a. As discussed above, different variables have a different impact on the prices of the put and call option; it is quite likely that the prices of call and put options on the same stock are interrelated.

b. We can understand the relationship between the call price and the put price by understanding the two portfolios as follows:

i. Portfolio A consists of a European call option and cash, and

ii. Portfolio B consists of a European put option and a share.

The values of the two portfolios are equal, and the underlying asset for the options is the same share which is a part of portfolio B.

The value of both the portfolios at the expiration of the options will be the same, i.e. the maximum of strike price or the exercise price. Their values at expiration are:

|

Portfolio |

ST > X |

ST < X |

|

Portfolio A |

(ST – X) +X = ST |

0 + X = X |

|

Portfolio B |

0 + ST = ST |

(X – ST) + ST = X |

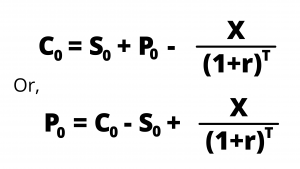

The present values of these two portfolios which have equal future values will also be equal. That is:

The above relationship explains put-call parity.

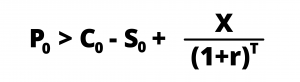

c. If the call-put parity relationship does not hold, then there would be arbitrage opportunities.

d. It is known from the above relationship that the value of a European call with a certain exercise price and a certain exercise date can be deducted from the value of the put option with the same exercise price and the date and vice-a-versa.

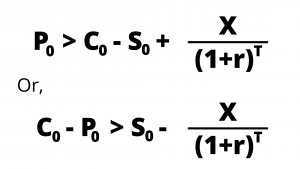

e. Though the above relationship holds good only for European options, we can also derive a similar relationship for the American option on a non-dividend-paying stock, as well.

Since P0 > p0, we have:

f. It can be easily proved that an American call option on a non-dividend-paying stock should never be exercised prior to the expiration date. Therefore, an American call option on a non-dividend-paying stock is worth of corresponding call option on the same stock.

Thus C0 = c0,

This is an equivalent put-call parity relationship between the American call and put option.