LOS I requires us to:

explain the use of conditional expectation in investment applications

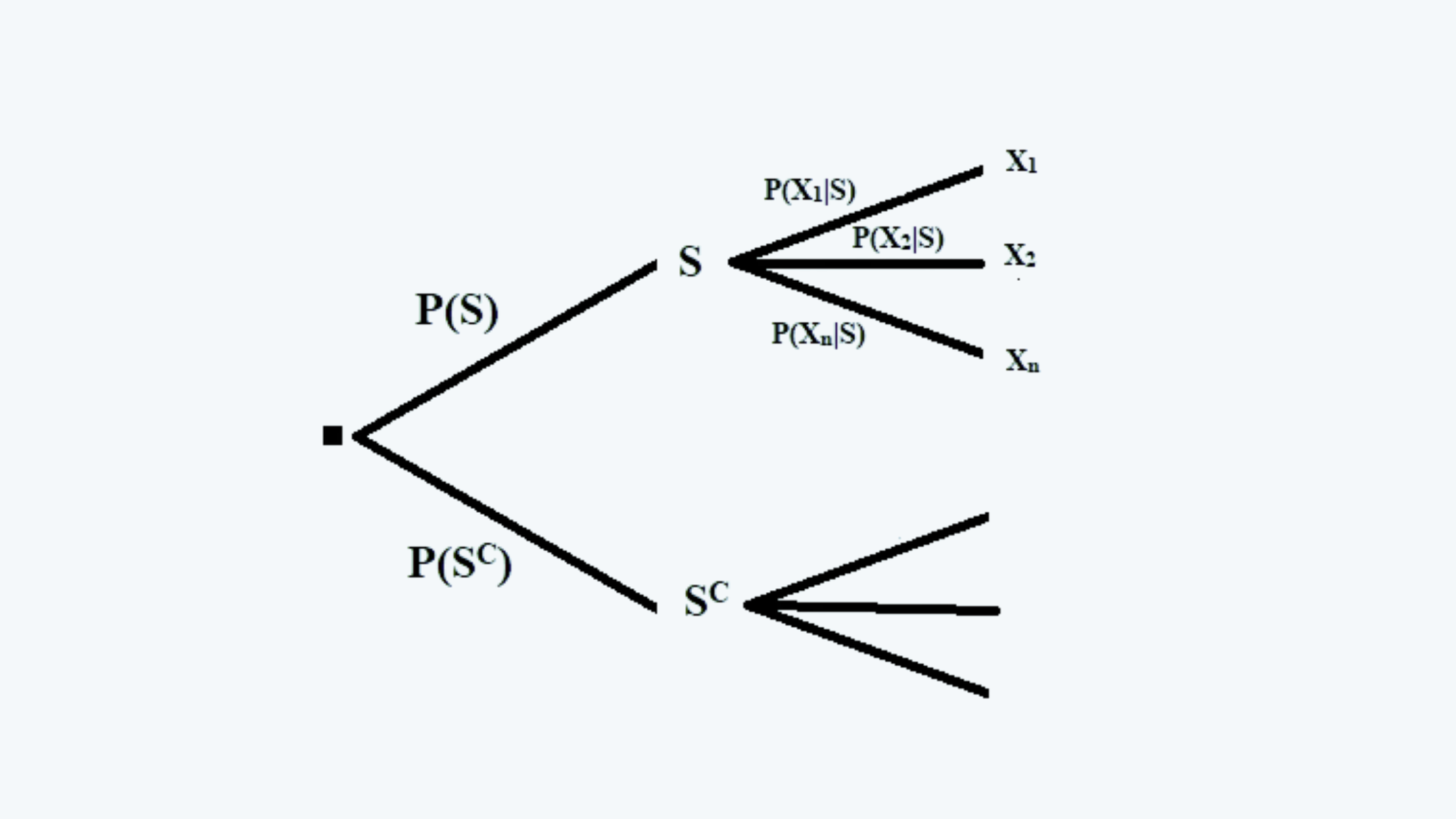

a. Consider the following expectation’s tree:

In the above tree, there are two events S (having two expectations, i.e. S and S not happening, denoted by SC), and X (having possible values of X1, X2, ….Xn).

