LOS C requires us to:

explain systematic and nonsystematic risk, including why an investor should not expect to receive an additional return for bearing nonsystematic risk

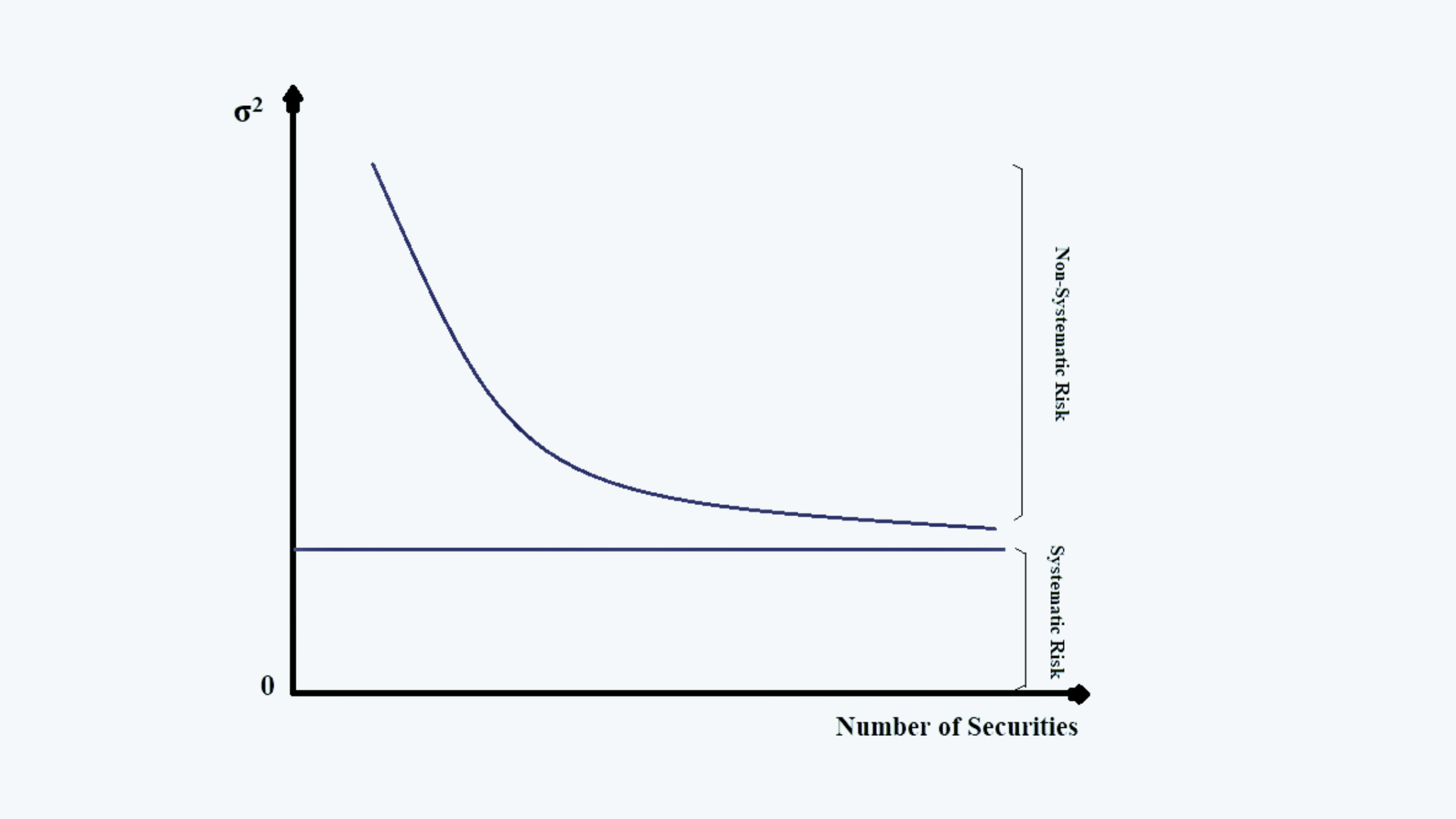

There have been researches on the effect of diversification on the total risk of the portfolios. These researches have indicated that as the number of securities in a portfolio is increased, the total variance of the portfolio decreases. The fall in the variance was in the form of a downward sloping curve, as shown in the figure below:

a. From the above figure, it can be noted that as there is an increase in the number of securities, the total variance (or risk) of the portfolio decreases.

b. This fall in the total variance can only be observed up to a certain level.

c. Thus, the risk that can be reduced, through the diversification of the portfolio is called the unsystematic of the diversifiable risk.

d. The diversifiable risk is the risk that pertains to a single company or industry. This can be attained through building a portfolio of assets that are not highly correlated with each other.

e. The risk that remains even after the diversification, and cannot be decreased by increasing the number of securities in a portfolio is called the non-diversifiable or systematic risk.

f. Systematic risk is the result of events or circumstances that affect the entire market or the economy, for example, the changes in interest rates, inflation, economic cycles, etc.

g. The total risk thus comprises two elements, i.e. systematic risk and non-systematic risk.

Non-Systematic Risk and Abnormal Gains

a. Now, let us assume that we receive returns for both diversifiable and non-diversifiable risks. That is, there is a perfect correlation between the risk and return. Thus there is an increase in returns with every extra risk that an investor is ready to take.

b. Since the non-systematic risk is diversifiable; the investors would buy a large number of assets with a large amount of non-systematic risk and then diversify it away. Thus, the investors would get paid for the risk that they can avoid.

c. This would result in increased demand for the diversifiable risk, driving up the price of the assets, thereby reducing its potential return.

d. Therefore no incremental reward can be earned for taking the diversifiable risk.

Examples:

a. Consider two assets, i.e. 3-months Treasury bill and S&P 500 index with a variance of 20%.

Of these the first asset, i.e. Treasury bill does not carry any risk, whatsoever, neither systematic risk nor unsystematic risk, as this is a risk-free asset.

The second asset, i.e. S&P 500 index is a well-diversified asset, having diversification across 500 different securities. Thus all the risk as represented by the variance of 20% is a non-diversifiable or systematic risk.

b. Now consider the other two assets, Asset A and Asset B. Asset A has a total risk of 30%, of which 15% is diversifiable and 15% is non-diversifiable. And Asset B has a total risk of 15% all of which is non-diversifiable.

Out of these assets, which asset should have a higher expected return?

The answer is Asset B. Despite the fact that Asset B has a lower total risk; it has a higher non-diversifiable risk that needs to be compensated with a higher return. And as seen in the above section, the investors cannot earn a return for taking diversifiable risks.

|

Thus, as per the capital market theory, the market will expect a higher return on investment that has a higher level of systematic risk, regardless of the total risk. The non-systematic risk is not rewarded by any efficient market. |