1.1. Accounts Receivable

Accounts receivables include all the payments that are receivable by a company, whether in the normal course of business or otherwise. There are different aspects of accounts receivable that need to be managed properly so that the company can have a regular and timely flow of revenues and it doesn’t face liquidity issues. Some of the important aspects of accounts receivable management are:

1.1.1. Credit Management

a. Credit management is the process of managing the credit granting and its recovery. It basically involves preparing and following credit policies.

b. If the credit policies of the company are too lenient, the company may face a lot of bad debts and late recovery.

c. If the credit policies of a company are too tight, it may lose sales.

d. The credit policies of a company should be so balanced, so that it may maximize revenues and have timely recoveries.

1.1.2. Collection Management

a. It is the process of managing and monitoring the process from the time of sale to the time of payment being received.

b. These include policies for timely reminders, changing credit terms appointment of collection agencies, offering discounts for early payments, etc.

1.1.3. Receipts Management

a. At times there is a lag between the times when the payments are received to the time when the cash is available for use. Such period is called the float period.

b. The management of this float period is called receipts management.

c. The companies might have to pay a certain fee, at times, to reduce the float period. The management must manage this trade-off between the cost and benefits of reducing the float period.

d. The receipts system can be improved by moving to electronic payment, making use of lockboxes, and clearing the float, etc.

NOTE:

The tools that might help in the process of accounts receivable management are aging schedules, weighted average collection period, etc.

1.2. Inventory

a. Inventory is the stock of raw material, work-in-progress, and finished goods that are either ready for sale or will be ready for sale in the course of business.

b. The main aim of the system of inventory management is to maintain a level of inventory that ensures the availability of stock without any excess.

c. The shortages, if any, in the inventory and create a stock-out risk, which, in turn, may hurt the level of sales.

d. The excess inventory inflates the storage cost, increases the risk of obsolescence and shrinkage, and requires extra financing for working capital.

e. Inventory can be held for the same reasons as holding money, i.e. for transaction purposes, as a precautionary measure, and for speculative reasons.

