In the previous chapters of this study session, we have understood various important sources of data for analysis, i.e. balance sheet, income statement, and cash flow statement. The data obtained from these sources need to be converted into meaningful information for the purpose of financial analysis. This can be done by using various financial analysis techniques such as ratio analysis, trend projections, etc.

The two most important categories of analysis discussed in this chapter are: equity analysis and credit analysis. The main purposes of equity analysis are the valuation of the firm or its equity, and performance evaluation. On the other hand, the credit analysis takes to account the creditor’s perspective.

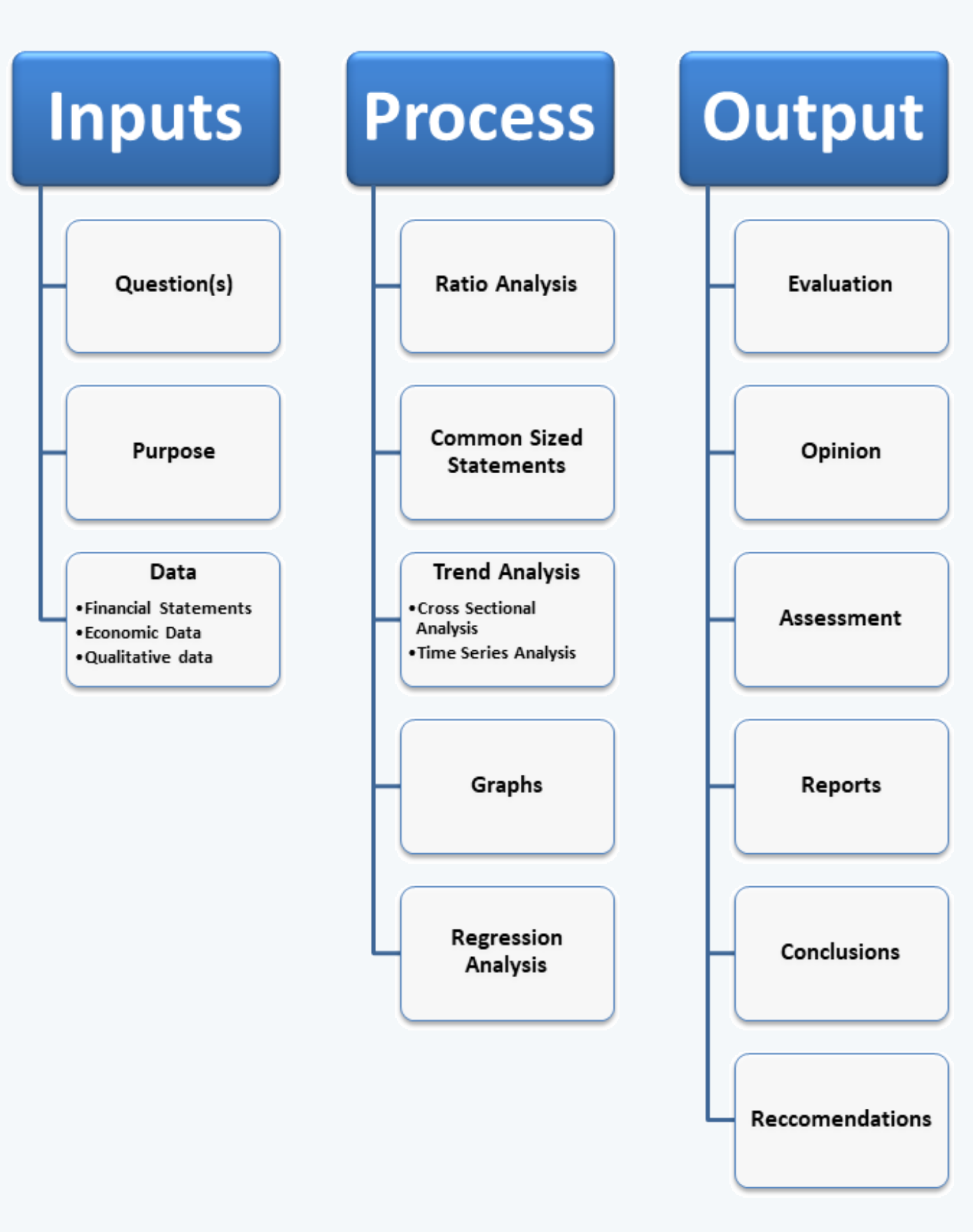

Before we begin the discussion about financial analysis; we need to understand three main components of financial analysis, i.e. inputs, process, and output.

Input begins with the question; the question as to what is the purpose of analysis, whether it is equity or credit analysis. Then we decide the purpose of analysis, which helps in deciding the data (whether from financial statements, economic data, or qualitative data) that would be needed to do the analysis.

The process, which is the main focus of the chapter, is the techniques that are used for the analysis purpose. Some of the major techniques are ratio analysis, common-sized statements, trend analysis, graphs, and regressions. One thing that needs to be noted here is that these techniques are not the end goal or the desired output, they only facilitate evaluation.

Lastly, the end goal of this whole process is the output that we get in the form of evaluation, opinion, assessment, reports, conclusions, and recommendations.