The LOS B requires us to:

describe the roles of financial reporting standard-setting bodies and regulatory authorities in establishing and enforcing reporting standards.

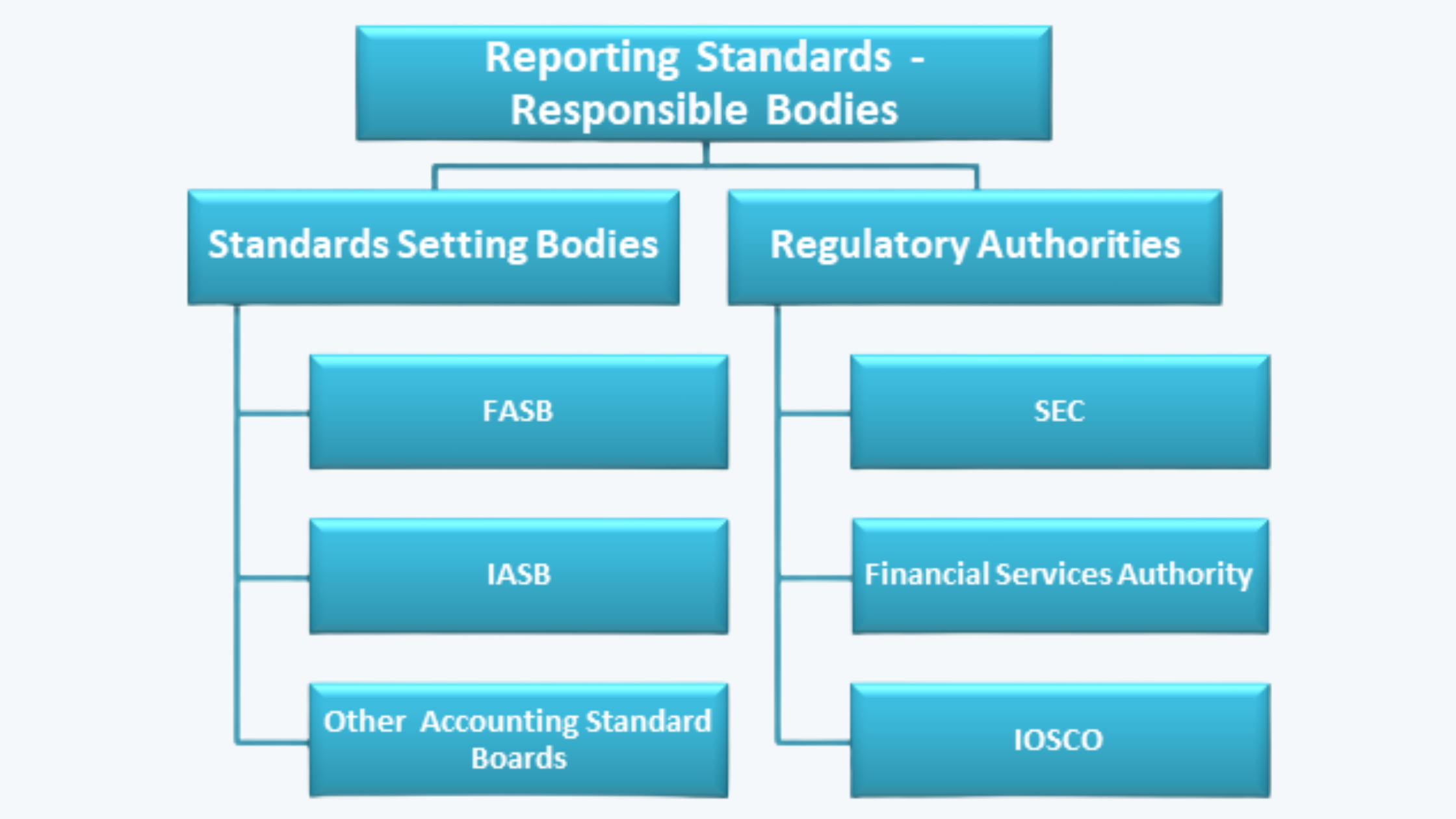

There are two types of bodies responsible for the formation and implementation of the financial reporting standards in any country. They are: the standard setting bodies and the regulatory authorities.

