The weightings determine how much of each security to include in an index. Some of the different ways in which the weightings can be assigned to each security are:

1.1. Price Weightings

a. This is the simplest way of weighting the constituent securities in an index. The price-weighted average is the arithmetic average of current prices.

b. The Dow Jones Industrial Average (DJIA) is the most popular price-weighted average. DJIA is unique in price-weighted series rather than market capitalization-weighted series.

c. The component weightings are affected only by the changes in the stock prices, in contrast with the other indexes which give weightings that are affected by both price changes and changes in the number of shares outstanding.

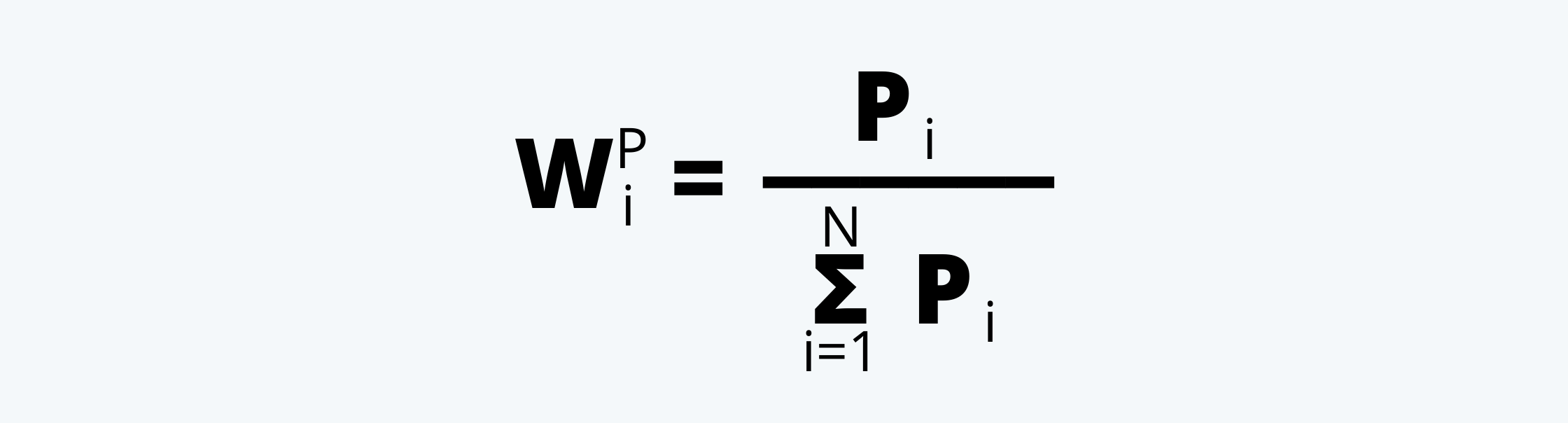

d. The weighting of a stock in the portfolio is calculated as follows:

