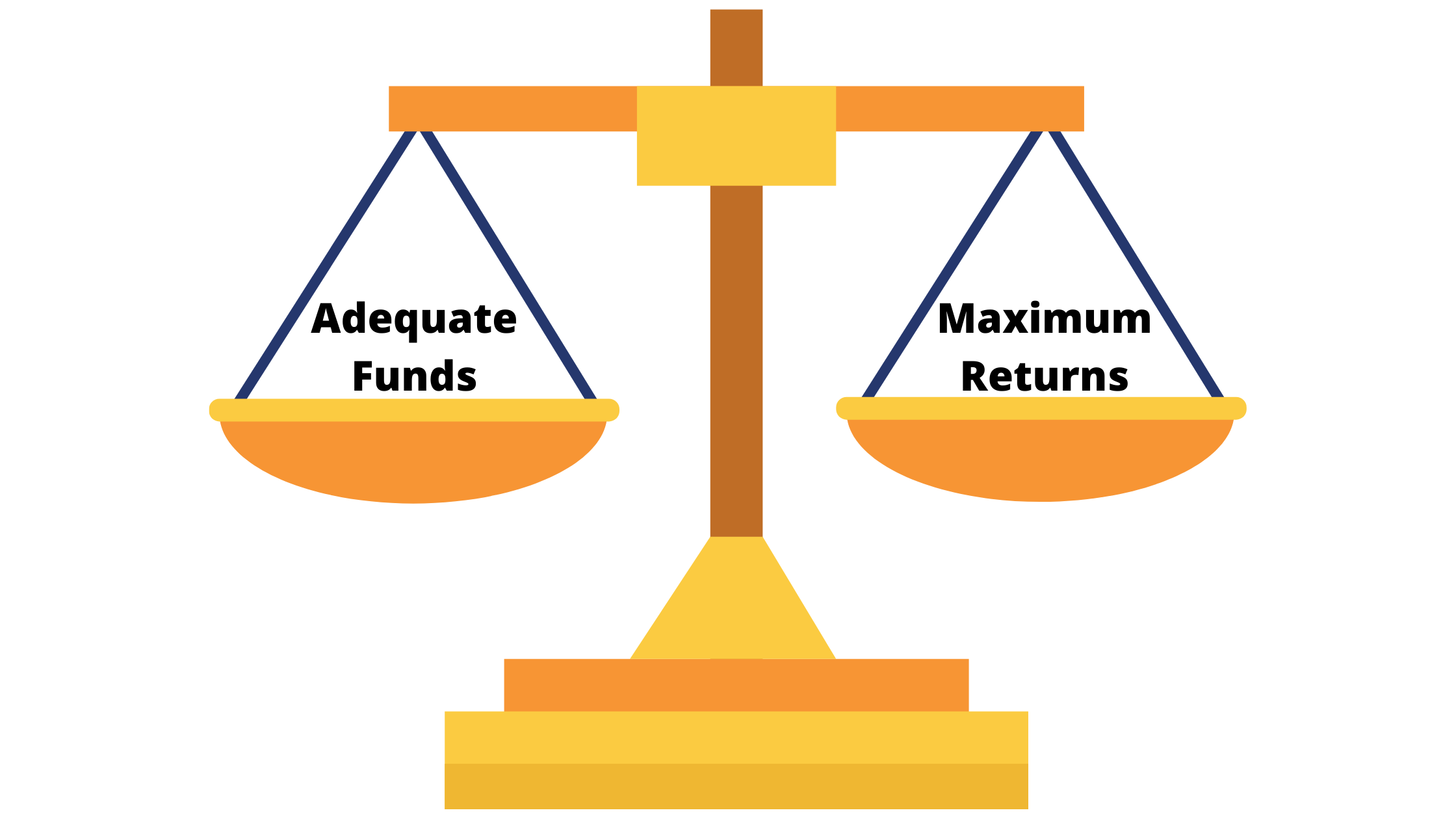

a. The main objective of working capital management is to maintain a balance between:

i. maintaining the adequate funds for day-to-day operations of the business, and

ii. ensuring maximum return by investing the assets in the most productive ways.

b. In order to have adequate cash for the operations of the company, the management must maintain adequate levels of cash. Investment in the short-term highly liquid securities or credit reserves comes in handy at the time when the liquidity of the firm is at risk. They act as shock absorbers for the fluctuating working capital needs.

c. And in order to maximize the returns, the management needs to invest in the projects or the assets that provide the maximum return, even though they may not be easily liquefiable.

1.1. Meaning of Liquidity

Liquidity is the extent to which a company can meet its short-term obligations using the assets that can be readily transformed to cash, either by sale or financing.

1.2. Primary Sources of Liquidity

The main sources of liquidity for a company are:

a. Ready Cash Balances. These include the cash in hand, balances in a bank account, and near-cash securities (having maturity of fewer than ninety days or one year).

b. Short Term Funds. These include trade credits/accounts payable, bank’s line of credit, short-term investment portfolios having marketable securities.

c. Cash Flow Management. It is the management’s effectiveness in maintaining the balance between the adequacy of funds and returns. It includes the cash credit cycle management and having a collection and payment system having a certain level of centralization.

1.3. Secondary Sources of Liquidity

For the day-to-day needs of working capital, the companies mainly resort to their primary sources of liquidity. But in the case of fluctuations or in emergency situations, the companies may also resort to secondary sources. Some of the most important secondary sources of liquidity are:

a. Debt Contracts. The companies can finance their liquidity with the help of long-term debt contracts; it is not one of the desired sources, though. It can also do it through renegotiating the existing contracts to increase the amount of debt or to reduce the number of monthly payments for interest and principals.

b. Liquidating Assets. The management can meet its liquidity needs by selling off some of the assets. This is also not a much-desired source, though.

c. Bankruptcy Protection / Reorganization. This can help in providing finance through liquidating the company or selling off unnecessary assets.

1.4. Factors That Influence the Liquidity

a. There are two kinds of factors that influence liquidity. The ones that drag the liquidity and those that pull the liquidity.

b. Some of the factors that drag the liquidity are: receipt lags, a high amount of uncollectible receivables, huge obsolete inventory lying in the stocks, tight credit due to lack of short-term credit available.

c. The main factors that pull liquidity are cash leaving early due to making early payments, reduced credit limits, limits on the short-term line of credits due to resting requirements, etc., low liquidity position as a result of growth or aggressive cash management.