LOS C requires us to:

describe the International Accounting Standards Board’s conceptual framework, including qualitative characteristics of financial reports, constraints on financial reports, and required reporting elements.

‘Conceptual Framework for Financial Reporting’, which was adopted in the year 2010 forms the base upon which the IASB sets its standards. The financial reporting framework prescribes the qualitative characteristics and required reporting elements based upon which the IFRS are prepared. The framework also acknowledges the constraints and the assumptions that go into preparing the standards. The framework is basically aimed at providing the standards that are useful for all the users of financial statements such as shareholders, lenders, creditors, etc.

1. Qualitative Characteristics of Financial Reports

There are two fundamental qualitative characteristics, as identified by the conceptual frameworks, which make the financial information as reported in the reports useful to its users. They are:

a. Relevance. The information is considered relevant if it affects the user’s decision-making and it has some value. The information could either have predictive value (useful in making forecasts), confirmatory value (useful to evaluate past decisions or forecasts), or both. Also, the information’s value should be at least enough to have an influence on the decision of the users, and its omission could badly influence the users of such information (i.e. it should be material enough).

b. Faithful Representation. Information is considered as faithfully represented if it is:

i. complete, in the sense that it covers all the economic data and other data necessary for the users to form an opinion;

ii. unbiased, in the sense that it should not be influenced by the personal benefits of any of its beneficiaries; and

iii. free from error, either intentional or unintentionally due to omission or commission, etc.

Besides these two fundamental qualitative characteristics, the Conceptual Framework (2010) identifies four characteristics that enhance the usefulness of relevant and faithfully represented financial information. They are:

i. Comparability. The information that is provided by the financial reports should be compared not only across different entities but also within the same entity, across different periods. Comparisons make the analysis of the information easier.

ii. Verifiability means that different knowledgeable and independent observers would agree that the information presented faithfully represents the economic phenomena it purports to represent.

iii. Timeliness. Timely information is available to decision-makers prior to their making a decision.

iv. Understandability. Obviously, all the financial information is not understandable by every other layman. But, it should be understandable for a person having reasonable knowledge about business, economic activities, and financial reports. Also, the useful information should not only be excluded on the grounds that it is not understandable.

2. Constraints on Financial Reports

It is extremely desirable that the information be absolutely complete with all the desirable qualitative characteristics. However, there are certain constraints to the same. They are:

a. The cost of the information. There is always a cost-benefit trade-off between the potential benefits that can be attained from information and the cost of making it available to its users in a complete form. Those responsible for providing the information should make sure that the cost of information shouldn’t exceed its potential benefits.

b. Valuing the Intangible. The information regarding the value of the tangible assets and liabilities can easily be identified. But, the non-quantifiable information about the intangibles is difficult to provide and is a big constraint towards providing qualitative information.

3. Underlying Assumptions of the Financial Statements

There are two major assumptions of financial statements. They are:

a. Accrual Accounting. This means that the accounting system does not record the transactions on a cash basis; rather they are recorded at the time of their occurrence.

b. Going Concern. It is assumed that the business of the entity is not going to cease at any time in the foreseeable future. Thus any events (such as the sale of major assets etc.) that indicate otherwise, should be reported separately as notes to accounts or otherwise, to give true and clear information about the entity.

4. Recognition of Financial Statement’s Elements

Any element of the financial statements, whether it is an asset, liability, revenue, or expense, etc., should only be recognized if the following criteria are met by them:

a. it is probable that any future economic benefit associated with the item will flow to or from the enterprise, and

b. the item has a cost or value that can be measured with reliability.

