1.1. Forward Commitments

a. Forward commitments are the financial contracts where the buyers and sellers agree to and are obligated to buy and sell a specific asset, at a specified forward or future price, by a specific date.

b. It is the over-the-counter (OTC) contract that obligates both parties (however, an exchange-traded forward is called a futures contract).

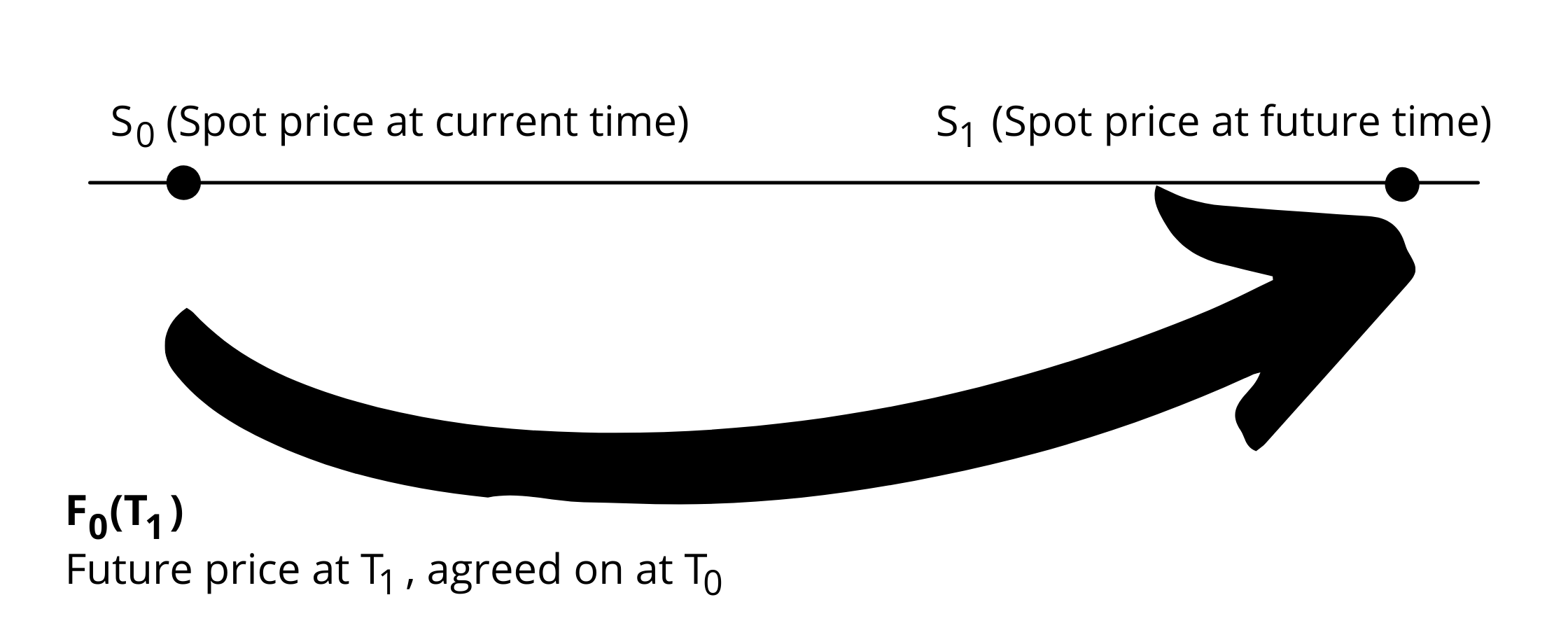

c. In this contract, a price at a future point in time is agreed on during the current time. Thus, in the current period, there would be two prices, i.e. the current spot price (the price at which the asset would be traded currently) and the forward price (the price at which the forward contract/derivative is traded).

This can be explained with the help of the following timeline:

d. The position of the parties at the time of squaring-off the transaction at T1 would be as follows:

i. If the spot price at T1 is greater than the forward price at which the contract is entered then the parties having long position profits and the parties with shorter position would lose. And, the amount of pay-off by each party equals the spot price at the future (squaring-off) date minus the agreed forward price. The party, incurring the losses has to pay this amount and the one making profits receives the same. Or,

|

If, S1 > Fo(T1)

|

ii. If the spot price at T1 is less than the forward price at which the contract is entered then the parties having short position profits and the parties with long position would lose. And, the amount of pay-off by each party equals the agreed forward price minus the spot price at the future (squaring-off) date. The party, incurring the losses has to pay this amount and the one making profits receives the same. Or,

|

If, S1 < Fo(T1)

|

e. All the forward commitment contracts are not delivered or deliverable. There exist the non-deliverable forwards (NFDs), that are cash-settled and are usually settled in cash for differences. The payoffs for such transaction is same as above.