Now, if we have to calculate the conditional probability of X, given that S has already happened; we can calculate the same using the following equation:

This can be simplified to the following equation:

b. Similarly, we can also calculate the total expected value of X, we can do so by summing up the possibilities of X in both cases when S has happened and S has not happened. That is

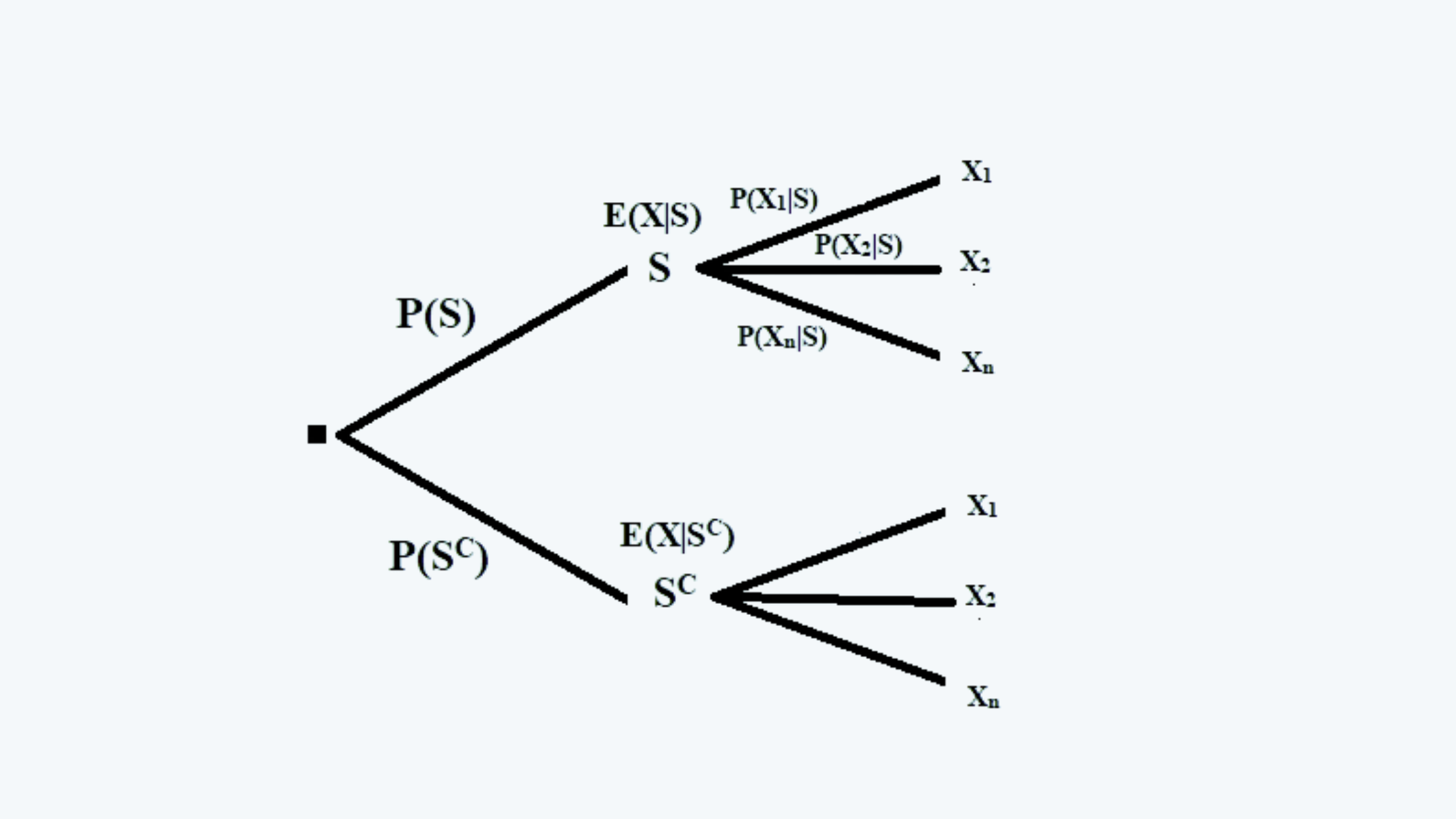

Thus, in the following figure:

the total probability or expected value of S would be:

