LOS F requires to:

EXPLAIN AND DEMONSTRATE BETA ESTIMATION FOR PUBLIC COMPANIES, THINLY TRADED PUBLIC COMPANIES, AND NONPUBLIC COMPANIES

1. Regression Analysis

a. Typically, beta is calculated/estimated using regression analysis.

b. The beta is calculated by taking the historical return on a company’s stock and regressing it over the market return.

c. The regression equation found as a result is:

Rit = ậ + β Rmt

d. β is the estimate of the beta coefficient. It is sensitive to the following:

i. length of the estimation period (higher the estimation period, lesser is the richness of data and value of beta estimated),

ii. periodicity within the period (smaller the interval of each period used, the lesser is the standard error in the estimated beta),

iii. the selection of an appropriate market index (i.e. Rmt) also affects the value of β,

iv. use of a smoothening technique and adjustment for small-cap stocks.

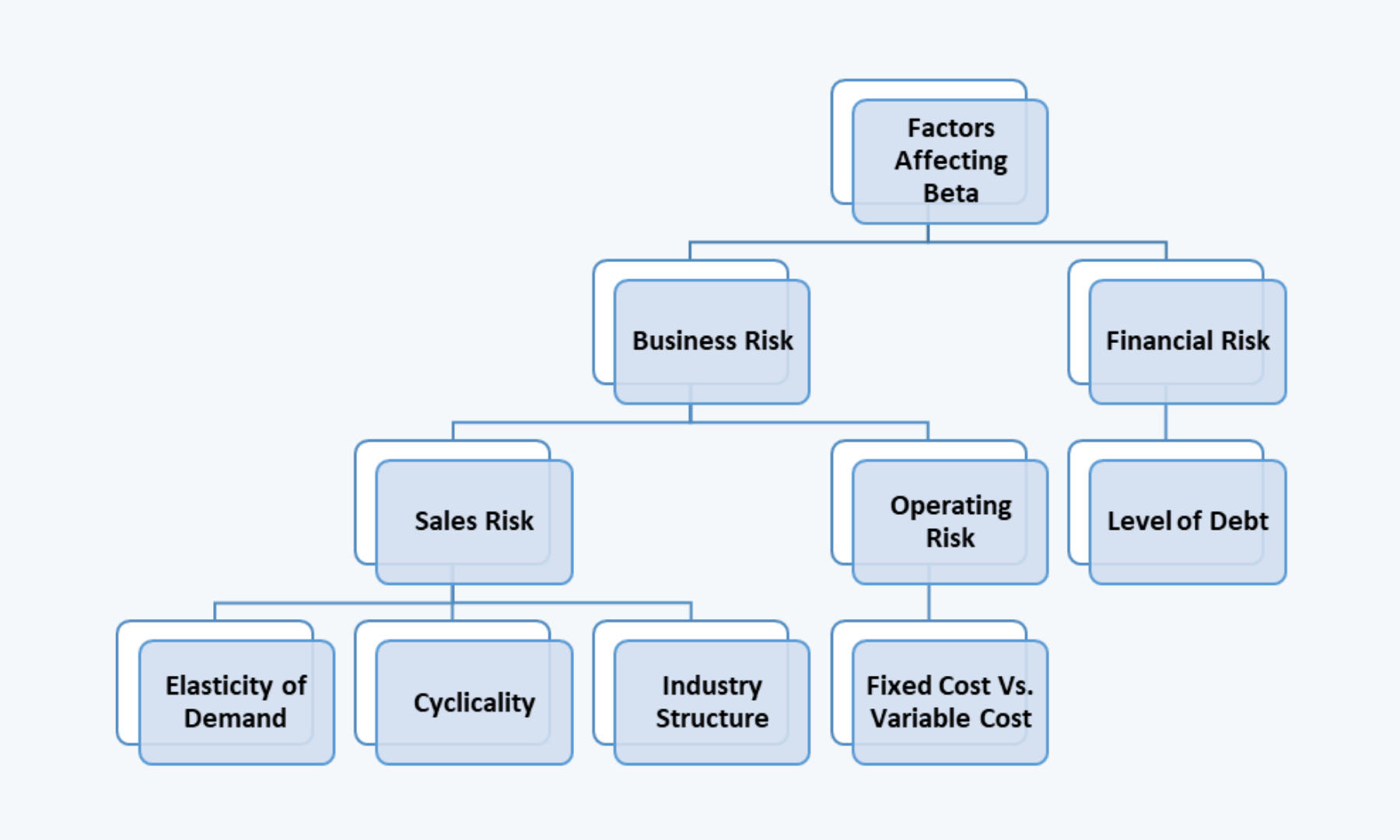

e. Beta is the measure of systematic risk, it is mainly affected by business risk and financial risk.

Business risk of a company is the risk related to the uncertainty of revenues, referred to as sales risk (which in turn is impacted by the elasticity of demand, its cyclicality, and the industry structure), and the operating risk.

Financing risk on the risk of the inability of the company to service the debt obligations. It is dependent on the level of debts.

1.1. Adjusting Beta

Another important thing about this beta we calculated above is that it is raw and or unadjusted. And it needs to be adjusted because it tends to move towards the value one in a long run. When the value of beta is one, it would mean that the expected return on equity would be exactly equal to the expected market return. So, we must re-adjust the beta.

