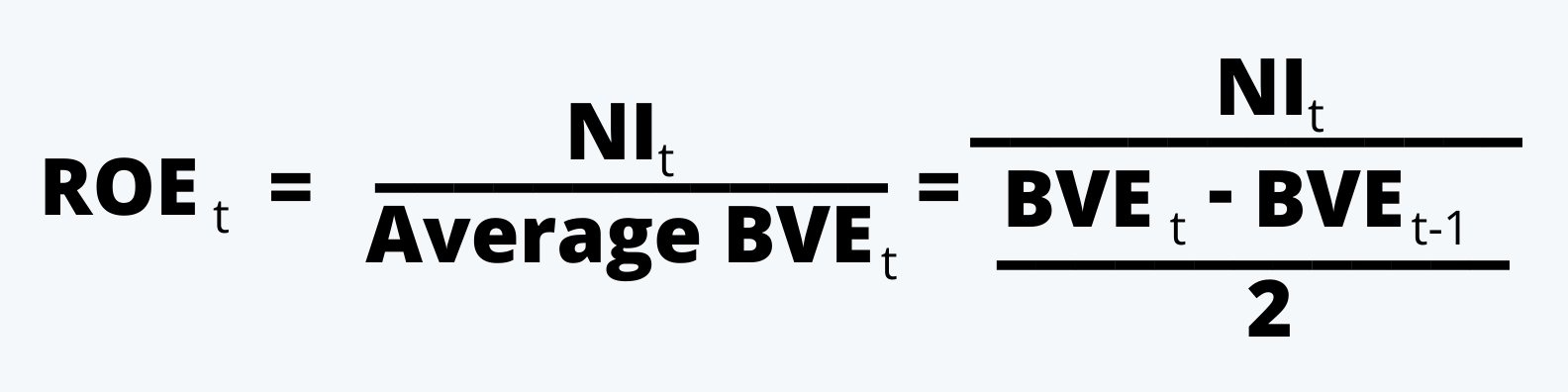

1.1. Accounting Return on Equity

a. It is the net income of an organization expressed as a percentage of its equity capital.

b. It uses the accounting net income, which is subject to the estimates and methods used by the management for the calculations.

c. It can be written as follows in the form of an equation:

d. One thing that needs to be noted here is that the NI or the net income is the total net income available to the common shareholders. It is the net income minus the dividends paid to the preference shareholders.

e. The ROE can be managed, especially through the issue of debt to buy back shares.

f. The accounting return on equity can be increased if:

i. Net income rises faster than the book value of equity, or

ii. Net income falls slower than the book value of equity, though this situation is not quite desirable.

1.2. Intrinsic Value

Intrinsic value is the present value of the expected future cash flows, discounted at the required rate of return called the ‘cost of equity’.

The cost of equity is the discount rate needed to equate the expected future cash flow with the offering price.

1.3. Price-to-Book Ratio

a. It is the ratio of the market value of equity per share to the book value of equity per share.

b. A higher price-to-book ratio indicates that the market is pricing in the higher future growth opportunities. It means that the company is perceived as a less risky investment option by the investors.