LOS E requires us to:

describe implications for financial analysis of alternative financial reporting systems and the importance of monitoring developments in financial reporting standards

1. Comparison of IFRS with Alternative Reporting Systems

IFRS is more of an international set of standards, aimed at providing a unified set of standards for all the reporting entities and users of financial statements across the world, in order to make comparison easier. Most of the countries either follow either IFRS in absolute form / converged form or their own set of accepted financial reporting standards, which have certain differences with the IFRS. Arguably, the most critical is the differences that exist between IFRS and US GAAP.

There is basically the difference in the treatment and the disclosure requirements as per both the US GAAP and the IFRS. Since the US GAAP are more of rules-based standards, there are regulations for every small detailed aspect of financial reporting; leaving very little room for manipulation and use of judgment by the preparers of the financial statements. The US GAAP was predominantly meant for the application to the US companies and was more akin to the taxation and SEC filing rules in the States.

However, the IFRS’s were predominantly formulated with an idea to have a uniform set of reporting standards that could be applied to the entities across the globe, making the financial statements more readable and easily understandable to the users of financial statements across the world. Thus the main principle, on which these standards were ought to be formed was adaptability across the countries, considering the varied tax structure and the legal framework. Thus, IFRS is more general in nature and leaves more scope for manipulation by the users.

For example, there are various aspects of reporting in which US GAAP differs from the IFRS. For instance, in reporting for fixed assets; as per the GAAP they must be carried at the historical cost and only a downward revaluation is possible. Also, exchange fluctuations on loans taken for the purchase of fixed assets can be expensed as incurred. However, as per the IFRSs, downward revaluation of fixed assets is also permissible and capitalization of exchange difference arising on repayment of liabilities incurred for the purpose of acquiring fixed assets is not permitted.

Also in accounting for inventories, as per the IAS, the inventories should be valued at a lower cost or realizable value. However, as per the US GAAP, there are certainly exceptional cases where inventories may be stated above the cost. These include the case of precious metals having fixed monetary value with no substantial cost of marketing stated at such monetary value.

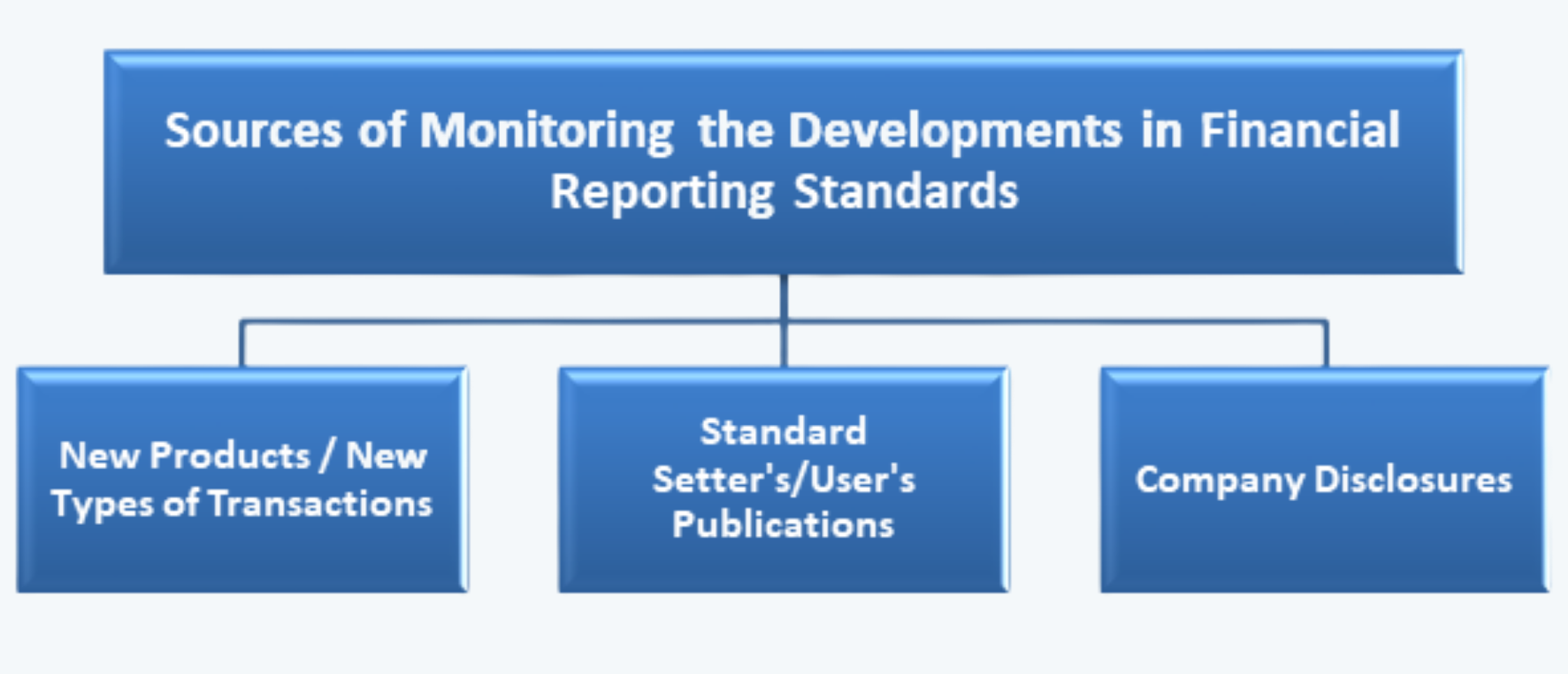

2. Monitoring the Developments in Financial Reporting Standards

For an analyst, it is imperative to monitor the developments in the financial reporting standards to understand what impact they will have on the valuation of securities and other financial instruments.

An analyst can monitor these developments by monitoring the following three things:

a. New Products or New Types of Transactions. These new products or transactions are those things that are new to the market and have not been accounted for before. Hence there are no standards available to account for the same. Thus these give a lot of scope to the management for manipulation. Information regarding such transactions can be gathered from the companies’ financial statements and business magazines or journals etc. Although there are no set of standards to account for the same; the analysts can look into the framework for the correct treatment of such transactions, to analyze their possible impact.

b. From the actions of standard setters and other groups representing users of financial statements. The information can be gathered from the websites, publications, journals, press releases, etc. of the standard setters such as IASB, FASB, etc., or the groups representing the users of financial statements such as CFA Institute. These groups regularly publish updates with respect to the new issues that require consideration, the new updates to the existing standards, etc. This information can help the analysts in understanding the developments and their impact on the analysis of the transaction.

c. The Company’s Disclosures. Companies preparing financial statements under any of the standards are required to make certain disclosures regarding the significant accounting policies used by them and any changes or deviations from the previous period’s policies and the impact of such deviations on the financial statements of the company. These disclosures can be found in the notes to the accounts and in the ‘management’s analysis and discussion’ section.

Analysts can also find the discussion about the impact of new standards on the statements, in these reports.