The adjusted beta is an estimate of a security’s future beta. It uses the historical data of the stock but assumes that a security’s beta moves toward the market average over time. It weights the historic raw beta and the market beta. And the formula for the same is:

Adjusted beta = (.67) * Raw beta + (.33) * 1.0

2. Pure-Play Method

a. The pure-play method involves using a comparable publically traded company’s beta and adjusting for financial leverage differences.

b. The company so selected should have a similar business risk as to the project. There may be differences in the level of financial risk, which may be adjusted for the differences.

c. While analyzing the returns on a project we are concerned with the beta of the project. And, if the comparable beta is unleveraged (does not have the elements of debt), then we adjust the same by re-levering to reflect the capital structure of the project.

The beta of the project (i.e. beta of the assets) is:

ꞵA = ꞵDWD + ꞵEWE

Where,

ΒD = Beta of debt,

WD = Weight of debt in the capital structure,

βE = Beta of equity,

WE = Weight of equity in the capital structure.

Also,

WD = D/(D+E), and

WE = E/(D+E)

Therefore, we can re-write our equation as:

ꞵA = ꞵD[D/(D+E)] + ꞵE[E/(D+E)]

If we also include the impact of taxes on the debt of the company, we get:

ꞵA = ꞵD[(1-t)D / {(1-t)D+E}] + ꞵE[E / {(1-t)D+E}]

The above equation is also known as Hamada’s Equation. And while writing Hamada’s equation we make an assumption that the beta of debt equals zero.

Therefore, we can re-write Hamada’s Equation as:

ꞵA = ꞵE[E / {(1-t)D+E}]

If we now divide both numerator and denominator by E, we get:

ꞵA = ꞵE[E/E / {(1-t)D/E+E/E}]

Or, we get the following equation for the comparable unleveraged beta:

ꞵA = ꞵE[1 / {(1-t)D/E+1}]

Where,

D/E = Comparable company’s debt equity ratio

T = Comparable effective tax rate

βE = Comparable company’s leveraged beta

βA = Comparable company’s unleveraged beta

Thus, we can also re-write this equation as:

ꞵL = ꞵU [{(1-t)D/E}+1]

