LOS N and O require us to:

n. explain the relationship between normal and lognormal distributions and why the lognormal distribution is used to model asset prices;

o. distinguish between discretely and continuously compounded rates of return and calculate and interpret a continuously compounded rate of return, given a specific holding period return

a. A random variable Y follows a lognormal distribution if its natural logarithm (ln,y) is normally distributed.

b. This method of the lognormal distribution is used to model the probability distribution of asset prices.

c. Some of the important features of lognormal distribution are:

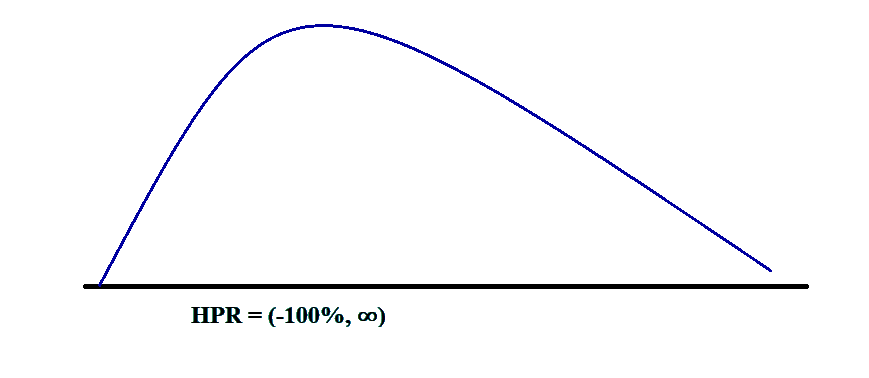

i. It is bounded by 0 on the lower end.

ii. The upper end of this distribution is unbounded.

iii. This distribution is skewed to the right (i.e. it is positively skewed).

d. A lognormal distribution can be drawn on the graph as follows:

e. If V0 is the beginning value of the distribution and Vt is the ending value of the distribution, then its ratio is such that:

f. This ratio i.e. Vt / V0 is distributed lognormally. However, its natural log, i.e. IN (Vt / V0), is normally distributed and unbounded at both ends. It is used as an approximation of actual returns.

g. The log of the ratio of the ending and beginning value of the distribution also equals the log of one plus the holding period returns.

h. The key point to be noted here is that if an asset’s continuously compounded return is normally distributed, then the asset’s future price must be lognormally distributed.

i. Thus, we can say that:

This was calculated by taking the natural log of:

Thus, we can also say that:

j. We can express the term St / S0 as follows:

Thus we can also write the equation as follows:

If we take the log of the above equation:

We can see that the above equation is now a linear combination of independent-randomly distributed variables. Therefore, a lognormal distribution is a normal one.

k. For the normal distribution to be useful in the analysis, there are two conditions that need to be satisfied:

i. Independence: It means that each of the individual variables in the distribution should be completely independent and should not have any information with respect to the other variables. The variables should be so unrelated so that:

That is, the probability of event ‘T’, given that the event ‘T-1’ has already happened, equals the probability of event ‘T’. This means that the previous event does not affect the probability of the following event.

ii. Identically Distributed: This means that all the variables must be identically distributed. This requirement emphasizes the stationarity of the data, i.e. the mean and the standard deviation of the data should not change from observation to observation.

However, the mean and standard deviations may not be the same for different financial and economic conditions.

These conditions imply:

Which is equal to:

l. A lognormal distribution can be applied to the volatility, which is the standard deviation of the continuously compounded returns.