LOS E requires us to:

describe how the choice of depreciation method and assumptions concerning useful life and residual value affect depreciation expense, financial statements, and ratios.

While accounting for long-lived assets management must make a lot of choices for the method of depreciation to be chosen, the estimates for useful lives, the residual salvage values, etc. need to be made. This increases the scope of manipulation of financial statements by the management. Some of the choices and their impact on the financial statements are discussed below:

1. The assumption for Useful Life

a. The estimated useful life of an asset has a direct impact on the amount of depreciation to be charged to the profits in each year.

b. A longer estimated life results in lower depreciation, thus a higher net income reported each year. It also results in the higher carrying value of the asset to be reported on the balance sheet.

c. On the other hand, a shorter estimated useful life results in lower net income and low carrying value of assets.

2. Estimates of Residual Value

a. The estimated residual value also impacts the amount that needs to be depreciated over the estimated useful life.

b. A higher estimated residual value would mean a lower value to be depreciated during the useful life, and a higher carrying value of the asset for the balance sheet.

c. On the other hand, a lower residual value would mean higher depreciation and lower carrying value.

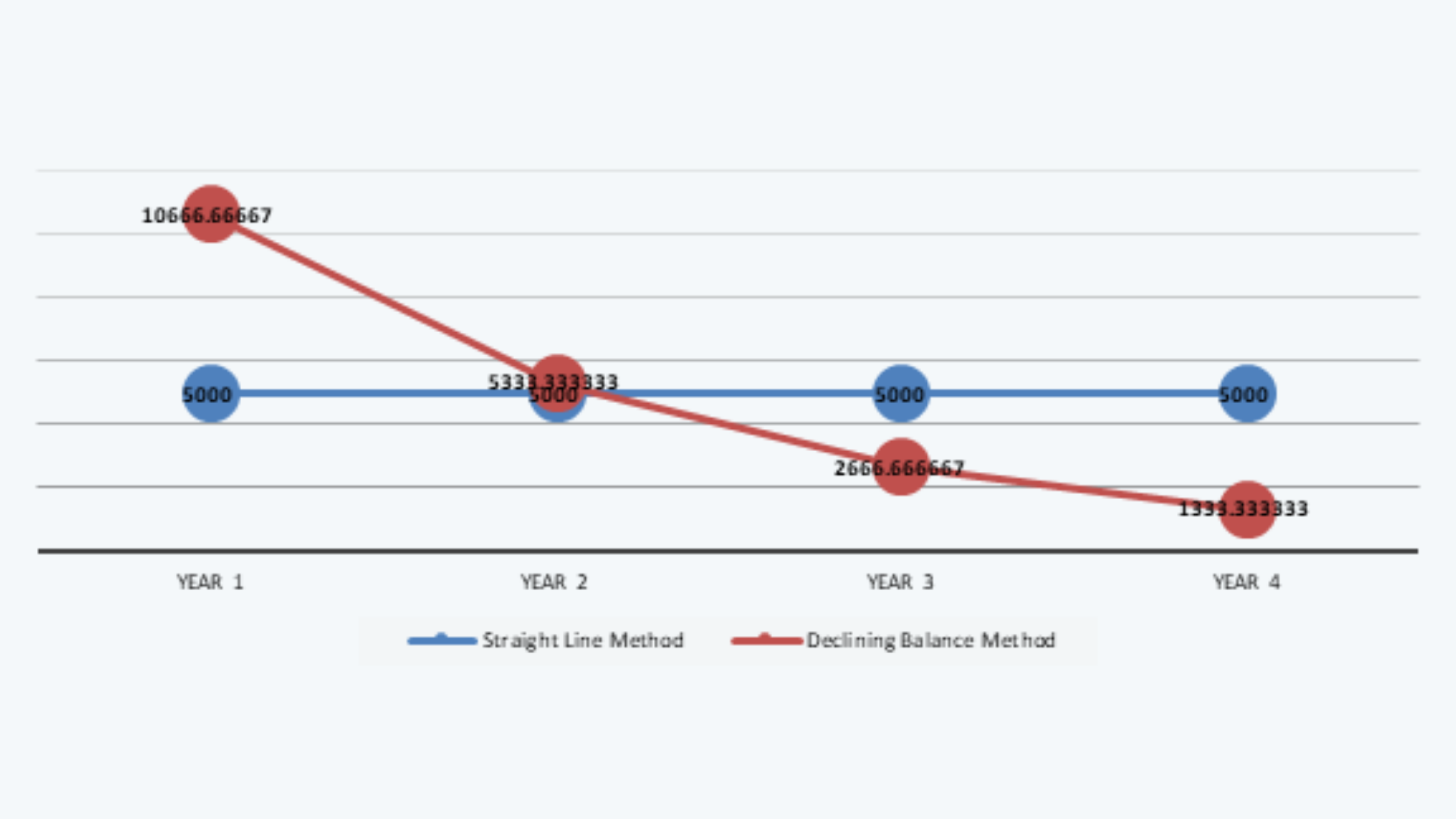

3. Impact of Choice of Method

a. On Amount of Depreciation.

