LOS D requires us to:

describe the different depreciation methods for property, plant, and equipment and calculate depreciation expense.

There are two ways of reporting non-current assets. They are

a. Cost Model. This model of reporting the long-lived asset is accepted by both IFRS and U.S. GAAP. According to this method:

i. The long-lived assets are reported in the balance sheet at their historical cost.

ii. This capitalized cost is allocated to the income statement of future periods as depreciation or amortization.

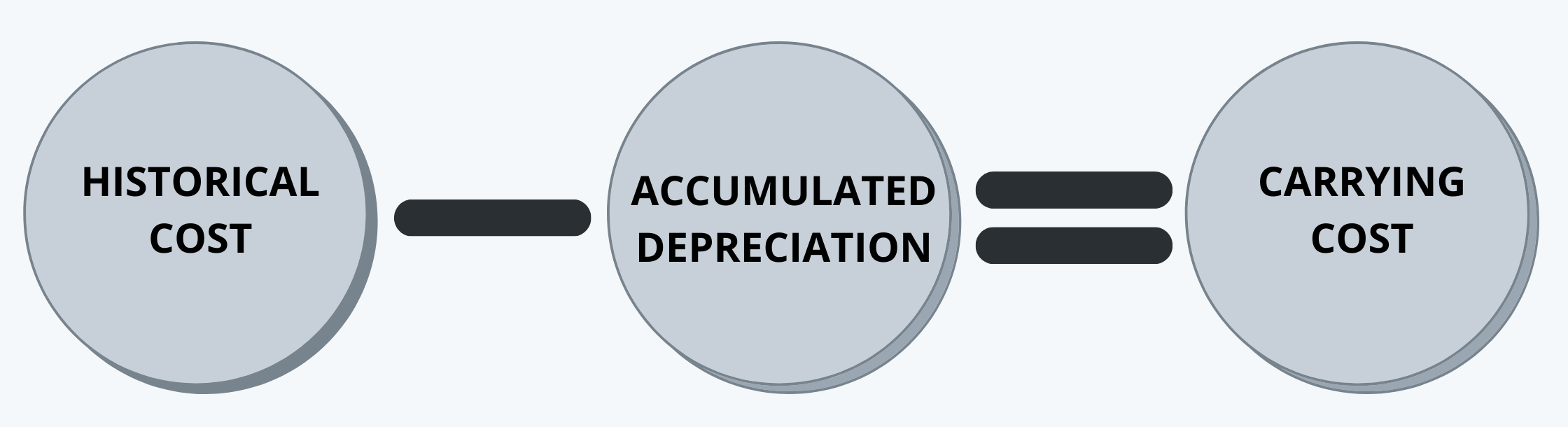

iii. Thus, the carrying cost of the asset is the historical cost as reduced by the amount of accumulated depreciation.

b. Revaluation Model. This model for reporting the long-lived asset is only accepted under IFRS. And, under this model, the assets reported at their fair value on the balance sheet.

1. Methods of Depreciation

There are many ways in which the depreciation may be calculated, which are accepted by IFRS and GAAP. There may be some other methods or rates of depreciation as required by the tax laws of different countries, apart from the ones accepted by the IFRS and GAAP.

Some of the important methods of depreciation are:

1.1. Straight-Line Depreciation

Under this method, the capitalized cost of the asset is allocated evenly across the estimated useful life of the asset. Thus, the depreciation expense each year can be calculated as follows:

|

1.2. Accelerated Depreciation Method

This method is also known as the ‘declining-balance method’. Under this method, it is assumed that there is greater wear and tear to the asset in its initial years. Thus a greater depreciation expense is charged in its initial years in comparison to later years. Here, usually, the depreciation expense is some percentage of the carrying value of the asset. And the percentage is such that the carrying value is depreciated to the expected salvage value of the asset at the end of its estimated useful life. Thus,

|

1.3. Units-of-Production Method

As per this method, it is assumed that the amount of wear and tear to the asset during a period depends upon the amount of economic benefits (as measured by the units of production during that period) provided by the asset. Thus, depreciation as per this method is based on the proportion of production during the period vs. the production capacity of the asset over its useful life. Thus, the depreciation expense can be calculated as follows:

|