Under IFRS, IAS12 covers accounting for a company’s income taxes and the reporting of deferred taxes. And, under U.S. GAAP, SFAS No. 109 is the primary source for information on accounting for income taxes.

There is sometimes a difference in the way transactions are accounted for and recognized for the financial accounting purpose, and the way they are treated for the income tax purpose. The financial statements prepared for accounting and reporting purposes are usually built, keeping in mind the accounting standards. These statements usually result in a line item called the income before taxes. Whereas, the reportable income prepared for the taxation purpose is built based on the applicable tax laws. And, these reports mainly report a line item called the taxable income. The tax calculated on the income tax expense as per the accounting income is called the ‘income tax expense’. Whereas, the tax calculated on the taxable income is the actual ‘tax payable’.

The difference between the taxable income and accounting income can be classified into permanent differences and timing differences. Permanent differences are those differences between taxable incomes which originate in one period and do not reverse subsequently. Whereas, the timing differences are those differences between the taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more subsequent periods.

If the income tax expense as per the accounting income is greater than the actual income tax payable, then there is a creation of the deferred tax liability. But, if the actual income tax payable is higher than the tax expense then there is a creation of deferred tax asset.

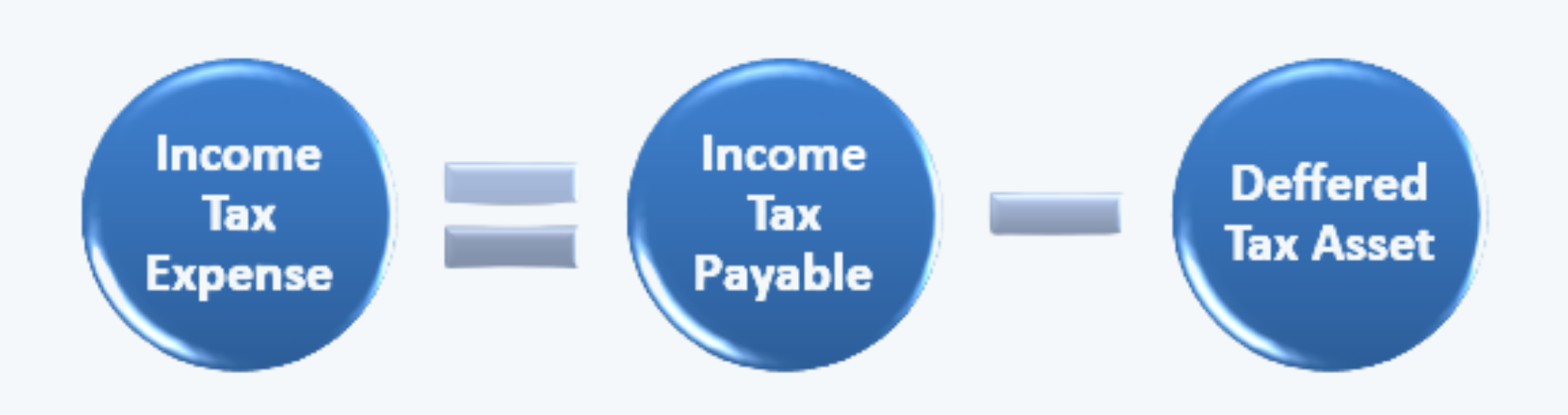

Therefore the income tax expense is always equal to the income tax payable as adjusted for the deferred tax asset/liability. That is,

Or,

The deferred tax asset is usually adjusted for a ‘valuation allowance’ under GAAP. This valuation allowance reflects the probability of non-use of this asset. For example, a company may be carrying a deferred tax asset to reflect the temporary differences created due to the carry forward losses, and these losses may only be carried forward for next year. Now, if we expect the company may also incur the losses in the next year, this would not allow them to make use of such deferred tax assets. Therefore, in anticipation of the inability to use these assets, the company may adjust these deferred tax assets reflected in the balance sheet through an allowance called the valuation allowance. The detail about the valuation allowance is usually found in the notes to accounts.

Further, there may also be changes in the tax laws that restrict the future use of the deductible temporary differences, creating a need for the valuation allowance.