1. Multi-Stage Dividend Discount Models

1.1. Two-Stage DDM

a. This model makes use of two growth rates; a higher initial growth rate for a finite period and then low growth perpetuity.

b. For the latter, i.e. the low growth rate perpetuity, the intrinsic value can be estimated using Gordon’s Growth Model called the terminal value.

c. For the first part, we can explicitly discount the value of all the dividends during the period along with the terminal value, calculated in the previous step to find the intrinsic value of the stock.

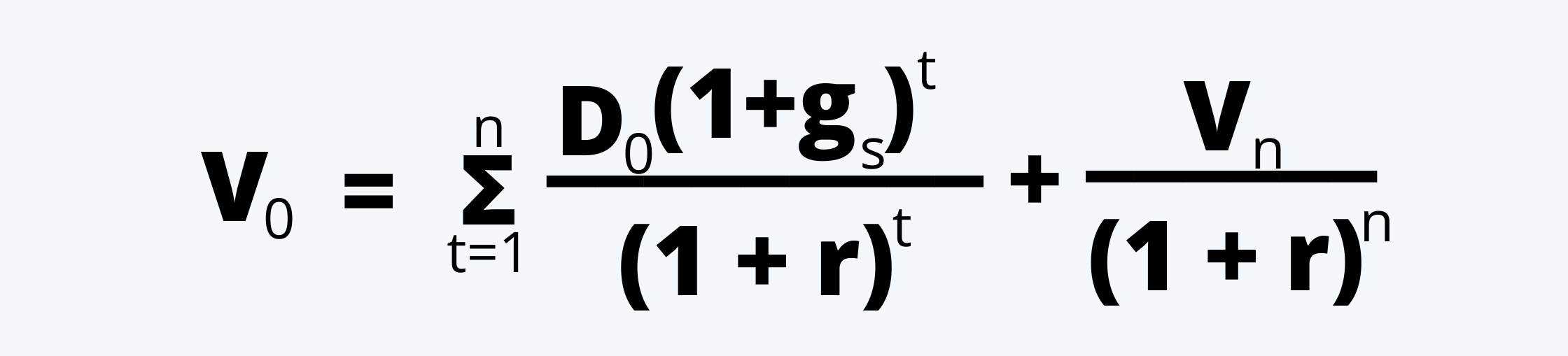

d. Thus the intrinsic value as per a two-stage DDM would be:

|

Where, Vn = gs = initial slower growth rate. gL = longer-term growth rate r = required rate of return |

For Example:

Suppose there is a stock, which is currently paying a dividend at $ 1 per year per share. This dividend is expected to grow at 8% per annum initially for the next 3 years and then at the rate of 4% per annum, infinitely. The required rate of return of the stock is 10%. We have to calculate the intrinsic value of the stock.

We are given the following information:

|

Particulars |

Value |

|

D0 |

$ 1 |

|

gs |

8% |

|

gl |

4% |

|

R |

10% |

The intrinsic value of the stock would be:

We, therefore, calculate the terminal value at the end of the third year (i.e. Vn) first.

V3 = (Dn+1) / (r – gL)

= [1 × (1 + 0.08)3 × (1 + 0.04)1] / [0.10 – 0.04]

= $32.75

Now we can calculate the intrinsic value of the stock today as follows:

V0 = [1 × (1 + 0.08)1 / (1 + 0.10)1] + [1 × (1 + 0.08)2 / (1 + 0.10)2] + [1 × (1 + 0.08)3 / (1 + 0.10)3] + [32.75 / (1 + 0.10)3]

= $ 27.50

1.2. Multiple Stage Model

The two-stage model can be extended in a similar fashion to accommodate for the change in growth rates multiple times, till it becomes stable in the long run.

2. Identifying Appropriate Model for The Companies

The model that is most appropriate for a company depends on the level of growth, maturity, and nature of the company. The valuation models and the list of companies for which they are most suitable are:

a. The Constant Growth Model. This model is most suitable for:

i. the companies with stable growth,

ii. the companies at the maturity phase,

iii. non-cyclical companies, and

iv. the dividend-paying companies.

b. The Two-Stage DDM. This model is most suited for the companies at the maturity stage that are expecting a transition. It is mainly for the older companies out of a growth stage or a revitalized company.

c. The Three-Stage DDM. This model is best suited for fairly young companies that are about to enter the growth stage. These companies can expect three stages, i.e. growth, transition, and maturity.