Accounting bodies across the world, including SEC in the US, has from time to time set the roadmap and deadlines for the convergence from GAAP towards IFRS; but these were rarely met.

In Europe, as per the direction of the European Union (EU), each of its member countries must individually adopt the IFRS, starting from 2005.

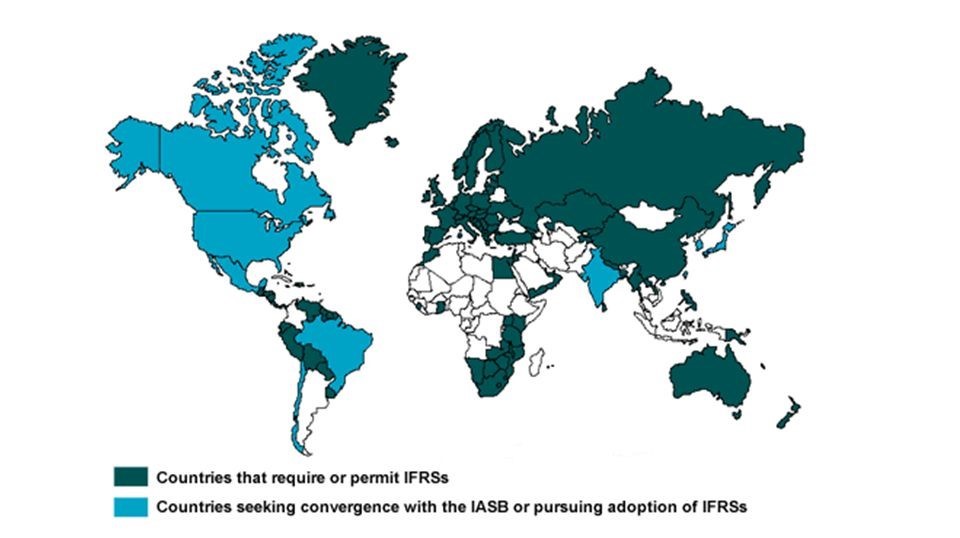

As far as most of the Asian countries are concerned they have accepted to adopt the IFRS, either directly or by converging their standards in line with the international standards and remaining compliant with local regulations and requirements. Around 120 countries have either adopted IFRS fully or issued directives and set deadlines for the same.

The convergence of these standards used by the countries worldwide with IFRS aims to achieve harmony with IFRS. The term convergence can be considered to mean: ‘to design and maintain national accounting standards in a way that financial statements prepared in accordance with a country’s accounting standards are in line with the IFRS’. IAS 1 requires the financial statements of entities to comply with all the requirements of IFRS. This, however, doesn’t mean that the IFRS should be adopted word to word. The local standard setters in any country can add certain disclosure requirements or remove some requirement that does not create compliance with their local accounting standards. Thus convergence with IFRS means adoption of IFRS with exception wherever necessary. IFRS is currently being used in more than 100 countries and it may be expected that all the major countries will adopt the same to some extent, at least, in near future.

The convergence of these standards and financial reporting is an important process that can be expected to add to the free flow of investments globally and tries to achieve important benefits for all capital market stakeholders. It improves the comparability of investments on a standard scale globally for the investors and thus helping in lowering their risk of errors of judgment. It eliminates the costly requirements of reinstatement of financial statements by facilitating reporting for companies with operations worldwide. It also helps in promoting greater transparency in the market, which helps all market participants, i.e. buyers, sellers, and regulators. It helps in reducing the operational challenges for accounting firms by providing unified reporting standards and helps to focus their value and expertise around other core objectives of the entity. It creates an opportunity for those involved in standard-setting and others towards improving the reporting model.

Convergence is a long-term process; it may take years of improvements and amendments to reach the goal of a single set of standards. In the near future, there may be a mix of standards and two sets of standard setters. Some of the standards may be expected to be prepared together and issued jointly, and others may be prepared and issued independently within the framework of convergence.

