1.1. Returns

a. Return is the total profit earned from an investment.

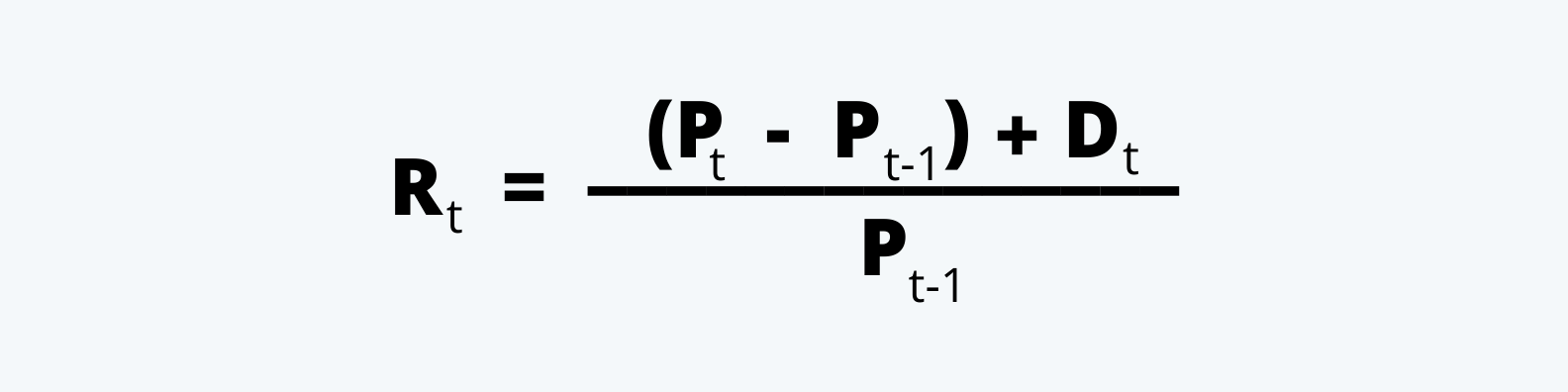

b. The two main sources of a single period return from an equity investment are capital gains and dividends.

|

Where, Rt = Total return in the period Pt = Price at the current point in time Pt-1 = Price at the beginning of the period Dt = Dividend during the current period |

c. For the depository receipts and direct foreign investments, the total returns also include the currency gains or losses.

d. Over the multiple periods, the dividends earned are also reinvested at times, thus there is a compounding effect that comes to play. This reinvestment need not be in the same security as before; it could be made in another company as well.

e. Thus there are four potential sources of return on equity investment: capital gains, dividends, currency gains, and dividend reinvestment.

1.2. Risks

a. Risk is thus the uncertainty of returns mentioned above, and cash flows.

b. Risk is said to be the chance of an outcome not occurring as planned. This may be due to the actual returns differing from the previously predicted return. In addition, the risk may also arise from the interest rates or foreign exchange rate changes, counterparty failure, issuer default, and many other causes.

c. There are two kinds of equities, i.e. preferred and common. The preferred equity is considered less risky than the common. This is mainly because:

i. The preference dividends are generally known and fixed, and dividends account for a large portion of total return from preferred stock, as it generally trades around its par value across its life. Thus, there is less uncertainty regarding the future cash flow on the preferred stock.

ii. The preferred stocks receive all dividends and distributions before the common stocks, making them less risky.

d. Also, the cumulative preferred shares are less risky in comparison to the non-cumulative

e. For the common shares, a large part of the total return is made up of capital gains, i.e. the change in the market price of the shares. Thus, the following needs to be noted about the risk factors associated with the different classes of common shares:

i. Putable shares are less risky than callable or non-callable shares.

ii. Callable shares are riskier than non-callable ones.

iii. Since public equity is more liquid than private equity, it is considered less risky.