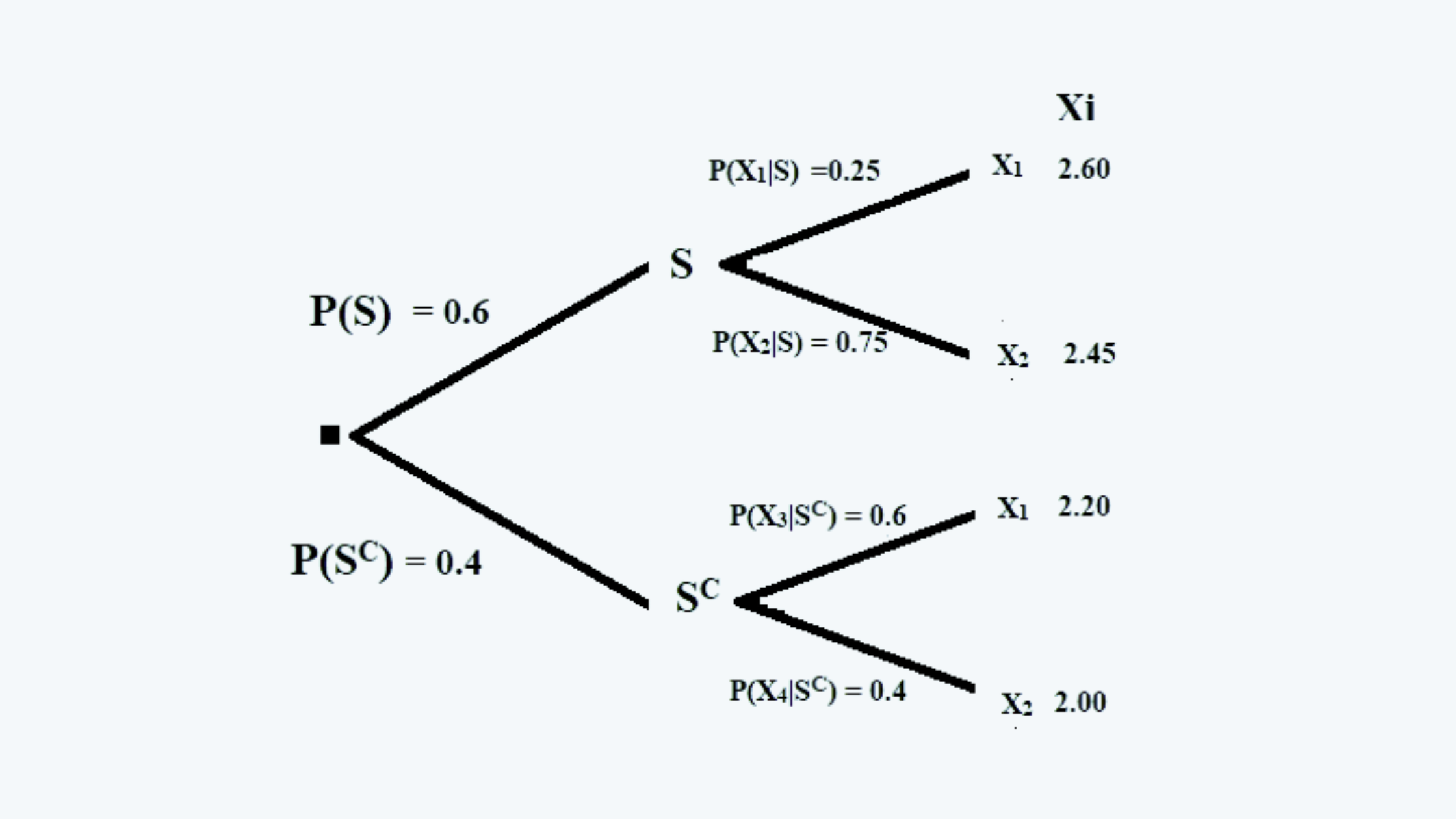

c. For example, if we extend the previous example to say that event X is succeeded by another event S having a 60% probability of S happening, and a 40% probability of S not happening. If S happens there is a 25% chance of event X1 and a 75% chance of X2. If S does not happens, there is a 60% chance of event X3 and a 40% chance of event X4. Consider the following table:

|

S |

P(S) |

X |

P(X) |

Xi |

|

S |

0.60 |

X1 |

0.25 |

2.60 |

|

X2 |

0.75 |

2.45 |

||

|

SC |

0.40 |

X3 |

0.60 |

2.20 |

|

X4 |

0.40 |

2.00 |

We can also draw the same on an event tree, as follows:

Now, the probability of individual values of X would be calculated as follows:

Thus the individual probabilities of values of X would be:

|

S |

X |

P(X) |

|

P(Xi) |

|

|

S1 |

0.6 |

X1 |

0.25 |

=0.6*0.25 |

0.15 |

|

X2 |

0.75 |

=0.6*0.75 |

0.45 |

||

|

S2 |

0.4 |

X3 |

0.6 |

=0.4*0.6 |

0.24 |

|

X4 |

0.4 |

=0.4*0.4 |

0.16 |

Thus the probability of X, given that S has already happened would be:

And the probability of X, given that S has not happened would be:

Thus, the total probability is:

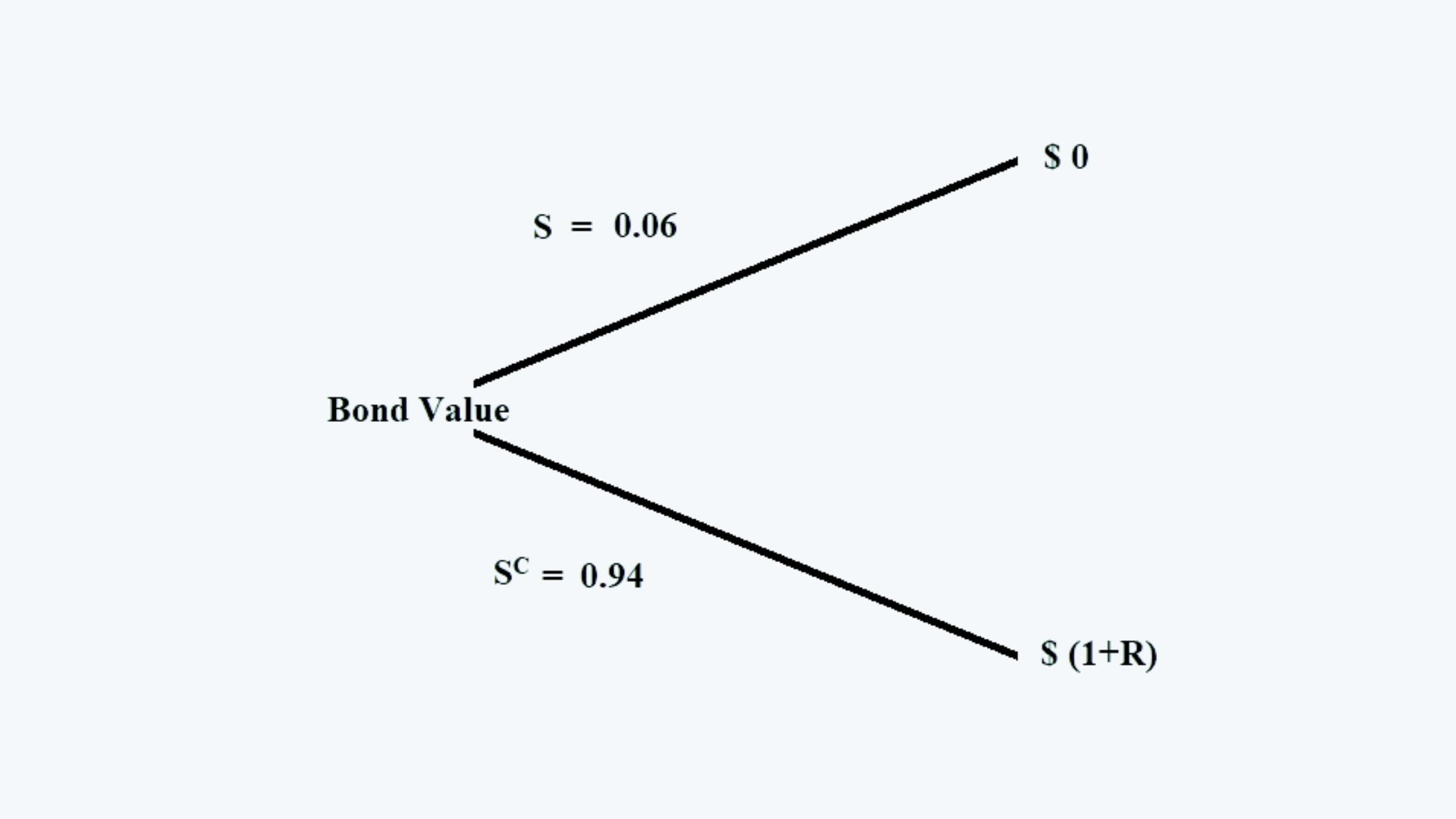

d. Consider another example:

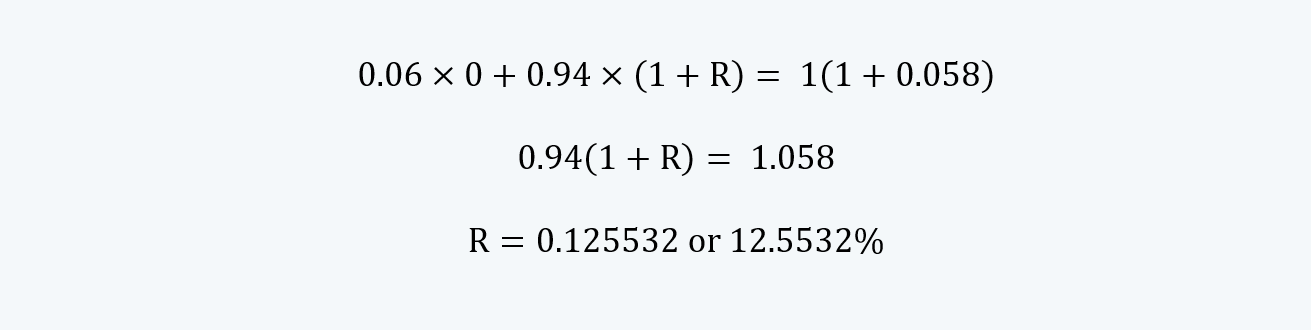

Suppose the probability of a bond default is 0.06. And if the bond makes a default its price at the end of the term would be 0. The risk-free rate on treasury bills is 5.8%. How much default risk premium should a bond earn?

Solution:

To calculate the same, we are given the following:

P(X) = 0.06, Rf = 0.058, & E(PB|X) = 0. We have to find the value of R-Rf.

Let the price of the bond, if it does not default be $ (1+R) (where R-Rf is the risk premium).

We can draw the expectation tree for the same as follows:

The value of the bond, after making the necessary provisions for the risk, should offer a return equal to the risk-free rate. Hence its price should be the face value plus the return at a risk-free rate. Thus, considering $ 1 face value:

Thus the risk premium is 6.75% or 0.675 basis points (i.e. 12.55%-5.8%).