Where,

D/E = Comparable company’s debt equity ratio

T = Comparable effective tax rate

βL = Comparable company’s leveraged beta

βU = Comparable company’s unleveraged beta

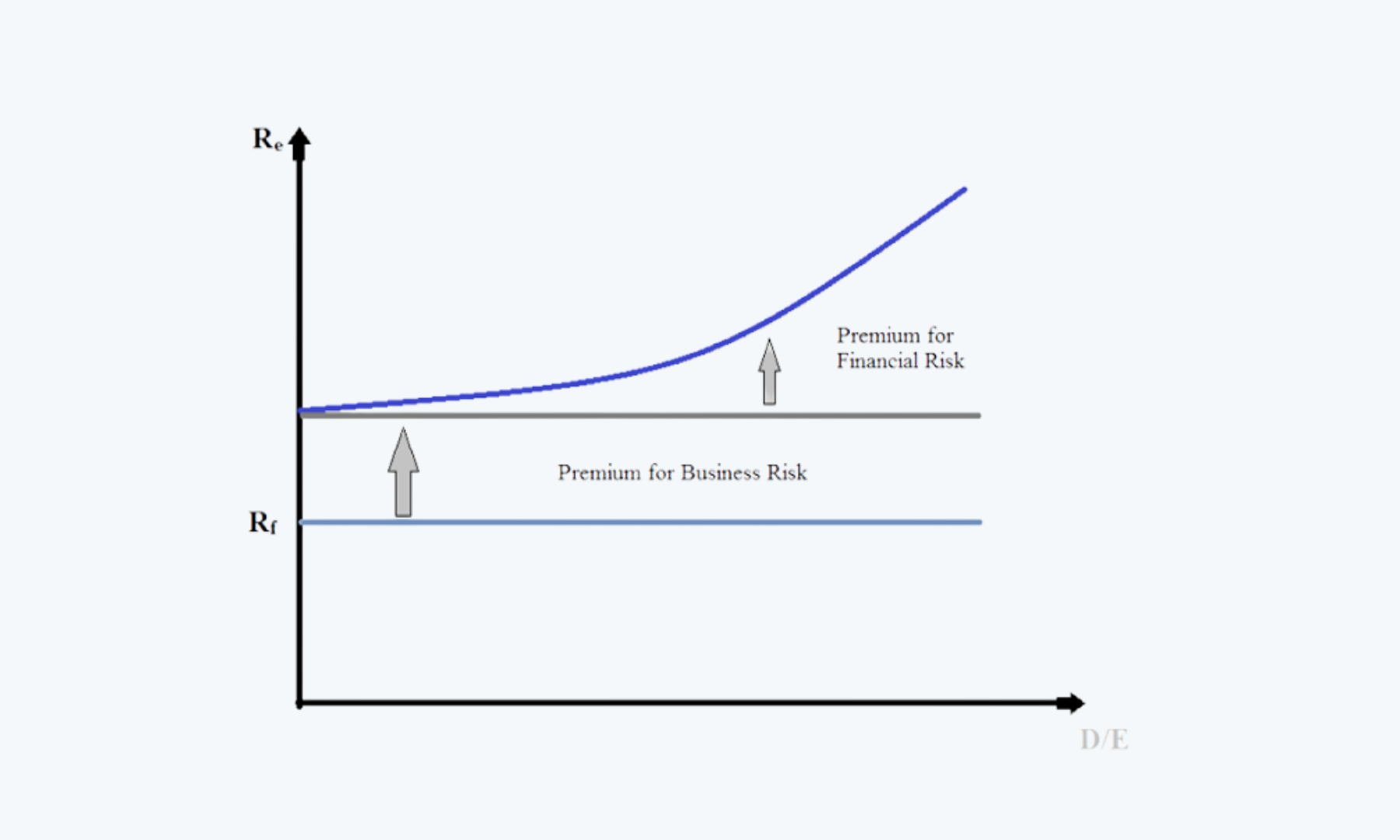

If we present this equation graphically, we get the following graph:

In the above graph, the level of risk till the time debt is equal to zero, represents the premium for business risk, as there is no leverage till that time. But as there is an increase in the amount of leverage, the increase in the amount of risk that follows represents the premium for financial risk.

Thus, to sum up, we can say that the pre-play method of estimating beta involves the following steps:

Check out our YouTube Channel for the latest updates.