LOS C and D require us to:

c. describe risk and return objectives and how they may be developed for a client

d. distinguish between the willingness and the ability (capacity) to take risk in analyzing an investor’s financial risk tolerance

The portfolio risk should be congruent to the risk tolerance of the investor. The risk tolerance of an investor is the lower of the ability and the willingness to take risk of the investor.

1. Risk-Objectives

There are basically two types of risk objectives that act as a restriction for discretionary activities of the portfolio managers, i.e. absolute and relative:

1.1. Absolute Risk Objective

a. This objective deals with capital preservation, such as maximum loss in any 12-month period. The main motive here is not to deal with the returns but to limit the losses due to the unsystematic risks of the company.

b. The managers can operationalize such objectives by identifying in numbers, the amount of downside fluctuations that the investor can bear. For example, one can select the risk level such that a 95% probability exists that the fund will not suffer a loss of more than 4% in any given 12-month period.

c. The measure of risk that can be used in the process may be variance, standard deviation, or value at risk.

1.2. Relative Risk Objective

The relative risk objective relates risk relative to one or more benchmarks perceived to represent appropriate risk standards.

These comparisons could be made with the help of a tracking error.

For example, large-cap equities can always compare their performance against the equity market index.

Institution’s Risk Objectives

The institution’s risk objectives may be tied to some future liability, such as pension plans.

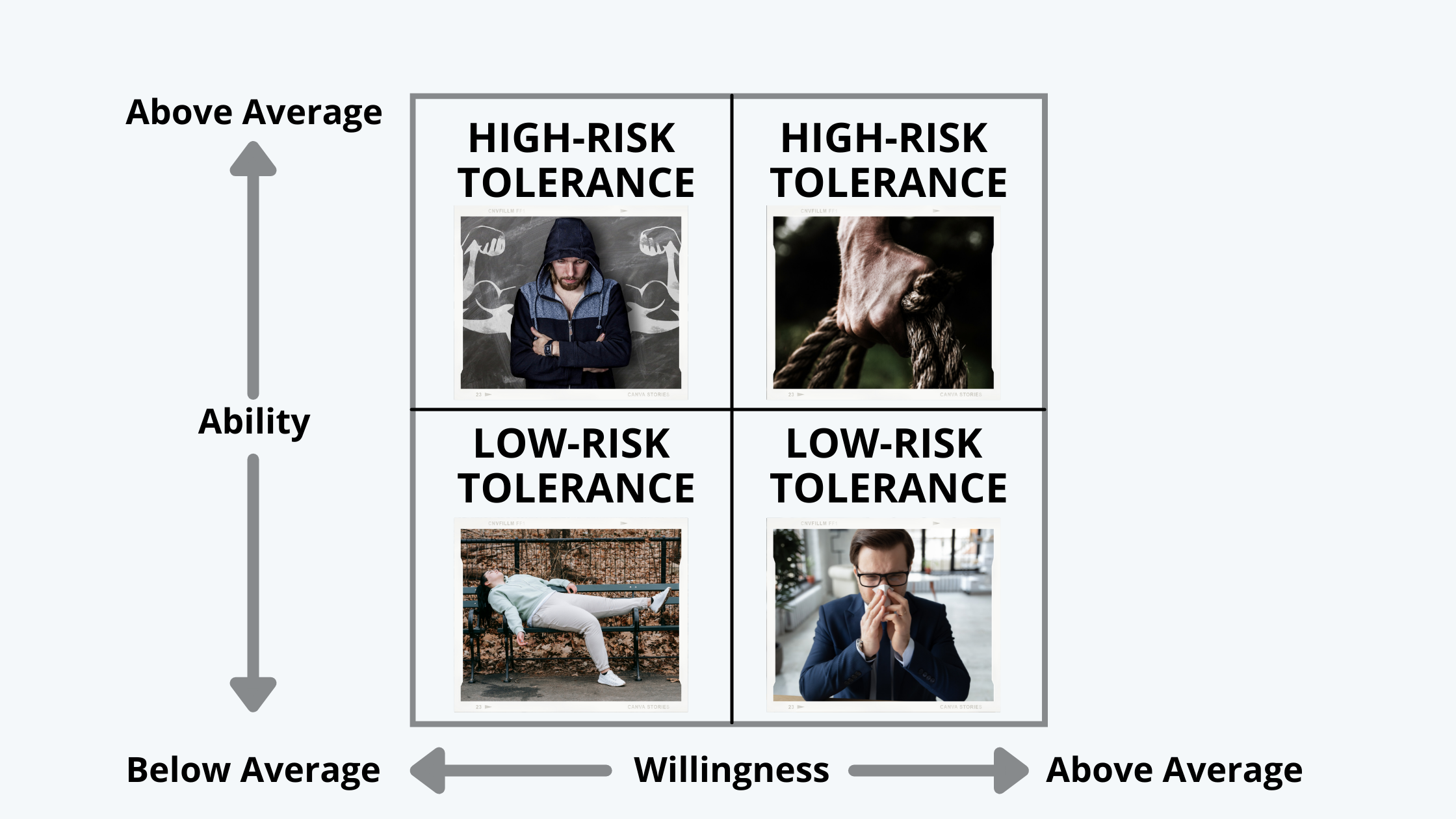

Risk Tolerance

Risk tolerance is a function of the ability and willingness of an investor to take the risk. The ability depends upon the time horizon of investment, the income levels, and the wealth of the investor. The willingness, on the other hand, is the disposition of the financial understanding of the investor.

The following matrix explains how the degree of willingness and ability impacts the risk tolerance of the investor:

If the client has a high risk-taking ability but low willingness, then the manager needs to explain the implications and conflicts in not taking the risk to the client.

Whereas, if there is a high willingness but a low ability then the manager needs to talk to the client and explain, they why need to lower the risk.

However, if both the risk-taking ability and willingness match, then this is a fairly easy situation. The manager knows the risk tolerance and can construct the portfolio accordingly.

2. Return Objective

The return objectives must be realistic in nature. The return objectives can be stated in terms of pre or post-fee basis, tax basis, or inflation basis. They can again be of two types:

2.1. Absolute Return Objective

Here, the return objectives are stated in realistic terms, such as a required rate of return of 10%.

2.2. Relative Return Objectives

The return objectives, here are stated in the terms of certain benchmarks and are compared against them.