility.

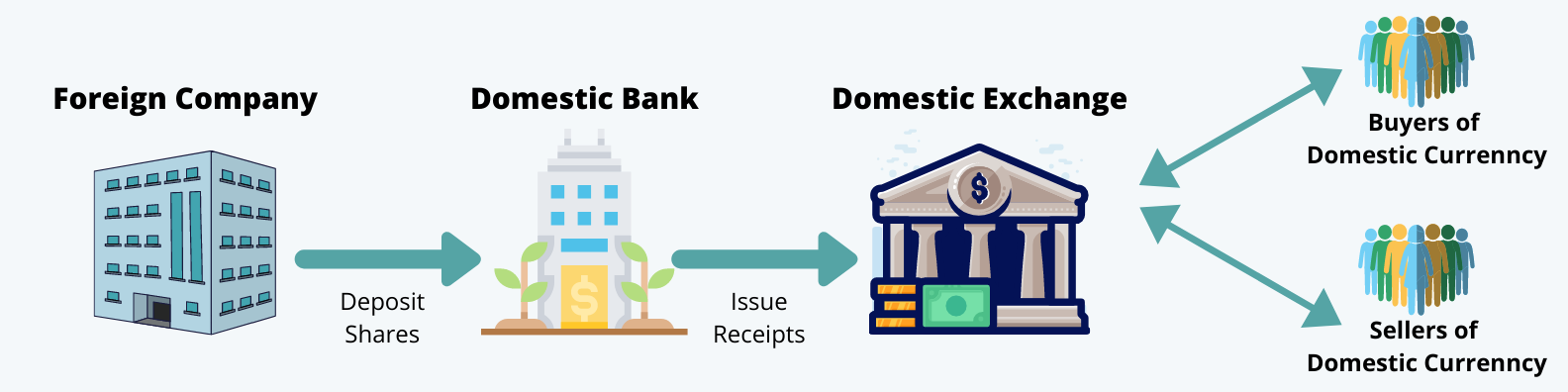

1.1.2. Depository Receipts

a. Depository receipt is the financial security issued by a local bank (acting as a custodian or transfer agent) that represents the foreign company’s traded securities.

b. These instruments trade like an ordinary share on a local exchange but represent an economic interest in a foreign company.

The following diagram explains the mechanism of a depository receipt:

c. The depository receipts do not eliminate the foreign currency risk but eliminate the foreign currencies from the transaction for the local investors.

d. The depository receipts may be of two types, i.e. sponsored or unsponsored.

e. The sponsored depository receipts allow the foreign companies a direct involvement in the issuance of receipts; whereas the investors in the depository receipts have the same rights as the direct owners.

f. The level 1 American Depository Receipts (ADRs) trade on the over-the-counter markets, whereas level 2 & 3 ADRs trade on the stock exchanges. Thus level 2 & 3 ADRs must be registered with SEC, and follow the regulatory guidelines. According to rule 144A, only qualified institutional buyers are allowed to trade in privately placed instruments.

g. In the unsponsored depository receipts, the foreign issuing company does not have any direct involvement in the issuance of receipts. The right of ownership also lies with the depository and not the investor.

h. The two most common types of depository receipts are American Depository Receipts (ADRs) and Global Depository Receipts.

i. The American Depository Receipts (ADRs) are certificates that are issued by a bank of American origin and traded in the US as domestic shares.

j. The Global Depository Receipts (GDRs) are issued by a depository in both banks outside the issuer’s home country and the US.

1.1.3. Global Registered Shares

These are ordinary shares that are quoted and traded in different currencies on different markets.

1.1.4. Basket of Listed Depository Receipts

It is nothing but the exchange-traded funds listed on the non-domestic territories.