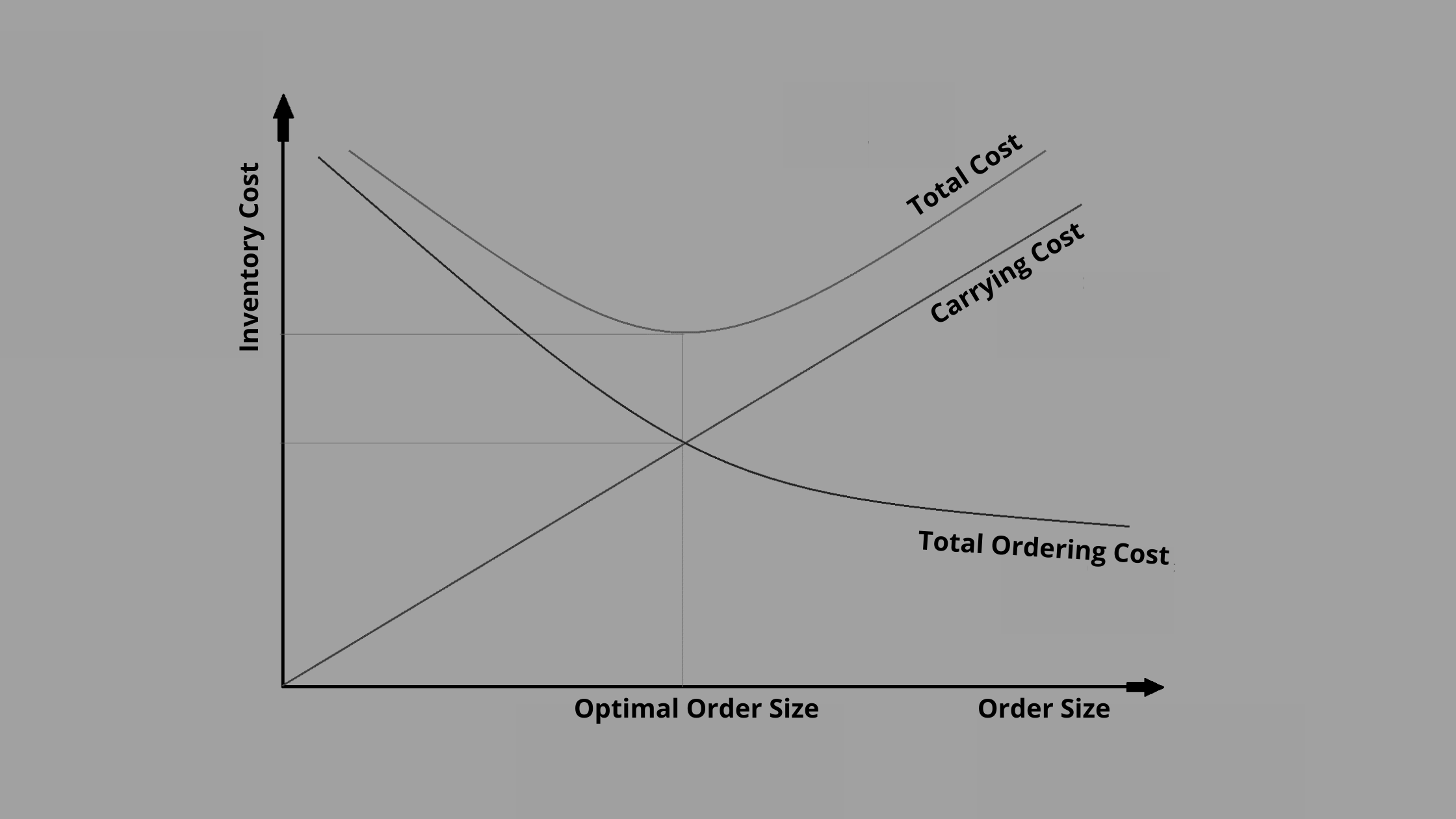

1.2.1. Economic Order Quantity

a. In order to find out the best level of inventory that minimizes the cost of holding and ordering the same, we should find out the economic order quantity (EOQ).

b. The formula for calculating the EOQ is:

|

EOQ= √(2SO/C) Where, S = Usage in units per period O = Ordering cost per order C = Carrying cost per unit per period |

c. This can be analyzed with the help of the following figure:

We can see, in the above figure, the optimal order size is the quantity, where the total cost of holding the inventory is minimum.

1.2.2. Just-in-Time

a. This is another method of maintaining inventory, where the inventory is ordered, as and when it falls to the minimum level.

b. This method of keeping inventory reduces the in-process inventory and associated carrying cost.

c. The reorder points under this system are determined by using the historical usage rate.

NOTE:

To determine the efficiency of the inventory management system, we can calculate and compare the inventory turnover ratio or the number of days of inventory, with the industry and historical data.

1.3. Accounts Payable

a. Accounts payables are the money owed by the company to its creditors in the ordinary course of the business.

b. The longer the number of days of payables, the shorter is the credit conversion cycle.

c. If the payment to the creditors is made too late, there is a deterioration of credit relationships and credibility with them and the company may miss out on the early payment discounts if any offered by them.

d. If the company makes the payment to the creditors too early, there is a loss of interest income (which could have been received on the assets, had the money been invested, instead of paying them to the creditors), and there is an increase in interest expense (if the payments are made from the borrowed funds).

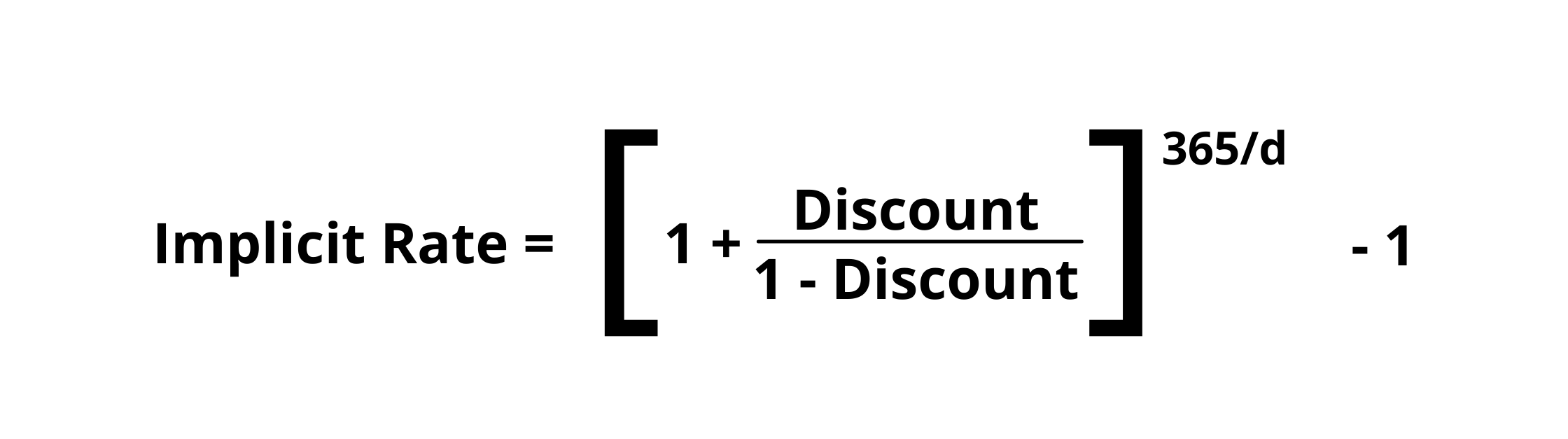

|

The implicit rate of discount can be calculated using the following formula:

Where, d = Number of days beyond discount period. |