About Lesson

a. An FRA is a forward contract on the interest rate on the basis of a fixed notional principal where cash is settled based on the difference between the contract rate and reference rate existing on the closing date. The final settlement is done on the basis.

b. It allows the investor to lock in a certain interest rate for borrowing or lending at some future date.

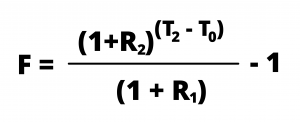

c. Suppose we expect to take a loan at the time T1, up to the period T2. During this period, we expect a rise in the interest rate. Suppose today at time T0, the interest rate up to time T1 is R1, and up to time, T2 is R2. The rate at which we can enter into the contract, F is: