a. There are two parties to an option contract.

b. The buyer of a call or a put option is the long position in the contract.

c. While the seller of the option, also known as the writer of the option, is a short position.

1.1. Call Options

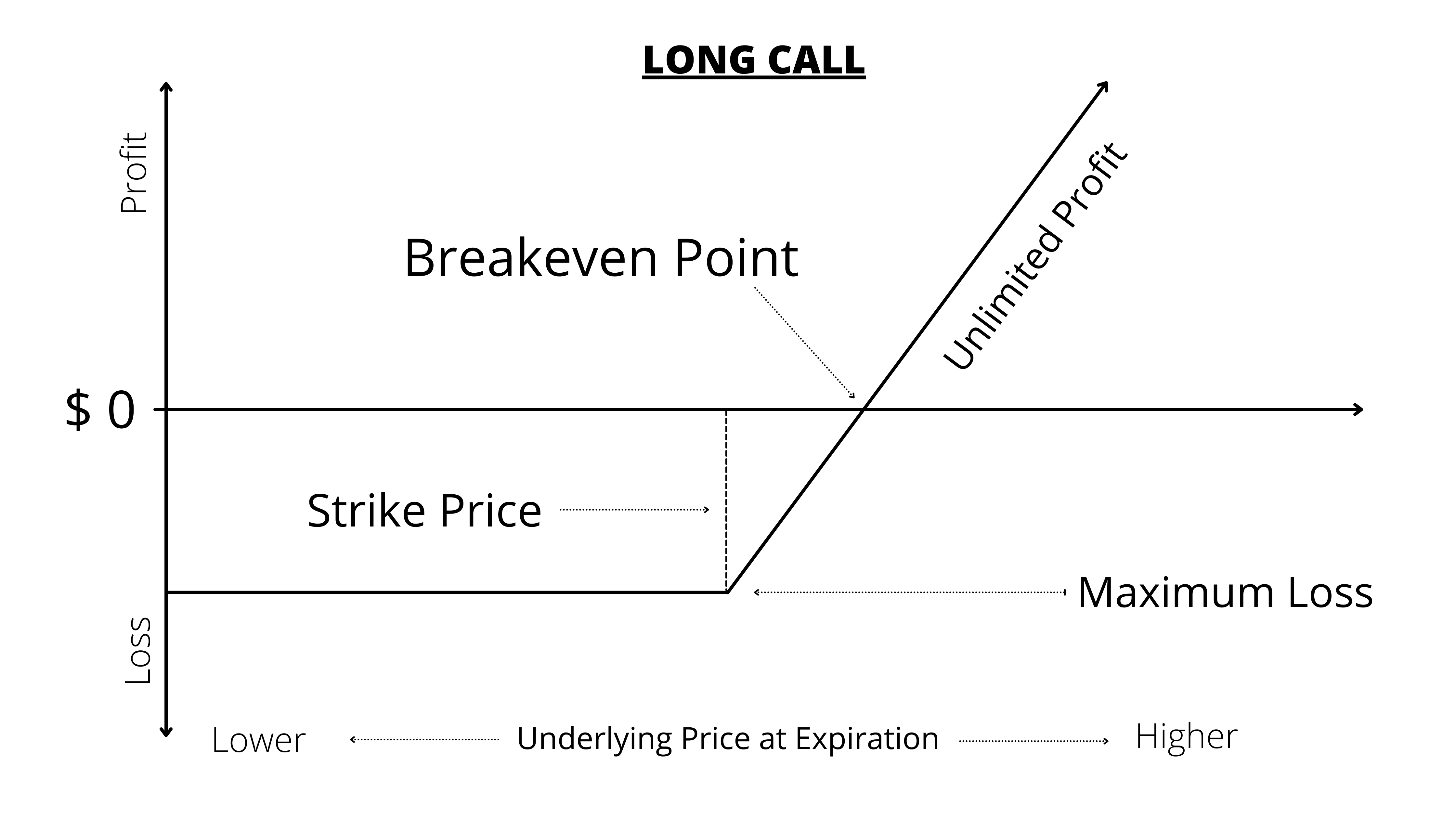

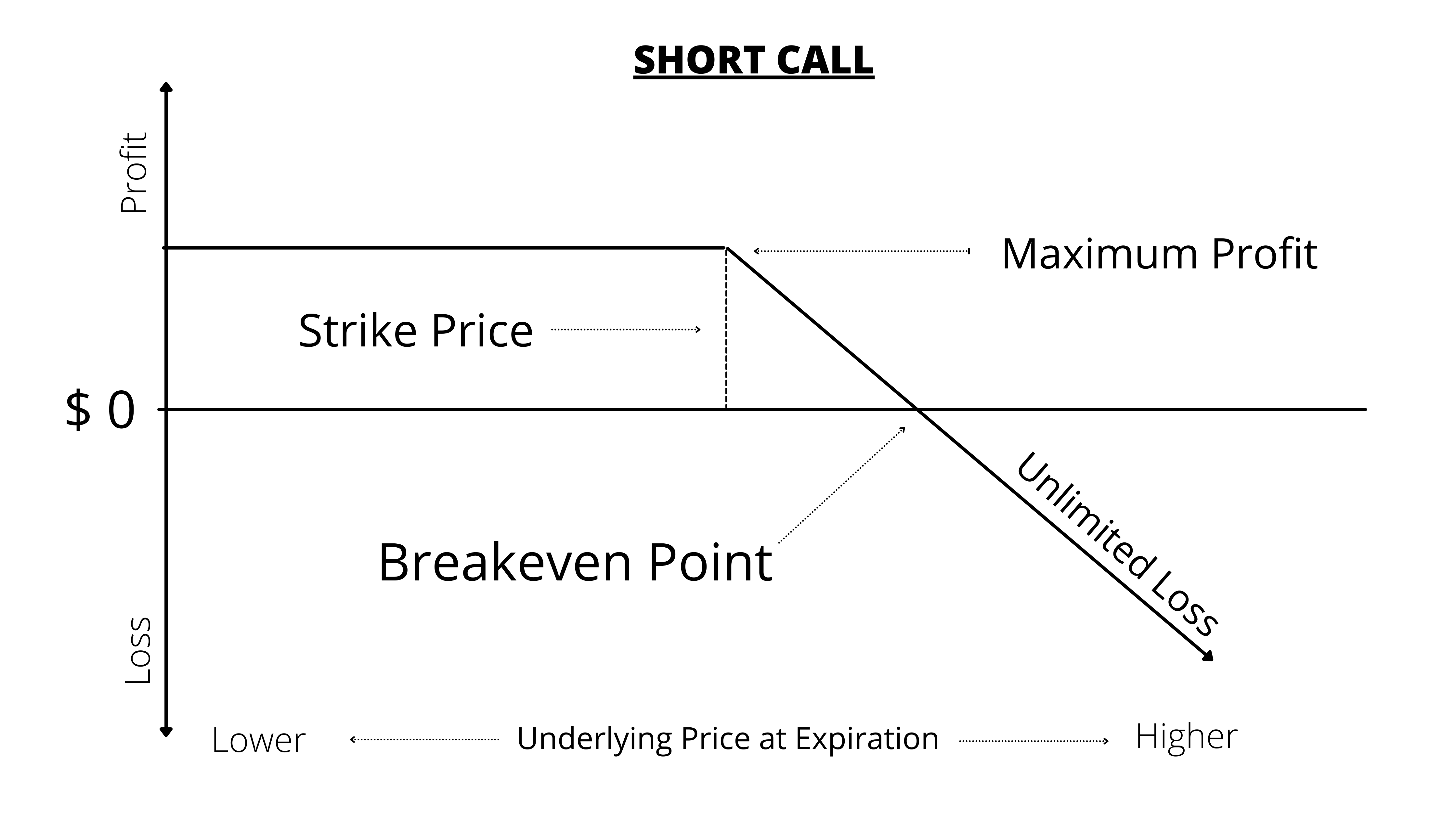

1.1.1. Value at Expiration of a Call Option

The payoff profiles of a call option are represented as follows:

Payoff for a call buyer = Max(0, ST – X)

Payoff for a call seller = −Max(0, ST–X)

Where,

ST is the price of the underlying at expiration; and

X is the exercise price.

1.1.2. Profit for Call Option

a. Using the payoff profile and the price paid for the option, the profit equation can be written as follows:

Profit for a call buyer = Max(0, ST–X) – C0

Profit for a call seller = −Max(0,ST –X) + C0

where c0 is the call premium.

b. The buyer of the call option has no upper limit on its potential profit and a fixed downside loss equal to the premium.

c. The seller has unlimited losses and gain limited to the premium.