1. Standard-Setting Bodies

The standard-setting bodies are usually:

a. the private, self-regulated, not-for-profit organizations;

b. consisting of people like accountants, auditors, industry veterans, users of financial statements, academicians, etc.

c. responsible for setting financial reporting standards.

The examples of standard-setting bodies are:

a. IASB or International Accounting Standard Board (responsible for giving IFRS).

i. IASB is governed by its board of trustees. These trustees have diverse geographical and professional backgrounds.

ii. The trustees of the board are responsible for:

# appointment of the members of the organization;

# appointment of members related entities such as IFRS Interpretation Committee and IFRS Advisory Council;

# financing the foundation;

# establishing the budget; and

# establishing and monitoring the strategies of the board.

iii. IASB is committed to working in the public interest towards:

# developing and promoting the adoption of a unified set of high-quality financial reporting standards;

# ensuring that the standards result in transparent, comparable, and decision-useful information, keeping in mind the geographical and volume-based diversity of its potential implementers; and

# promoting convergence of national accounting standards of different countries with the internationally accepted IFRS.

iv. IASB follows a series of processes while developing and issuing the reporting standards (Usually other standard-setting bodies spread across the earth, also follow a similar procedure). This includes:

# Step 1: An issue is identified as a priority for consideration and placed on the IASB’s agenda in consultation with the Advisory Council.

# Step 2: The issue is then considered in its meetings, after which the IASB may publish an exposure draft for public comment. In addition to soliciting public comment, the IASB may hold public hearings to discuss proposed standards

# Step 3: After reviewing the input of others, the IASB may issue a new or revised financial reporting standard.

v. FASB or Financial Accounting Standards Board of USA (responsible for giving US GAAP).

# Like IASB, FASB is also governed by a board of trustees, who are responsible for the appointment of its members and the related entities.

# The steps in the process of setting and improving the standards are also similar to that of IASB.

# The standards so set by the board after following the procedure are contained in the FASB Accounting Standards CodificationTM (Codification).

1.1. Desirable attributes of Standard-Setting Bodies

In order for the standard-setting bodies to provide high-quality financial reporting standards, they must have the following attributes:

a. The bodies should observe a very high quality of ethical, professional, and confidentiality standards.

b. The responsibilities of all the parties involved in standard-setting should be clearly defined, providing adequate authority, resources, and competencies; in order to have proper functioning and accountability.

c. The process to be followed in a standard-setting should be clearly defined, guided by a well-articulated framework with a clearly stated objective.

d. The board may seek inputs from various stakeholders, but it should operate independently, going by the stated objectives.

e. Decisions should be made in public interests only.

2. Regulatory Authorities

The standards set by the regulatory authorities cannot be implemented and enforced properly unless there are bodies regulating the same. The regulatory authorities are the bodies (mainly government organizations), responsible for the enforcement of financial reporting requirements based on the standards set by the standard-setting bodies, on the entities participating in the capital markets and falling under their jurisdictions.

There are many regulatory authorities around the world to ensure that there is proper enforcement of accounting and financial reporting standards. The major of them are:

2.1. International Organization of Securities Commissions (IOSCO)

a. IOSCO was formed in the year 1983 as a successor to the inter- American regional association, as a cooperative body.

b. IOSCO has three categories of members:

i. Ordinary Members (currently 126) are the national securities commissions or similar governmental bodies with significant authority over securities or derivatives markets in their respective jurisdictions.

ii. Associate Members (currently 23) are usually supranational governmental regulators, sub-national governmental regulators, inter-governmental international organizations, and other international standard-setting bodies, as well as other governmental bodies with an appropriate interest in securities regulation.

iii. Affiliate Members (currently 65) are self-regulatory organizations, securities exchanges, financial market infrastructures, international bodies other than governmental organizations with an appropriate interest in securities regulation, investor protection funds, and compensation funds, and other bodies with an appropriate interest in securities regulation.

c. IOSCO’s core standards are set in the form of The Objectives and Principles of Security Regulations (2010). These standards give three major objectives for financial reporting regulations. They are:

i. protecting investors;

ii. ensuring that the markets are fair, transparent, and efficient; and

iii. reducing systematic risk.