1. Why is Convergence Necessary?

In the present era of globalization and liberalization, the world has become an economic village. It has become extremely important to have a unified globally accepted financial reporting system. A lot of multinational companies are moving out of the confinement of their geographical boundaries to establish their business on a global map. The entities in emerging economies, in order to fulfill their capital needs, are increasingly accessing global markets by getting their securities listed on the foreign stock exchanges. Capital markets are, thus, becoming integrated and consistent with this worldwide trend. More and more companies are also being listed on overseas stock exchanges. A sound financial reporting structure is absolutely necessary for the economic well-being and effective functioning of capital markets.

The users of financial statements may get confused by the different treatments prescribed by different accounting standards for the same type of underlying financial transaction. This confusion also creates inefficiency in the capital market and complexity in the assessment of the financial statements and thus, calls for a single set of high-quality financial reporting standards. Good financial reporting standards will help in fortifying the faith the stakeholders would place in the financial reports of the business entities. Thus, the requirement of a single set of globally accepted accounting standards has inspired many countries to seek convergence of their local accounting standards with IFRSs.

2. Global Status of Convergence

IFRS are already used (either completely or in parts) in many countries across American, Europe, and Asia; such as countries in the EU, India, China, Pakistan, Hong Kong, Singapore, etc. The status across various countries of IFRS is as follows:

Brazil: Brazil has adopted IFRS for the reporting purpose in the case of publically listed companies along with CPCs (new Brazilian GAAP), since 2010. However for the companies other than the listed companies also the IFRSs are applicable, but the emphasis is more on the CPCs.

Mexico: In Mexico, the IFRSs as published by the IASB are applicable to all the companies whose shares are traded on the stock exchanges i.e. the publically traded companies. However, there is an exception for the financial institutions and the insurance companies; who are required to follow the Mexican Financial Reporting Standards. Also in Mexico, the IFRSs are not permissible for SMEs.

Canada: In Canada, the IFRSs issued by IASB as included in Part I of the CICA handbook are applicable for interim and annual financial statements of all the listed companies. However, for the US-listed issuers, the US GAAP continues to be applicable.

United States of America: In the US currently IFRSs are not applicable and permitted to any corporation. The currently applicable framework is GAAP.

US has always shown willingness to converge to the IFRS. It also had issued the guidelines and set deadlines for the part convergence; even though they were eventually missed. Right now, there is a lack of clear direction as to whether there is any likelihood of adoption of IFRS any time soon in the future.

Argentina: In Argentina, the IFRS as issued by the IASB for consolidated financial statements are applicable to all companies except the financial institutions and the insurance companies; since 2012. Here, for SMEs also the relative version of IFRSs is applicable.

The countries that are members of the European Union, such as the United Kingdom, Austria, Belgium, Greece, Germany, Sweden, etc. are required to adopt the version of IFRS as adopted by the European Union. The EU has a formulated various committees and groups (such as IASB, EGRAG, SARG, ARC, etc.) that issue directives and helps in the implementation of IFRS in the member countries.

India: In India, the IFRSs are planned to be adopted in a phased manner starting Apr. 2016, starting with the listed companies. In India, NACAS issues the IndAS, which are nothing but converged form of IFRS, which are planned to be implemented.

China: In China, the IFRSs are not applicable directly. They follow the Chinese Accounting Standards (CASs), which are nothing but converged form of IFRSs but easily understandable to Chinese readers.

Japan: In Japan, the IFRSs are neither applicable nor permitted on a standalone basis. However, there are companies that meet certain requirements (“specified companies”) that are permitted to use the IFRS for their consolidated financial statement; since March 2010. Additionally, in Japan, Japan’s Modified International Standards (JMIS) based on IFRS were introduced in 2015.

Saudi Arabia: In Saudi Arabia, the banks and financial institutions as regulated by the Saudi Arabian Monetary Agency are required to follow IFRSs. Others are not allowed to follow IFRS.

Singapore: In Singapore, the IFRSs are permitted only if either, company is listed on any other stock exchange outside Singapore that requires IFRS; or an exemption is granted by the authority. Other companies are required to follow Singapore Financial Reporting Standards.

United Arab Emirates: In UAE, all the entities except those in Dubai International Financial Centre and other free zones are required to follow the IFRSs as formulated by the IASB.