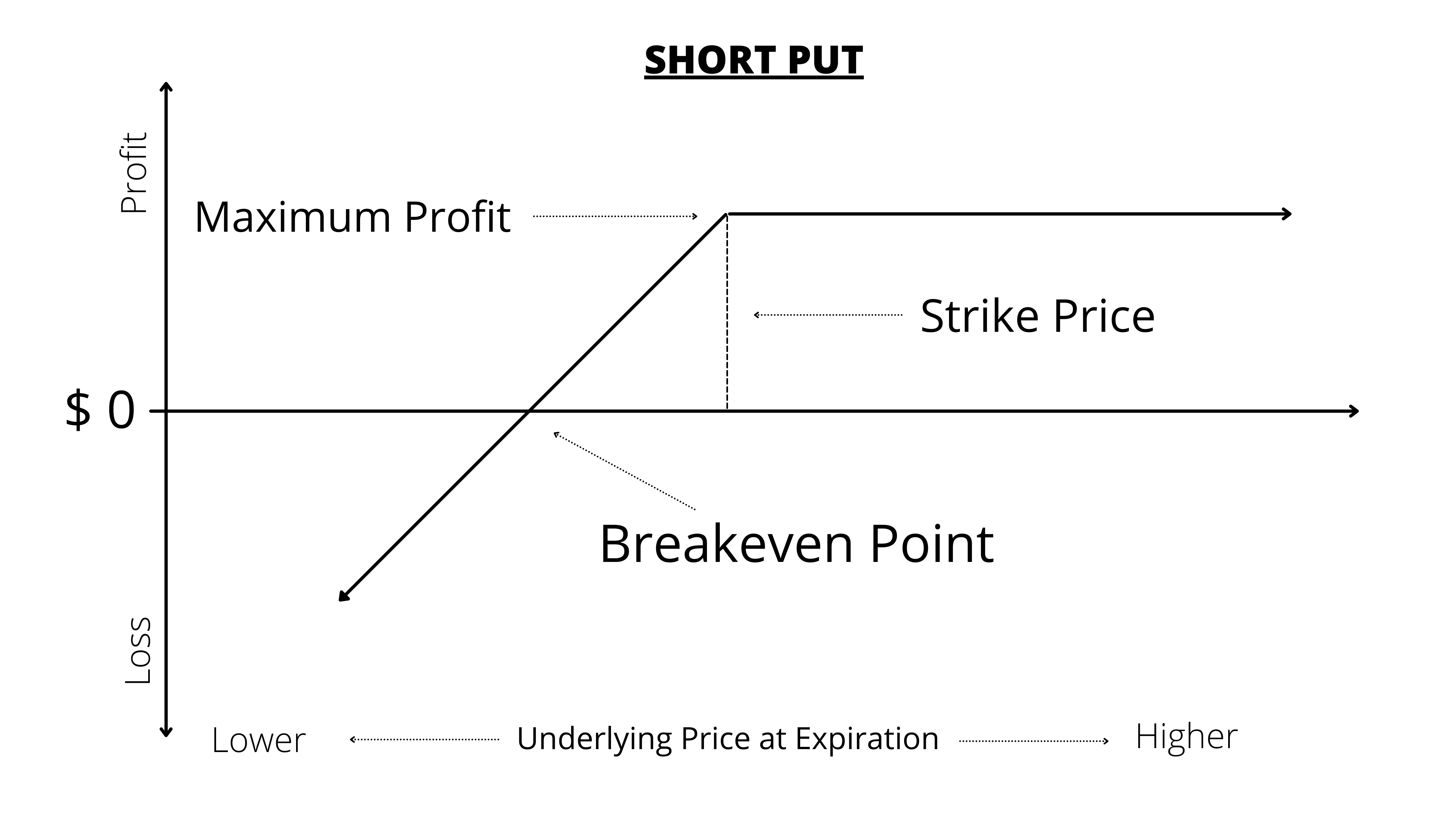

1.2. Put Options

In put options, we just have to replace the term “ST − X” by “X− ST”.

1.2.1. Value at Expiration for Put Options

The payoff and profit profiles of a put option are represented as follows:

Payoff for a put buyer = Max(0, X−ST)

Payoff for a put seller = −Max(0, X−ST)

1.2.2. Profit for the Put Option

a. Using the payoff profile and the price paid for the option, the profit equation can be written as follows:

Profit for a put buyer = Max(0, X−ST) – P0

Profit for a put seller = −Max(0, X−ST) + P0

Where P0 is the put premium.

b. The put buyer has a limited loss and, while not completely unlimited gains, as the price of the underlying cannot fall below zero, the put buyer does gain as the price falls.

c. The put seller has nearly unlimited losses and his gains are limited to the put premium paid to him by the put buyer.