Where,

Pi = Price of the security i

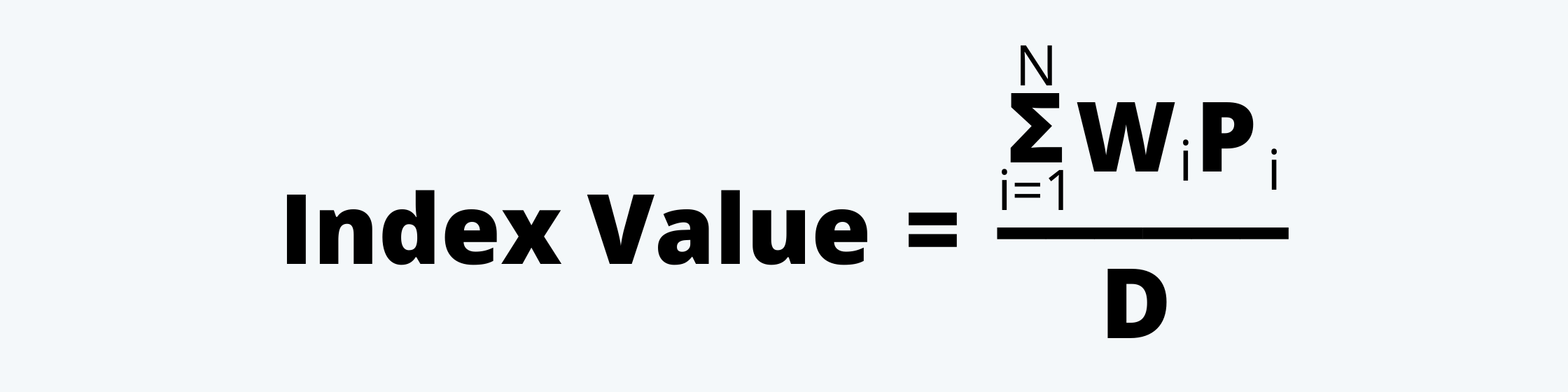

e. And, the value of the index is calculated as follows:

Where,

Wi = Weight of the security i

Pi = Price of the security i

D = Value of the Divisor typically set at the time of inception

f. When the weightings are assigned according to the price of the individual security, the stocks with the highest price will have the greatest impact on the return of the index.

g. When we use the price-weighted index, and there is any stock split in any of the constituent security, there is a fall in the price of that security, therefore all the weightings change, resultantly. Therefore, in such an event, the divisor needs to be adjusted to prevent the split from changing the value of the index.

1.2. Equal Weightings

a. This is also another very simple way of assigning the weights to the individual constituent securities in an index.

b. According to this method, equal weights are assigned to each of the constituent securities in the index.

c. Thus, the amount of weight assigned to each security equals one divided by the number of securities. That is,

d. The biggest disadvantage of using equal weightings is that the securities that represent the largest fraction of the target market are under-represented by this index. And, those that constitute a smaller fraction are over-represented.

e. This type of index requires frequent rebalancing because, after the construction of such an index, any price change would mean that the weightings are no longer equal.

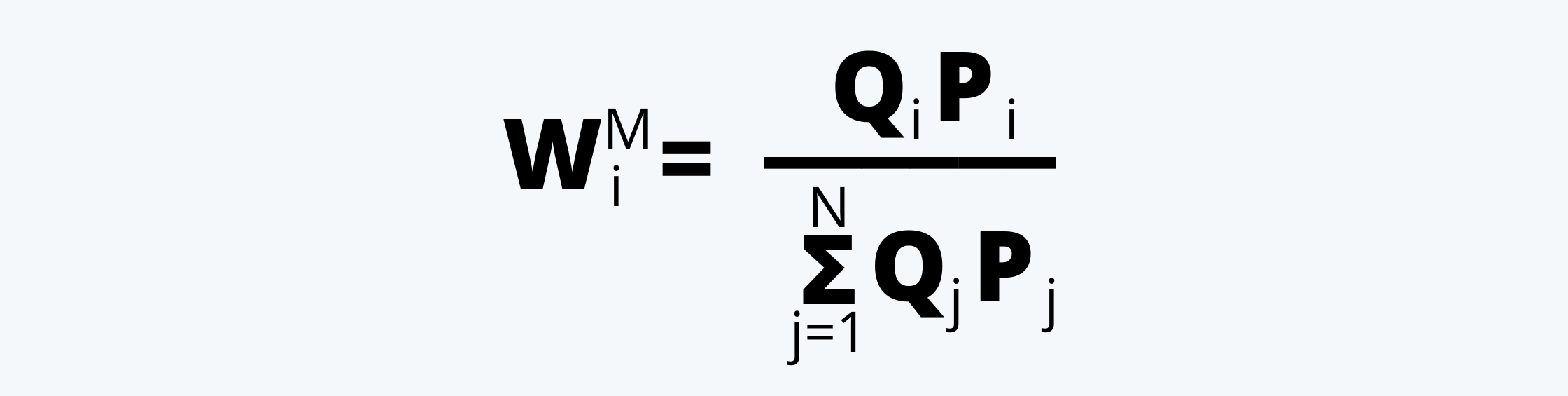

1.3. Market-Capitalization Weightings

This is one of the most popular ways of assigning weightings to the securities in an index. According to this method, the weights are assigned to the individual securities by dividing the market capitalization of that security by the sum of all market capitalizations. That is,

