a. We can understand a put-call forward parity with the help of the following example of two portfolios:

i. Portfolio A consists of a European call option and a zero that matures at X, and

ii. Portfolio B consists of a European put option and forward on underlying plus a zero with a forward price that equals FV.

b. The values of the two portfolios are equal, and the underlying asset for the options is the same forward which is a part of portfolio B.

c. The value of both the portfolios at the expiration of the options will be the same, i.e. the maximum of strike price or the exercise price. Their values at expiration are:

|

Portfolio |

ST > X |

ST < X |

|

Portfolio A |

(ST – X) +X = ST |

0 + X = X |

|

Portfolio B |

0 + (ST – F0) + F0 = ST |

(X – ST) + (ST – F0) + F0 = X |

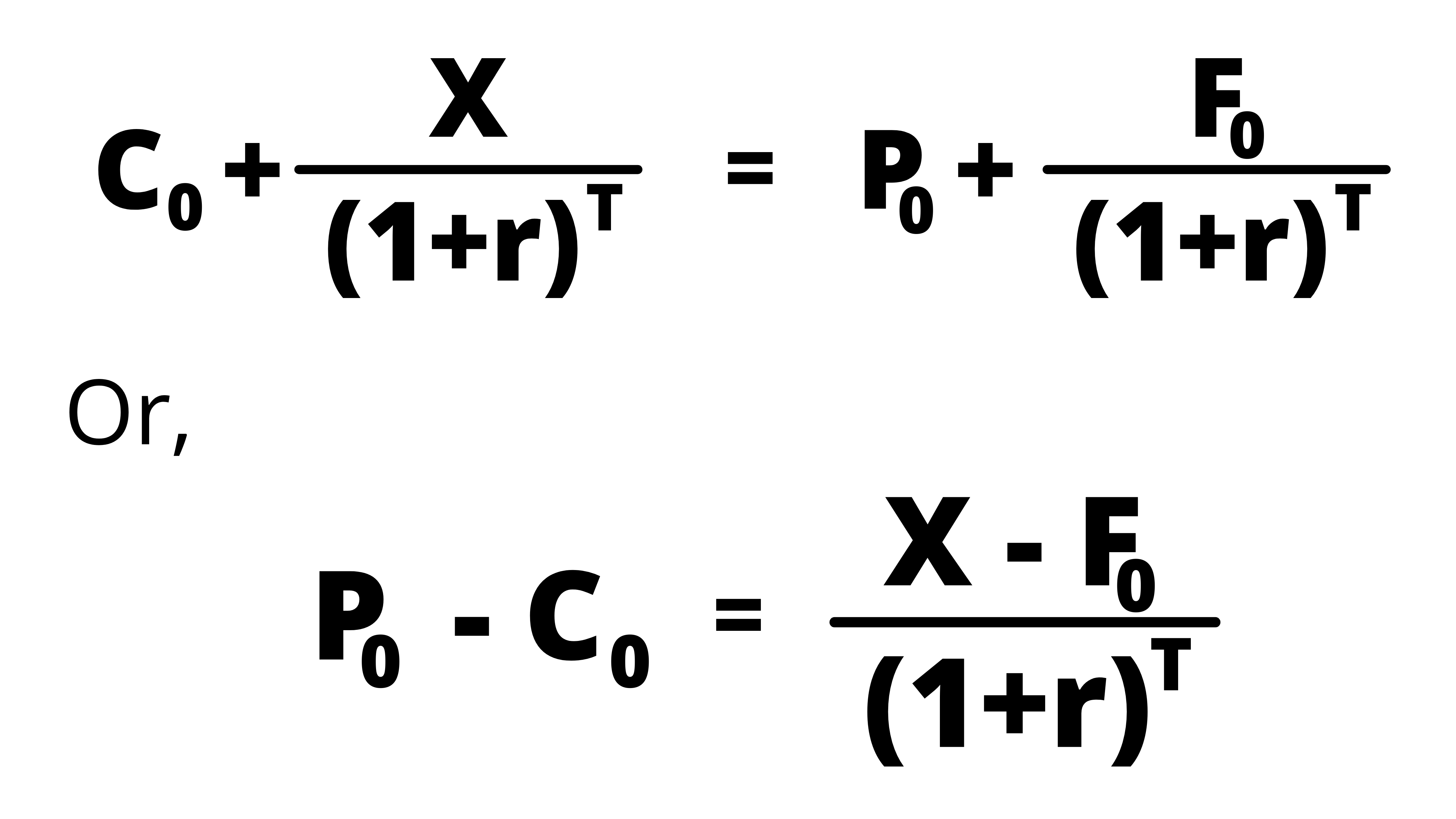

d. The present values of these two portfolios which have equal future values will also be equal. That is:

The above equation explains the put-call forward parity.