The straight-line method of depreciation results in lower depreciation in the initial years of the depreciable life than the declining balance method. In the later years, the depreciation is higher under the straight-line method. Graphically, it can be represented as follows:

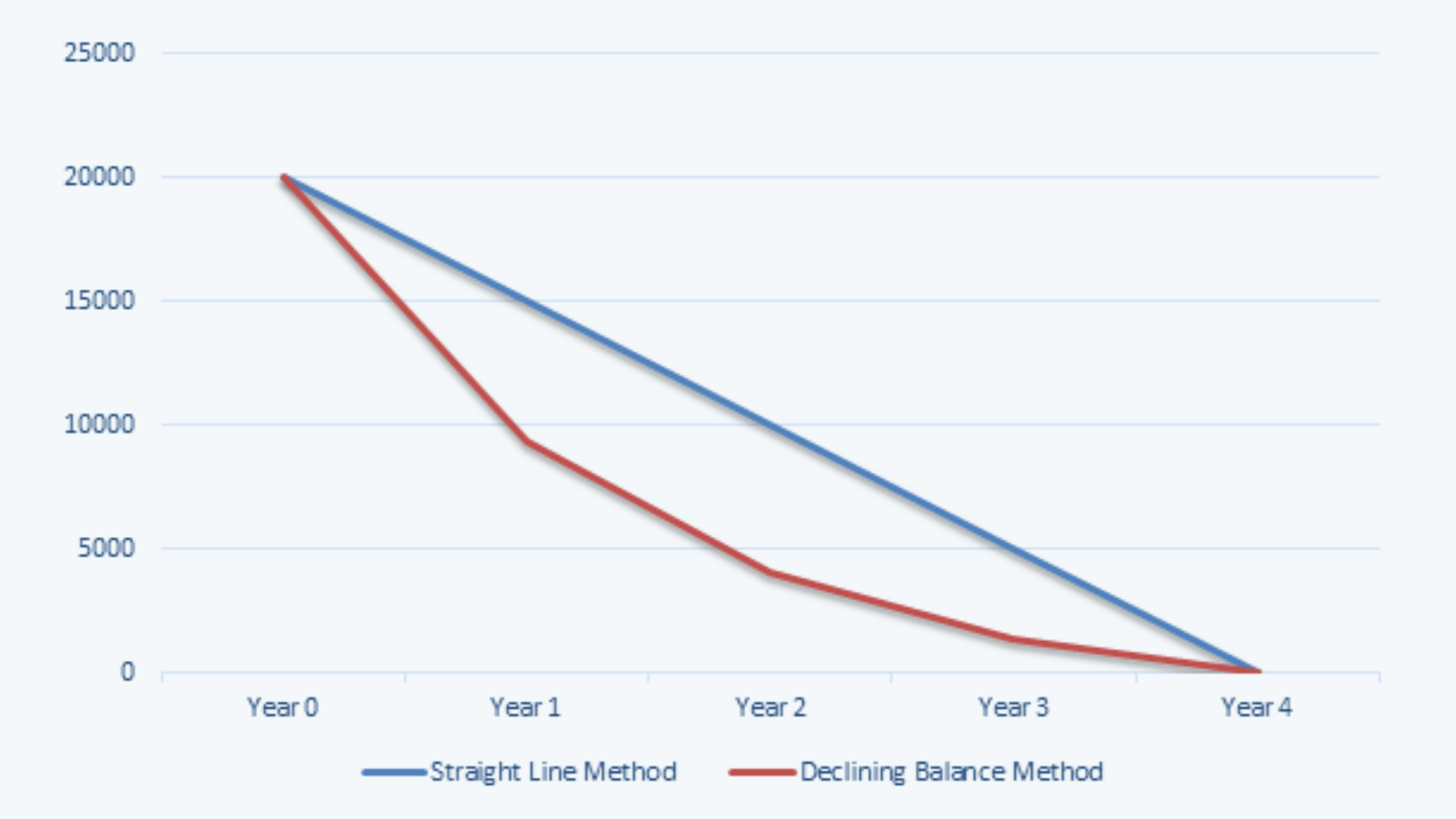

b. On the Book Value of Total Assets

The book value total assets would be the same at the beginning and the end of the useful life, and in the remaining part, it would be higher under the straight-line method. Graphically, it can be represented as follows:

c. Thus, any ratios that have average total assets in the numerator will be higher under the straight-line method and vice-a-versa for the ratios with average total assets in the denominator.

Component Depreciation

a. IFRS mandatorily requires, and U.S. GAAP gives the option to follow the component method of depreciation.

b. As per this method, different components of assets should be depreciated separately.

c. For example, we might have an asset with a cost of $ 10,000 including a component worth $2,000. The estimated life of the asset if 10 years and that of the component is 2 years, with zero salvage value.

Now, under GAAP, the asset would be depreciated at $ 1,000 (i.e. $ 10,000/10) each for the first two years. In the third year, there would be an additional cost of $ 2,000 that would be depreciated for the next 8 years. So the depreciation cost in 3rd year onwards would be $ 1,250 (i.e. $1,000 + 2,000/8). And the amount of depreciation would keep increasing every time a new component is purchased.

However, under IFRS, the asset would be depreciated separately for 10 years at the rate of $ 800 ($ 8,000/10) each year. And the component would be depreciated at the rate of $ 1,000 (2,000/2) each year for two years of its life.

The total depreciation under both methods would be the same under both IFRS and GAAP.