1.3.1. Float Adjusted Market Capitalization Weightings

a. We can move from the market-cap to the float-adjusted market-cap weightings. It should be noted that most of the market-cap-weighted indices are float-adjusted.

b. Float is the number of shares available to the investing public. Thus, free-float market capitalization is the proportion of total shares issued by the company that is readily available for trading in the market.

c. It generally excludes the promoters’ holding, government holding, strategic holding, and other locked-in shares that will not come to market for trading in the normal course.

d. The biggest advantage of converting to float-adjusted market-cap weightings is that the components are held in proportion to their value in the target market.

e. However, there is a disadvantage of having the float-adjusted market-cap, i.e. the capitalization is still based on the price times the quantity. And components whose prices have risen/fallen the most have a greater/lower weight in the index. This leads to overweighting of stocks that may be overvalued and underweighting of stocks that are undervalued.

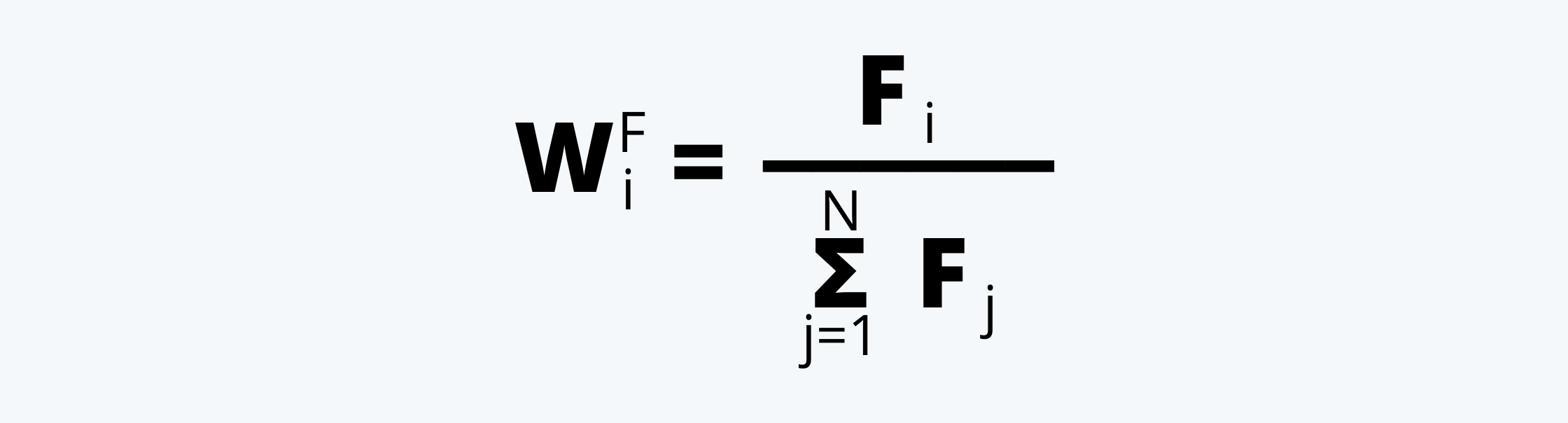

1.4. Fundamental Weightings

a. This method attempts to the disadvantages of the market-cap method in assigning the weights to the component securities.

b. This method uses a fundamental value as a proxy for size rather than the market cap. This fundamental value can be the book value, revenues, cash flow from operations, earnings, etc. Thus, the weights for each component are:

c. This method results in the indices with the ratio of fundamental value to market value, which could be higher than its market cap counterpart. These weights also favor the securities that have decreased in value.