LOS C requires us to:

calculate the tax base of a company’s assets and liabilities.

The tax base is the amount at which the assets and liabilities are valued for the tax base. For the purpose of financial reporting, we prepare an income statement. Whereas, for the income tax purpose, we report the revenues, expenses, and profits through the income tax return. There may be differences in the amount of income and expenses reported in the two statements (as discussed above). And due to the differences in the income and the expenses reported in the two statements, there may arise, differences in the carrying values of assets and liabilities (under the two). The carrying value of the assets and liabilities in the balance sheet, as if the income and expenses as per the income tax return was our real income statement.

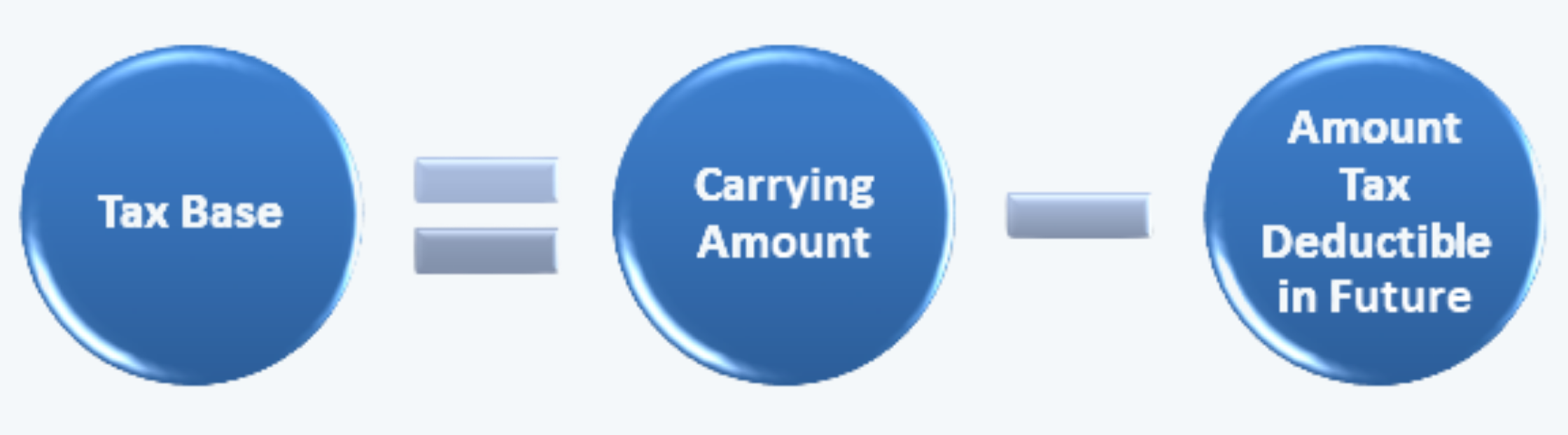

1. Assets Tax Base

It is the amount that would be deducted or expensed on the future tax returns when the economic benefits of it are realized.

For Example:Suppose there were some research and development costs of $ 1,000,000 incurred during the year. For the financial reporting purpose, the entire amount was expensed in the year of incurring. Thus in the statements prepared for financial reporting purposes, the entire amount would be reduced from the current year’s revenue, and there would be no assets to be reported in the balance sheet. However, suppose for the taxation purpose, the entire amount of expense on research and development is capitalized and expensed/amortized over a period of next five year, then the tax base of the asset would be:

The tax base, as reflected above, is the amount that would have been reported in the balance sheet if it was prepared considering the income tax return as the real income statement. This would create a deferred tax asset, as the earnings before tax (as per the financial reporting) are less than the taxable income (as per the income tax return). This is the amount that would be expensed in the future years in the tax returns. |

Note:

One thing that needs to be noted here is that students do get confused about the taxability issue and its effect on the tax base. The taxability of any amount of asset does not affect its tax base. The tax base simply reflects the carrying value of the assets or liabilities, if the tax return were to be considered as the actual income statement.

For example, a company has a receivable of $ 100,000 in the next year and these revenues are exempt from tax. These would be reported as assets in the actual balance sheet under accounts receivable and the carrying value would be $ 100,000. And, since the same is not recognized as revenue in the current year as well, it would be reported at $ 100,000 in the tax base as well. The future taxability does not affect the carrying value of the asset for the tax purpose.

