LOS A requires us to:

describe the capital allocation process and basic principles of capital allocation

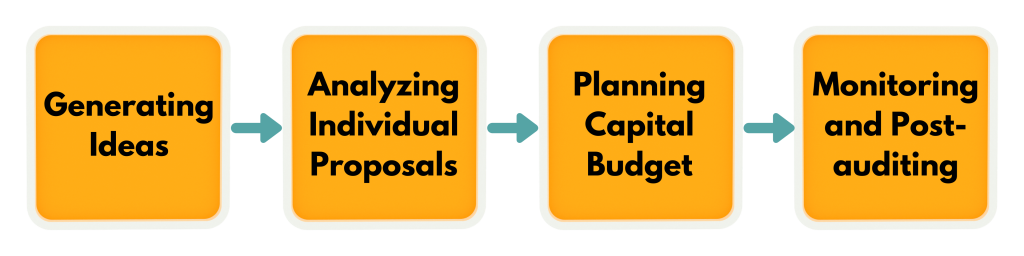

1. The Capital Budgeting Process

The exact capital budgeting process may differ from one investment to another, depending upon the size, level, and complexity of the project being evaluated. However, a typical capital budgeting process involves the following steps:

a. Generating Ideas: This is the first step in the process of capital budgeting. The ideas could be generated from anywhere within the organization or outside it. Within the organization, it could be generated at any level, in any department.

b. Analyzing Individual Proposals: Individual proposals could be generated using various capital budgeting techniques such as net present value, internal rate of return, payback period, discounted payback period, profitability index, etc., based on cash flow analysis.

c. Planning the Capital Budget: For the individual proposals so selected, they are planned to fit the timing, overall strategies, and resources of the company.

d. Monitoring and Post-Auditing: In this phase, the actual results are compared with the planned or predicted results. If there are any differences noticed they are sorted, and the plans are made to correct them in the future.

Monitoring and post-audit are important because:

i. It helps in identifying systematic errors.

ii. It helps in ensuring that management has employed the recommendations that were included in the audit report, and that all the issues that were identified are addressed. Thus, it improves business operations.

iii. It helps in better monitoring and forecasting the capital allocation process.

iv. Also, it helps in developing better ideas for future investment.

The process of capital budgeting is undertaken to make different categories of decisions, some of the important categories that require capital budgeting are:

a. Replacement Projects. There is always wear and tear in the long-term assets of the company over the years of usage. And after a period, they need to be either replaced or repaired. Capital budgeting is a very useful tool in deciding whether it is most economical to continue with the existing asset after giving it a repair or replace the existing asset with a new one. This is done by comparing the cost and benefits of the two options. Capital budgeting also helps in deciding whether to maintain the productive capacity or to gain efficiency or productivity improvement.

b. Expansion Projects. The existing capacity may be earning decent profits for the company, but sometimes, expansion may also further improve the productivity or profitability by adding the synergy effects. So, capital budgeting also helps in deciding whether it would be profitable to go in for capital expansion or not.

c. New Products or Services. Adding a new product or service to the existing line of business of the company is a key strategic decision. It requires a proper evaluation as to whether it would be profitable enough or not. Capital budgeting techniques help in deciding the same.

d. Regulatory, Safety, & Environmental Projects. These are usually the mandatory expenses that the companies must take. However, at times, the cost of these projects may be so high that it is better to cease the operations of such a company. Thus, the decisions regarding whether the operations should be ceased or not should be taken using capital budgeting techniques.

e. Others. For other decisions, that require choice, whether to lease or buy, make or outsource, etc., the capital budgeting techniques may be used.

2. Basic Principles of Capital Budgeting

The primary and the most basic principle in the process of the capital budgeting process is to pick up the project that is the most profitable one and has the highest positive net cash flow over the life of the project.

But before we discuss more principles of capital budgeting, it is extremely important to understand the important terminologies of capital budgeting. Some of them are:

a. Sunk Cost. These are the costs that have already been incurred and cannot be recovered in the future. Thus, for taking any capital budgeting decision, these costs should be ignored.

b. Opportunity Cost. This is the value of benefits that are foregone in making one decision over others. It is the value of benefits forgone for the next best alternative course of action.

c. Incremental Cash Flow. It is the value of additional cash flow realized as a result of the decision. It equals the cash flow that results from the decision as reduced by the amount of cash flow that could have been realized without the decision.

d. Externality. It refers to the effect of a decision on things other than the investment itself.

There are two types of externalities i.e., positive externalities (the ones that have a positive impact on the operations of the company) and negative externalities (the ones that may not have positive impacts).

Companies should consider externalities while making investment decisions. And if they have taken them into considerations, they are the absorbed externalities. However, some externalities may escape unabsorbed.

e. Conventional / Unconventional Cash Flows. The cash flow pattern could be considered conventional if there is only one sign change in the pattern of cash flow (where the cash flow starts with initial cash outflow, followed by a series inflow at a later stage). In an unconventional cash flow, there might be more than three sign changes in the series of cash-flows (from negative to positive or vice-a-versa). This may be a result of the expected capital expenditure between the project.

Thus, based on the above terminologies, the following are some of the principles of capital budgeting:

a. The decisions, in the process of capital budgeting, are taken based on the real cash flows only and not based upon the accounting/economic profits. The capital budgeting process only considers incremental cash flows. And, if the costs/benefits cannot be expressed as cash flow, they should be ignored.

b. Due to the impact of the time value of money, the timing of cash flow is extremely important. The sooner the cash flow, worthy it is.

c. The cash flows are based on opportunity cost.

d. The financing cost is ignored in the capital budgeting decisions. They are reflected in the cost of capital used in discounting the cash flows.

e. Cash-flows calculated on an after-tax basis are considered.

f. Accounting/economic net income is not considered for decision-making.

3. Evaluation / Selection of Project

There could be different types of project interactions that could form the basis of project selection. Some of them are:

a. Independent Projects Vs. Mutually Exclusive Projects. Independent projects are those projects whose cash flows are independent of each other. These projects can be selected together as well. Mutually exclusive projects, on the other hand, are those projects which compete directly with each other. Either of these projects can be selected, i.e. only one of these mutually exclusive projects can be selected.

b. Project Sequencing. Project sequencing is the process of creating a timeline for various projects, where investments are staged with an option to go ahead or not to go ahead, depending upon the outcomes of the previous project. For example, if we have a sequence of projects, say A, B, and C, sequenced to be undertaken one year after another, respectively, starting today. Then, if we start with project A today, and after one year, A turns out to be profitable enough, and economic conditions are also fine, then one can go ahead with project B, otherwise, scrap the project then and there itself. This way, there is a go/no-go option at the end of each intermediate project.

c. Unlimited Funds Vs. Capital Rationing. Capital rationing requires allocating funds to ranked projects. When the funds are limited, they must be utilized judiciously, in a way that can maximize the returns. This can be done through the rationing of the funds. On the other hand, if the funds are unlimited (which is rarely the case), they can be used in any possible manner.