1.2. Futures

a. Futures are nothing but the forward contracts that are traded on the exchange.

b. They are settled daily on a mark-to-market basis, on a settlement price that is determined by the market.

c. For trading in futures, both the parties to the contract, i.e. the one having a long position and the one having a short position, post a performance/margin bond, which is typically less than ten percent of the value of underlying assets.

d. There is a daily upper and lower price limit called the limit band for trading in futures contracts. The futures traded can occur within this band but not at the limit. The trades are thus ‘limit locked’.

e. In an exchange-traded futures market, only very few contracts are settled for delivery. Most of the contracts are offset by closing out or squaring the position before delivery.

f. The prices of the futures contracts may be different during the life of the contract, but these generally tend to converge at the expiration of the contract.

g. Since the futures are traded on the exchange, therefore, they are highly regulated and transparent and do not involve any counterparty risk.

1.2.1. Credit Derivatives

a. Credit derivatives are contracts where the risk of default in loans is sold by the lender to the other parties.

b. Credit derivatives act as the insurance to the default risk, though it avoids many of the regulatory constraints of insurance.

c. Under such a contract, a credit protection seller provides credit protection against a specific loss to the credit protection buyer.

d. Under a credit default swap, the insurance services are provided against the periodic payments. And, when the default occurs, the periodic payment/fees stop and the CDS is settled.

e. These contracts may be settled physically or in cash.

f. In the case of a physical settlement, the buyer gets the total amount of the default asset and delivers the asset to the seller. (The seller might still get something out of the contract, through the collaterals attached or otherwise).

g. Under the cash settlement, the net value of the asset, i.e. the par value of the asset minus the post-default market value of the contract is paid to the buyer of the contract.

h. The credit derivatives other than the credit default swaps are total return swaps, credit spread options, credit-linked notes, etc.

1.3. Asset-Backed Securities

Asset-backed securities are securities that are in the form of loans, credits, etc., which are usually backed by the assets purchased by its proceeds as collateral.

1.4. Swaps

a. It is a derivative contract under which the trading parties exchange financial instruments.

b. Financial swap means the agreed exchange of future cash flows with or without the exchange of cash flows at present. In other words, a financial swap is an agreement between two parties to exchange interest payments for specific maturity on an agreed-upon notional amount.

c. A swap is an exchange of two streams of cash flows. The value of each stream of cash flows is the net present value of cash flow in the stream. The price of the swap is the difference between the values of the two cash flows.

d. The length of a swap contract is called the tenor of the swap, and it ends on the termination date of the contract.

e. Swaps are similar to the forward contracts, as:

i. There is no payment when the parties enter into the contract.

ii. They are not standardized contracts, rather they are custom contracts.

iii. These are largely unregulated contracts that are traded on any organized secondary market.

iv. The main parties to the swap contracts are usually the large institutions and on the individual market participants.

v. These contracts are subject to default risk.

f. The most common type of swap is plain vanilla interest rate swap, where one party exchanges the fixed rate for the floating rate swap. Here the two parties may either completely exchange the series of payments, or they may also go in for a net settlement.

1.5. Options

a. Options are the contracts where the contracting parties have the option to buy or sell (depending upon whether it is a call option or a put option) the underlying asset at a pre-decided strike price.

b. The writer of the option may also go long or short in his position.

c. A long position is created by a person buying an asset without taking any offsetting position, whereas a short position is created when the person sells an asset without taking any offsetting position.

d. Under a long call option, the buyer of the option has the right to buy the underlying asset.

e. Under the short call, the writer of the option has the obligation to sell the underlying asset.

f. Under long put, the writer has the right to sell the underlying asset.

g. Under short put, the writer is obliged to buy the underlying asset.

h. The options may American Option that can be exercised any time up to the expiration of the contract, or they may be European Options that can only be exercised only on the expiration of the contract.