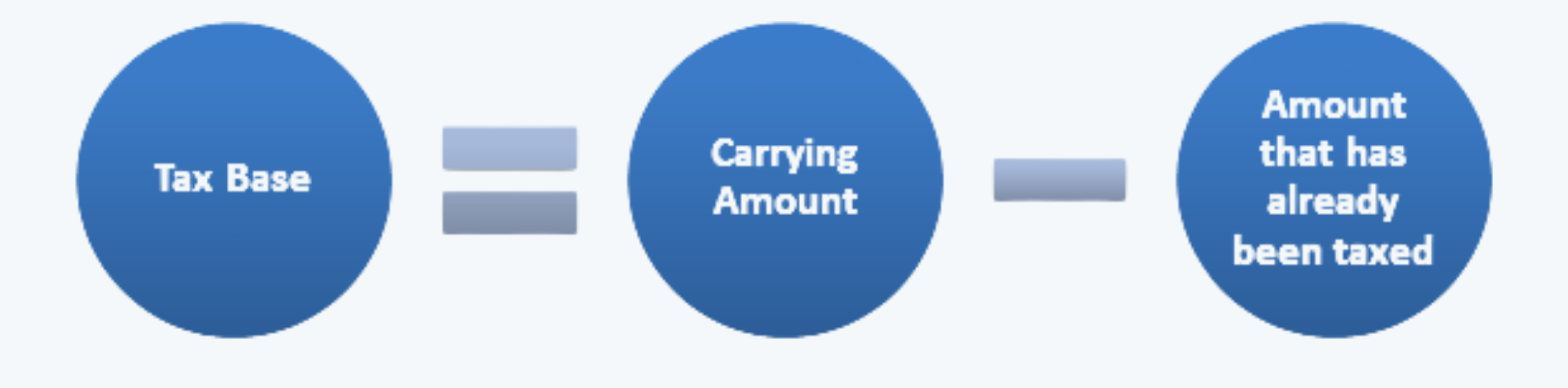

2. Liability Tax base

A liability tax base is the carrying value of the liability, as reduced by any amount that would be deductible on the tax return in the future. The tax base of revenue received in advance or the unearned revenue is the carrying value minus the amount of revenue that will not be taxed.

Thus, for a liability like accrued expense:

This can be explained with the help of the following example:

Example:Suppose a company has a policy of expensing 2% of the sales as warranty expense each year. And the company this year’s warranty expenses turn out to be $ 10,000 for financial reporting purposes. However, there were no warranty charges this year. Also, as per the applicable tax laws, the warranty expenses can only be deducted in the period when they actually become payable. Thus, the carrying value of the expense would be $ 10,000, i.e. the amount actually expensed during the period. However, the tax base is the carrying amount minus the amount tax-deductible in the future. Thus, in this case, the tax base is: $ 10,000 – $ 10,000 = 0 The temporary difference (i.e. carrying value – tax base), would thus be: $ 10,000 – 0 = $ 10,000 Similarly, consider there were accrued salaries of $ 100,000 at the end of the year. For the financial reporting purpose, these are supposed to be expensed in the year they get accrued. Thus, the carrying value of the expense in the current year would be $ 100,000. Now, let us suppose that the income tax laws also permit that the salary expenses should be allowed in the period to which they belong. Therefore, the tax base, i.e. the carrying amount minus the amount tax-deductible in the future, would be: $ 100,000 – 0 = $ 100,000 Thus, the temporary difference (i.e. carrying value – tax base) here would be: $ 100,000 – $ 100,000 = 0 |

And, for the revenue received the tax base is:

This can be explained with the help of the following example:

Example:Suppose there were unearned revenues worth $ 10,000 during the reporting period. For financial reporting purposes, these must be reported as a current liability. Thus there would not be any expense during the period. Hence, the carrying value as per the balance sheet would be $ 10,000. Now, as per the tax laws, suppose the revenues ought to be taxed in the period in which they are received. Thus, the entire $ 10,000 would be reported as the income of the current year and be taxed as well. Thus, the tax base (i.e. carrying amount – amount already taxed) would be $ 0 (i.e. $ 10,000 – 10,000). And the temporary difference would be $ 10,000 (i.e. $ 10,000 – 0). |

To summarize, we can say that:

a. A higher tax expense or lower tax revenue results in lower taxable income. Therefore, the tax payable is less than the income tax expenses. This, in turn, results in the creation of deferred tax liability.

And, any increase or decrease in the deferred tax liability also increases or decreases the total liabilities side of the balance sheet.

b. A lower tax expense or higher tax revenue results in higher taxable income. Therefore, the tax payable is higher than the income tax expenses. This, in turn, results in the creation of deferred tax assets.

And, any increase or decrease in deferred tax assets also increases or decreases the total asset side of the balance sheet as well.