5. Measurement of Financial Statements Elements

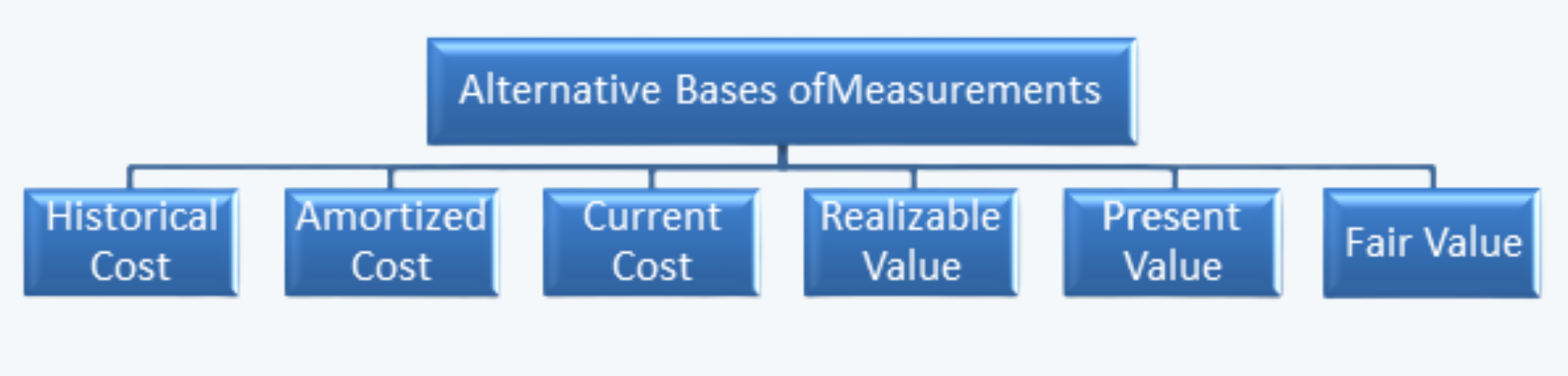

The values of the elements of the financial statements can be measured and recognized in the books of accounts using the following alternative basis of measurements:

a. Historical Cost. The historical cost is either of the following:

i. The amount of cash or cash equivalent paid to purchase and put the asset to use. This also includes the other cost of acquisition.

ii. If the asset was not purchased in cash, then the fair value of the asset given in barter to purchase the same.

b. Amortized Cost. It is the historical cost of the asset, after adjusting for depreciation, amortization, or impairment.

c. Current Cost. It is the cost to purchase the same or similar asset in the current market. For the liabilities, it is the amount required today to sell the asset.

d. Realizable Value. This represents the amount that will be received /paid today to sell off the asset or settle the liability on the reporting date.

e. Present Value. It is the discounted value of all the future benefits expected from an asset or the future obligations required to be paid or met in respect of any liability. The assets and liabilities are usually discounted at the cost of equity or the weighted average cost of capital.

f. Fair Value. It is the value that would be fetched if the asset is sold or liability is settled between the two knowledgeable and willing parties at arm’s length price.

6. Required Financial Statements

As per IAS No. 1, the following reports should be prepared to complete the set of financial statements:

a. Statement of financial position or balance sheet;

b. Statement of comprehensive income or income statement;

c. Statement of changes in equity;

d. Statement of cash flows; and

e. Notes to accounts (summarizing the significant accounting policies and giving disclosures as required as per IFRS and other applicable statutes).

7. General Features of Financial Statements

The financial statements prepared under IFRS should be compliant with all its requirements. If however, it has to deviate from the same, necessary disclosures are required to be made.

As per the conceptual framework as reflected in the IAS No. 1, financial statements should have the following general features:

a. Fair Presentation. The economic transactions and the elements of the financial statements should be reflected at their complete and fair value in the books of accounts.

b. Going Concern. It is assumed that the reporting entity would continue its business at all times in the foreseeable future. If there is any deviation from this assumption it should be reported as disclosure in the books.

c. Accrual Basis. All financial statements, except the cash flow statements, are prepared on an accrual basis.

d. Materiality and Aggregation. All the information is considered material if it can influence the decision of its users. And, all material information should be reported separately unless they are not material.

e. No Offsetting. All the assets and liabilities and income and expenses are not offset unless required or permitted by an IFRS.

f. The Frequency of Reporting. Financial Statements should be prepared at least on an annual basis.

g. Comparative Information. The comparative information of the previous period should also be reported along with the current year’s figures.

h. Consistency. The presentation and classification of items in the financial statements are usually retained from one period to the next.