LOS A requires us to:

describe the implications of combining a risk-free asset with a portfolio of risky assets.

a. Introduction of the risk-free asset there is a better trade-off available to the investment for risk and return, thus improving the risk-return characteristic.

b. This trade-off can be better represented with the help of a capital allocation line (CAL). This will be discussed in detail in the next LOS.

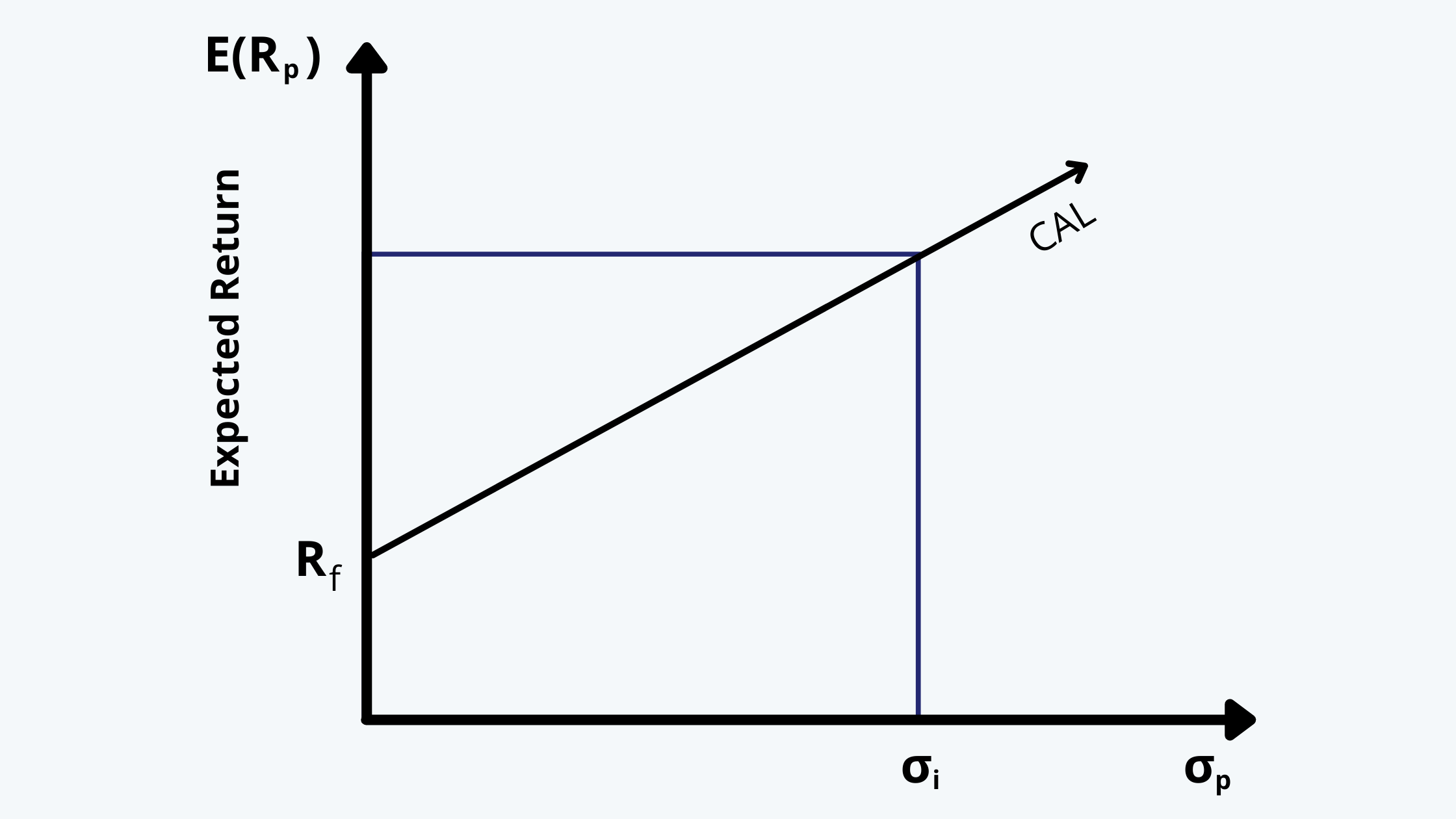

c. A capital allocation line can be drawn as follows:

On the horizontal axis, we take a risk, and on the vertical axis, the return. The trade-off is simple, higher the risk – greater the return. The CAL begins with the risk-free rate where the risk is zero. At that level, the returns are at a risk-free rate. The CAL is upward sloping because of the risk-return trade-off.

d. For a portfolio that contains both a risk-free asset and risky assets (i.e. the composite portfolio), the expected return can be calculated as the weighted sum of expected returns of the underlying assets.

e. And the portfolio risk of the composite portfolio can be calculated using the standard deviation, weights, and covariance or correlation between the assets. If you recall, the formula for the same is:

f. If the assets in the portfolio are negatively correlated then the variance (or risk) of the portfolio is lesser than that of the underlying assets, reducing the underlying risk of the portfolio.

This is mainly because the second part of the above equation becomes negative due to negative covariance.

g. It is difficult to find the optimal portfolio for the market because each individual has different assumptions and risk tolerance. Or, we have to make an assumption that the investor’s expectations are homogeneous.