There are also a set of nine principles for the regulators; the ones in relation to financial reporting are:

i. There should be full, accurate, and timely disclosure of financial results, risk, and other information which is material to investors’ decisions.

ii. Accounting standards used by issuers to prepare financial statements should be of a high and internationally acceptable quality.

d. Though mostly the regulatory authorities work within the jurisdiction of individual countries, with the desire to have a unified set of financial reporting standards like IFRS across the world; there is a need to have an international regulatory authority like IOSCO to oversee its enforcement. Thus, IOSCO assists in attaining this goal of uniform regulation as well as cross-border cooperation in combating violations of securities and derivatives laws.

2.2. The Security Exchange Commission (SEC)

SEC is also a member of IOSCO. Its primary responsibility is the regulation of securities and capital markets in the United States. It was basically formed after the great depression of 1929.

SEC has given many sets of laws and acts to regulate the auditors, dealers in the security markets, brokers, etc. The major of them being:

a. Securities Act, 1933. This act specifies the financial and other significant information that investors must receive when securities are sold, prohibits misrepresentations, and requires initial registration of all public issuances of securities.

b. Securities Exchange Act, 1934. This act created the SEC, gave the SEC authority over all aspects of the securities industry, and empowered the SEC to require periodic reporting by companies with publicly traded securities.

c. Sarbanes-Oxley Act, 2002. This act was created to oversee the functioning of the auditors, and for this purpose, it created the Public Company Accounting Oversight Board (PCAOB). The main focus of this board is to ensure the independence of the auditors so that they can function properly.

The companies comply with the regulations of the SEC through various fillings it makes in the form of reports, statements, and forms. Almost all the filings made with SEC are in electronic mode.

Some of the important filings required are:

a. Securities Offering Registration Statement. Whenever there is new security offered for sale to the public, the companies are required to file Form S-1 with SEC. In this form they are required to declare about:

i. the details about the security being offered for sale, especially the amount and use of proposed offerings proceeds;

ii. the information typically provided in the annual filings;

iii. underwriters identification;

iv. risk assessment;

v. relationship of the new securities with the existing capital instruments of the issuer; etc.

b. Forms 10-K, 20-F, and 40-F. These are the annual filing requirements for the US and non-US assessments. These forms require a comprehensive overview, including information concerning a company’s business, financial disclosures, legal proceedings, and information related to management. The financial disclosures include a historical summary of financial data (usually 10 years), management’s discussion and analysis (MD&A) of the company’s financial condition and results of operations, and audited financial statements

c. Annual Report. Though it is very much similar to the Form 10-K, the focus is slightly different. This report is mainly aimed to present the company’s information to its shareholders, unlike Form 10-K, which is more of a legal document. Some companies do not prepare a separate annual report; they modify the Form 10-K to inculcate the features of the annual report.

d. Proxy Statements. Proxy statements are filed with SEC in Form DEF-14A. These are the statements circulated to the shareholders prior to the general meetings, giving the shareholders the authority to give rights to others to cast vote. These statements typically give information about the proposals likely to be considered and voted for in the meetings.

e. Form 10-Q and 6-K. These are the interim reports required to be filed by the US and non-US companies respectively. The companies are required to file the updated non-audited financial statements, disclosing information about certain events such as significant legal proceedings or changes in accounting policies.

f. Form 8- The companies are required to file this form to make disclosures about the significant asset acquisition and disposals.

g. Form 144 can be filed by the issuers of the securities to qualified buyers without registering the securities with SEC.

h. Form 3, 4, and 5. These forms are required to report beneficial ownership of securities by the company’s directors and officers. These forms give information about the transfer of securities by the company insiders.

i. Form 11. This form is filed to make disclosures regarding the employee stock purchase, and other benefit plans.

2.3. Capital Market Regulation in Europe

In Europe, two committees regulate the securities market for the members of the European Union. These are: European Securities Committee (ESC) and the Committee of European Securities Regulators (CESR). ESC provides advisory services on the security policy issues, CESR however, assists in the technical issues.